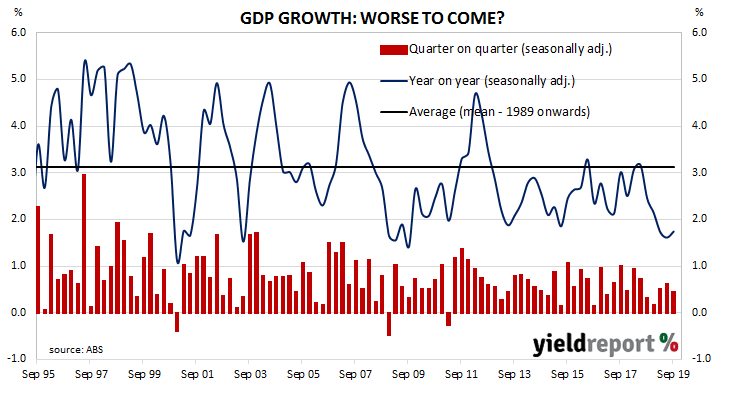

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. Australia even managed to avoid two consecutive quarters of negative growth in the GFC period. However, rates of growth in recent quarters have fallen below 2%, back to rates comparable to the GFC period. Forward-looking indicators have also been weakening, to the point where the RBA has cut the cash rate several times in 2019.

Figures released by the ABS indicate September quarter GDP grew by 0.4%, less than the 0.5% increase which had been expected and less than the June quarter’s +0.6%. However, on an annual basis, GDP increased by 1.7%, up from the June quarter’s comparable figure of 1.6% after revisions.

Westpac chief economist Bill Evans said, “Of most concern is that this represents the fifth consecutive quarter where private final demand, which declined by 0.3% in September, either contracted or was flat.” Commonwealth bond yields took a dive, largely as a result of following US Treasury yields which had dropped heavily in overnight trading. By the end of the day, 3-year Treasury bond yields had fallen by 9bps to 0.68%, the 10-year yield had shed 13bps to 1.06% and 20-year yields finished 14bps lower at 1.47%.

Commonwealth bond yields took a dive, largely as a result of following US Treasury yields which had dropped heavily in overnight trading. By the end of the day, 3-year Treasury bond yields had fallen by 9bps to 0.68%, the 10-year yield had shed 13bps to 1.06% and 20-year yields finished 14bps lower at 1.47%.

Prices of cash futures contracts moved to incorporate a hardening of expectations of another cut in the cash rate target. By the end of the day, February contracts implied a 70% chance of another 25bps rate cut, up from the previous day’s 53%. March contracts implied an 89% chance of a cut, up from 66% while May continued to fully price in another rate reduction.