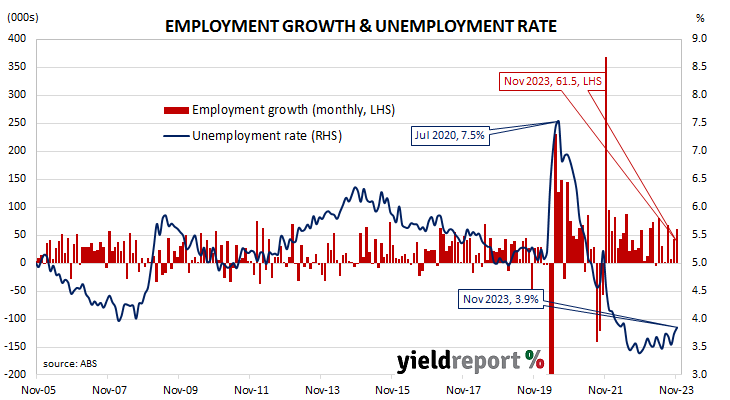

Summary: Employment up 61,500 in November, greater than expected; ANZ: labour market remains robust, supported by annual population growth of 3%; Citi: strong labour supply growth only marginally outstripping labour demand; participation rate rises to record high of 67.2%; jobless rate rises to 3.9%; more part-time, full-time jobs; aggregate work hours flat; underemployment rate up from 6.3% to 6.5%.

Australia’s period of falling unemployment came to an end in early 2019 when the jobless rate hit a low of 4.9%. It then averaged around 5.2% through to March 2020, bouncing around in a range from 5.1% to 5.3%. Leading indicators such as ANZ-Indeed’s Job Ads survey and NAB’s capacity utilisation estimate suggested the unemployment rate would rise in the June 2020 quarter and it did so, sharply. The jobless rate peaked in July 2020 but fell below 7% a month later and then trended lower through 2021 and 2022.

The latest Labour force figures have now been released and they indicate the number of people employed in Australia according to ABS definitions increased by 61,500 in November. The result was considerably greater than the 10,000 increase which had been generally expected and more than October’s 42,700 gain after revisions.

“The increase in employment was above market expectations and suggests that the labour market remains robust, supported by annual population growth of 3%,” said ANZ senior economist Blair Chapman. “That said, sample rotation may have contributed to the strength with full-time employment among the incoming rotation group materially stronger than that of the outgoing group.”

Domestic Treasury bond yields fell heavily on the back of large falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had shed 18bps to 3.76%, the 10-year yield had lost 15bps to 4.14% while the 20-year yield finished 14bps lower at 4.44%.

In the cash futures market, expectations regarding rate cuts over the next twelve months hardened. At the end of the day, contracts implied the cash rate would remain close to the current rate of 4.32% and average 4.305% in January and 4.315% in February. However, May contracts implied a 4.16% average cash rate, August contracts implied 4.005% while November contracts implied 3.845%, 47bps less than the current rate.

“The fact that such strong labour supply growth is only marginally outstripping labour demand is proof that despite the loosening, the labour market is still tight,” said Citi economist Faraz Syed. “Forward looking indicators also suggest that while employment growth could slow, it’s unlikely to collapse and lead to large-scale job-shedding. Indeed, the increase in the unemployment rate this year has been driven by higher participation, and not job losses.”

The participation rate rose from October’s figure of 67.0% to 67.2%, a record high, as the total available workforce increased by 80,300 to 14.830 million while the number of unemployed persons rose by 18,800 to 572,000. As a result, the unemployment rate increased from 3.7% to 3.9%.

The aggregate number of hours worked across the Australian economy remained unchanged in percentage terms even as 4,500 residents gained part-time positions and 57,000 residents gained full-time positions. On a 12-month basis and after revisions, aggregate hours worked increased by 1.6% as 182,900 more people held part-time positions and 258,600 more people held full-time positions than in November 2022.

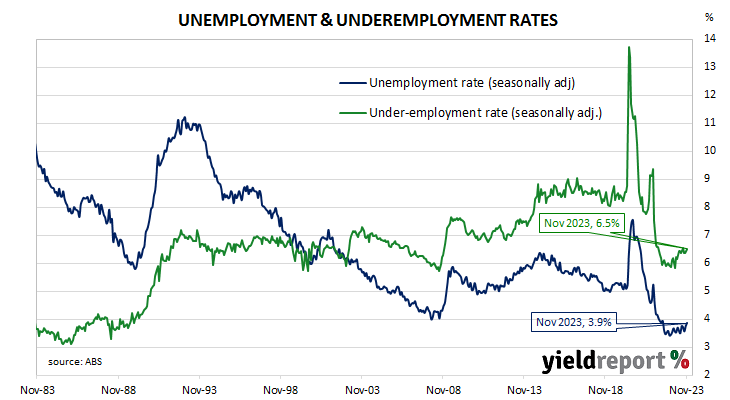

More attention has been paid to the underemployment rate in recent years, which is the number of people in work but who wish to work more hours than they do currently. November’s underemployment rate rose from October’s figure of 6.3% to 6.5%, 0.7 percentage points above this cycle’s low.

The underutilisation rate, that is the sum of the underemployment rate and the unemployment rate, has a strong correlation with the annual growth rate of the ABS private sector wage index when advanced by two quarters. November’s underutilisation rate of 10.4% corresponds with an annual growth rate of about 4.0%.