On 21 December 2015, it was reported that James Packer had resigned from the board of Crown Resorts. This news came just days after markets were speculating that he had instigated discussions with private equity groups and pension funds about privatising the gaming and entertainment company. Packer’s 53% stake in Crown is worth around $5 billion.

While the news provided a boost to the Crown share price, it has had the opposite effect on the two ASX-listed Crown subordinated hybrid notes that have since fallen substantially. It is speculated that any move to privatise Crown would likely be funded with debt, thus increasing the risk for hybrid note holders as it would decrease the creditworthiness of the company. The added risk is that the hybrid notes – both of which are considered ‘perpetual’ with a maturity dates beyond 2070 – will not be redeemed at the ‘first call’ dates of 2018 and 2021.

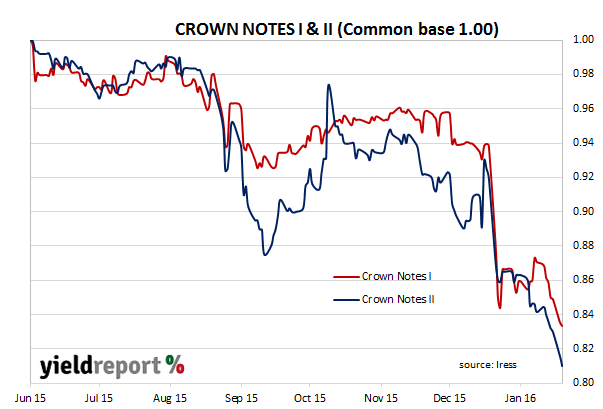

One interesting aspect of the fall has been how the recently issued series 2 notes (ASX code CWNHB), closed on January 19th at $81, down 19% on the $100 issue price. The series 1 notes (ASX code CWNHA) are “only” down 11.74%.

The difference in the discount to face value of each has led to further speculation as to why. In order to assess this it’s worth looking at the price movements of each from the listing date of the series 2 notes. By and large the two series have moved in tandem, although it is clear there are periods when the series 2 notes alone have been sold heavily. To some degree this is the case now and the gap between the two has widened.