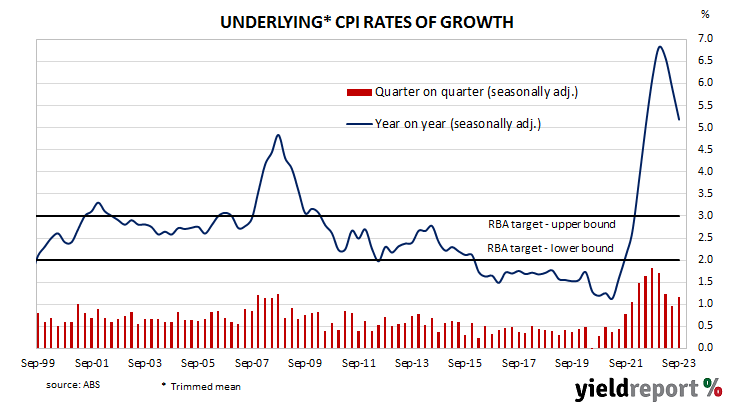

Summary: Annual Inflation rate slows to 5.4% in September quarter, above expectations; RBA preferred measure slows from 5.9% to 5.2%; ACGB yields rise, especially at short end; rate-rise expectations harden; housing, transport main drivers of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

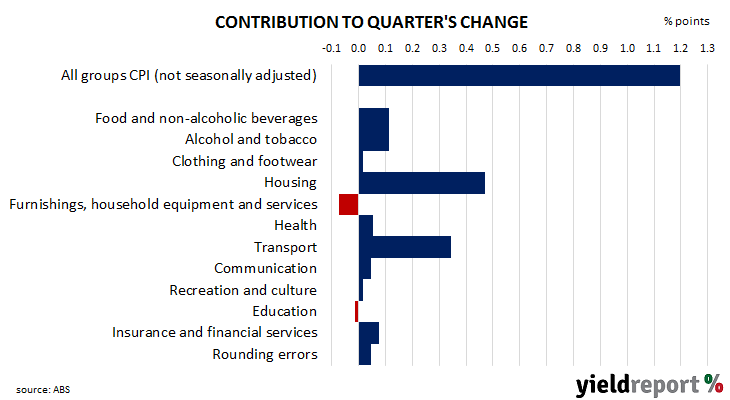

Consumer price indices for the September quarter have now been released by the ABS and the inflation rate posted a 1.2% rise before seasonal adjustments. The result was above consensus expectations of a 1.1% rise as well as the June quarter’s 0.8% increase. On a 12-month basis, the rate slowed from 6.0% to 5.4%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.2% over the quarter, more than the 1.1% increase which had been generally expected as well as the June quarter’s 1.0% rise after revisions. The 12-month inflation rate slowed from 5.9% to 5.2%.

Domestic Treasury bond yields moved higher on the day, especially at the short end. By the close of business, the 3-year ACGB yield had gained 10bps to 4.27%, the 10-year yield had added 3bps to 4.74% while the 20-year yield finished 1bp higher at 5.06%.

In the cash futures market, expectations regarding further rate rises hardened. At the end of the day, contracts implied the cash rate would increase from the current rate of 4.07% to average 4.205% through November, 4.30% in December and 4.37% in February. May 2024 contracts implied a 4.435% average cash rate while August 2024 contracts implied 4.42%, 35bps more than the current rate.

The main driver of the headline inflation figure in the quarter was a 2.2% rise in housing costs, contributing a little over 0.45 percentage points of the 1.2% (unadjusted) increase. Transport costs also had a significant effect on the quarter’s reading, contributing nearly 0.35% percentage points to the quarterly total.

Here’s what a few economists said about the figures:

Justin Smirk, Westpac

Overall, the momentum in both the Quarterly and the Monthly CPI Indicator was somewhat stronger than we expected, suggesting that inflationary pressures may not be moderating as fast as we had hoped.

Catherine Birch, ANZ

There was a broad-based reacceleration on a quarterly basis across several important measures, suggesting the weaker Q2 result might not have been indicative of the underlying trend.

Rodrigo Catril, NAB

Notably too, details suggest domestically sensitive components are the main driver of inflationary pressure. NAB continues to expect a hike in November, and for the tightening bias to remain.

Chris Read, Morgan Stanley Australia

Detail in the print showed disinflation continues to be driven more by core goods than core services. Importantly, there are still significant and temporary drags from government subsidies; electricity rebates are reducing prices by 13%, new childcare subsidies reduced costs by [around] 20% in the quarter and the Commonwealth rent assistance increase of 15% contributed to some sequential slowing in the quarter. All are temporarily contributing to somewhat lower headline inflation momentum and therefore a stronger underlying pulse.