On 15 Feb, YieldReport reported CBA’s likely new issue of a hybrid security after the bank flagged a capital raising in last week’s half yearly report. On 16 Feb, the bank confirmed it is seeking to raise $1.25 billion, with provision for over-subscriptions. The PERLS 8 Capital Notes, as they will be known, are subordinated unsecured notes and are Basel 3 compliant, which means they have the obligatory Capital Trigger Event or Non-Viability Event clauses (which triggers conversion into ordinary shares in the event the bank finds itself in financial distress).

As with any security of this sort, the three main points for investors to consider are the security of the issuer, the time until maturity and the expected return.

There’s no problem with the issuer. Commonwealth Bank was ranked the 11th largest bank in the world by market capitalisation in 2015, is very profitable and has a AA- credit rating from Standard & Poor’s, which is as good as it gets for banks nowadays.

The new securities will have a call date in October 2021 and a mandatory exchange date in October 2023. Redemption on the first call date is an accepted convention (although may not always be the case) and therefore it is anticipated the new PERLS will have 5.5 years to maturity. This becomes important when calculating a yield-to-maturity.

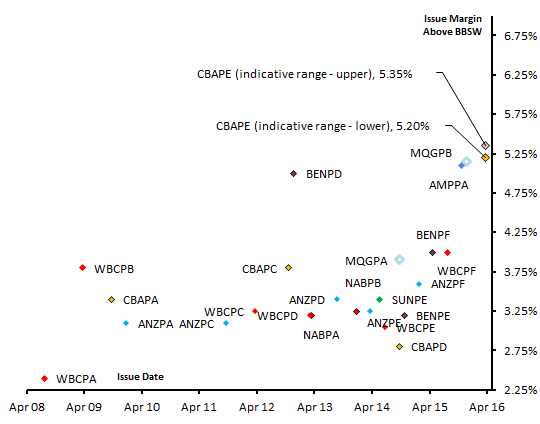

The issue margin has been indicated at BBSW* + 5.20% to 5.35%. With BBSW presently at around 2.30% this will return investors around 7.50% to 7.65% per annum before tax (i.e. this return is the gross amount including franking credits). On face value this appears to be a healthy return and well above the most recent bank issues in December from the lower rated AMP Capital and Macquarie at BBSW + 5.10% and 5.15% respectively. These issues were of Additional Tier 1 capital which is the same as to the proposed CBA issue.

From the chart below you can see how the issue price of the CBA hybrids are at the highest level for over 20 years for a major bank.