Back in late January there was some talk of CBA replacing the notes issued by its subsidiary Colonial (ASX code: CNGHA) with a new hybrid. The talk was triggered by some heavy buying of Colonial Notes which had pushed the yield down significantly. CNGHA’s maturity date was only a couple of months away and so people put two and two together, thinking holders of these notes would receive priority allocations. CBA have now come and confirmed this is indeed what is happening.

The bank has announced it intends to issue $750 million worth of CBA PERLS IX Capital Notes (ASX code: CBAPF), with the ability to raise more or less than this amount. PERLS IX are subordinated, unsecured notes which will pay quarterly, floating rate distributions. CBA already have multiple ASX-listed hybrids (see tables) and these latest ones will be similar in structure. The proceeds will be used for general purposes.

The new capital notes will qualify as Additional Tier 1 (AT1) capital under the Basel III bank regulatory framework, which means they have the now-standard “trigger events” which may lead to early conversion into ordinary shares or a write-off of the notes. At the prevailing level of interest rates, they will pay around 5.70% (annualised) inclusive of franking credits. As interest rates change, specifically the bank bill swap rate, quarterly payments will also change.

As with CBA’s other hybrid securities, these new capital notes have an indicative distribution of 90 day BBSW plus a margin of 390bps to 410bps. The final margin will be determined by a book build, which is a tender process managed by investment banks on behalf of CBA. If recent history is any guide, then the margin is likely to be set at the lower end. Distributions are to be non-cumulative, at the discretion of CBA directors and paid quarterly in arrears.

The first call date, the date on which CBA can redeem or resell the securities, is on 31 March 2022 and, by convention, securities are typically redeemed on this date. If redemption does not occur, exchange for ordinary shares will occur on 31 March 2024, subject to the mandatory exchange conditions. If the mandatory exchange conditions are not initially met in March 2024, the conditions will be tested on each distribution date thereafter until exchange takes place.

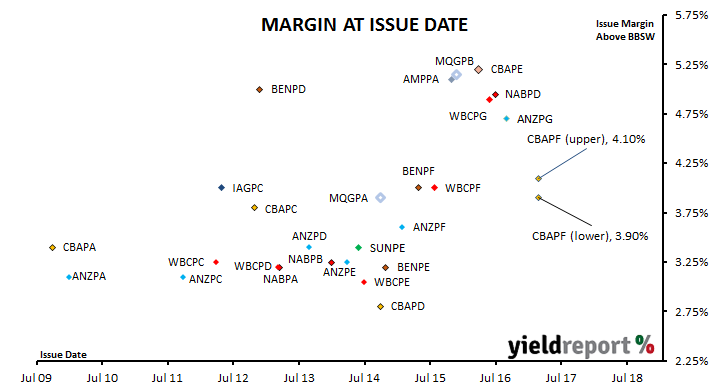

The chart below shows the history of issue margins of hybrid securities over the last eight years, including the GFC period in 2008/2009. The new capital notes are shown at both the lower end of the indicative margin (390bps) and the upper end (410bps).

Issue margins are set with an eye to current market conditions and margins of comparable hybrids already trading. Prices for securities change as soon as trading begins, whether it is on an organised market such as the ASX or an over-the-counter (OTC) market. Other securities issued at different margins may have fallen (or risen) in price, which generally means their trading margin will have changed. The new CBA hybrids are likely to have a margin set at the same rate as Macquarie Group Capital Notes which were issued in September/October 2014. The rate is substantially lower than new issue margins in the last 12 months and back to the top end of the 300bps-400bps range which existed from 2011 to mid-2015. The second chart below shows the trading margins of comparable securities which trade on the ASX as at the close of business 20 February 2017, as well as the new hybrids at both the lower and upper ends of the indicative margin range.