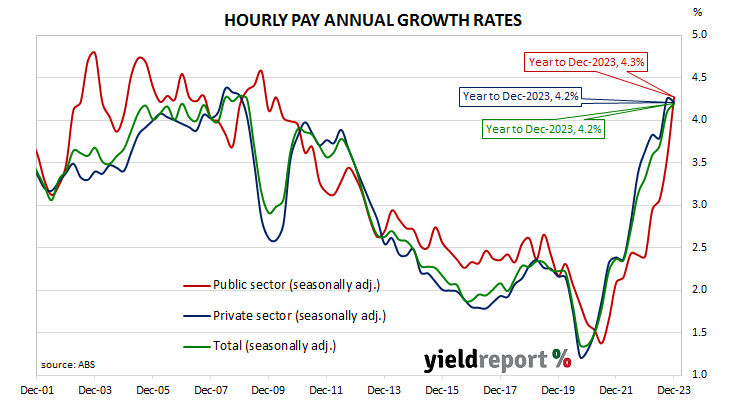

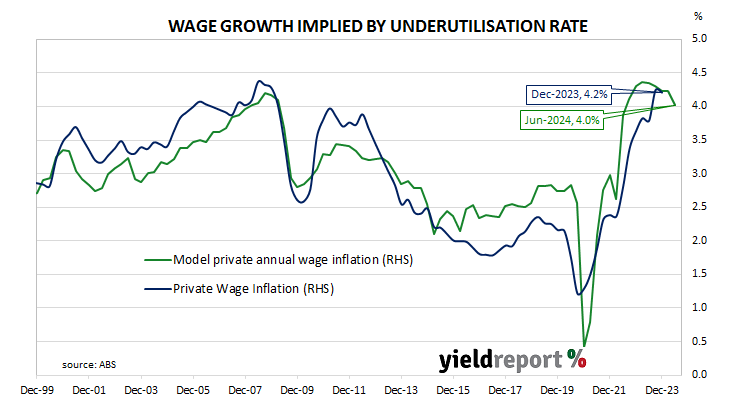

Summary: December quarter WPI up 0.9%, in line with expectations; annual growth rate rises from 4.1% to 4.2%; UBS: public sector wage growth key driver of increase; ACGB yields decline modestly; rate-cut expectations firm; Westpac: labour market peaked in first half of 2023, still be historically tight but now in softening trend; private sector wages up 4.2% over year, public sector up 4.3%; January underutilisation rate suggests slowing private wage growth in short-term.

After unemployment increased and wage growth slowed during the GFC, a resources investment boom prompted a temporary recovery back to nearly 4% per annum. However, from mid-2013 through to the September quarter of 2016, the pace of wage increases slowed, until mid-2017 when it began to slowly creep upwards. After remaining fairly stable at around 2.2% per annum from September 2018 to March 2020, the growth rate slowed significantly in the June and September quarters of 2020. Growth rates then accelerated over the next three years.

According to the latest Wage Price Index (WPI) figures published by the Australian Bureau of Statistics (ABS), hourly wages grew by 0.9% in the December quarter. The result was in line with expectations but lower than the September quarter’s 1.3% increase. On an annual basis, the growth rate ticked up from 4.1% after revisions to 4.2%.

“The key driver in Q4-23 was public WPI, excluding bonuses, which boomed 1.3% month-on-month and 4.3% year-on-year,” observed UBS economist George Tharenou. “Indeed, in Q4, the ABS cited the public sector contribution to wage growth of 34% was ‘significantly higher’ than the usual contribution of 10-25%. It was also materially above the public sector WPI weight of around 21.5%.”

Domestic Treasury bond yields declined modestly on the day. By the close of business, the 3-year ACGB yield had lost 2bps to 3.72% while 10-year and 20-year yields both finished 1bp lower at 4.19% and 4.51% respectively.

In the cash futures market, expectations regarding rate cuts later this year firmed a little. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.305% through March, 4.295% in April and 4.265% in May. However, August contracts implied a 4.125% average cash rate while November contracts implied 3.97%, 36bps less than the current rate.

“With hours worked now in decline and underemployment rising, it is clear that the Australian labour market peaked in the first half of 2023 and while it may still be historically tight, it has now entered a softening trend,” said Westpac senior economist Justin Smirk. “We expect this trend to continue through 2024 which will see wage inflation from Individual Arrangements, and in the services industries in particular, continue to moderate and be a drag on aggregate wage inflation.”

Wages in the private and public sectors grew by 0.9% and 1.3% respectively in the quarter. Over the past 12 months, wages in the private sector increased by 4.2% while public sector wages increased by 4.3%. Annual wage growth in the two sectors had been at 4.3% and 3.5% respectively in the September quarter.

The “underutilisation rate” is simply the sum of the unemployment and underemployment rates as per ABS monthly statistics. It has a good correlation with private wage growth two quarters in the future and thus it is useful as a leading indicator. However, differences can open up from time to time. January’s underutilisation rate suggests private wage growth will ease in the short-term.

Each quarter the ABS surveys around 3,000 private and public enterprises regarding a sample of jobs in each workplace to measure changes in the price of labour across 18,000 jobs. The results are used to construct the Wage Price Index in a manner similar to the construction of the Consumer Price Index (CPI). Changes in the WPI over time provide a measure of changes in wages and salaries, independently of the type or quantity of work.