In the early 1990s, entrenched inflation was broken by the “recession we had to have”, as it became known. Since then, “core” consumer price inflation has averaged around 2.6% which, coincidentally, is almost the midpoint of the RBA’s target range of 2%-3%. However, it has trended lower and lower since 2009 and it has not been above 2.0% since late 2015. With little sign of inflationary pressures, the RBA has decided to experiment with a near-zero cash rate in a non-recessionary environment.

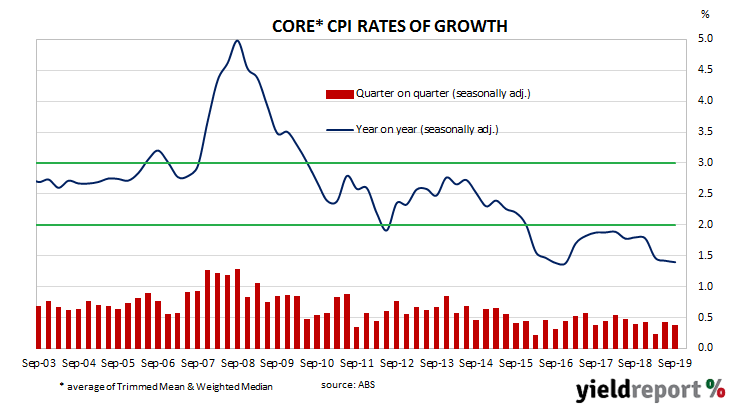

Figures for the September quarter have now been released by the ABS and both the headline and seasonally-adjusted figures were in line with their respective expected increases. The headline inflation rate was +0.5% for the quarter, down from the June quarter’s +0.6% while the seasonally-adjusted inflation rate slowed from +0.8% to +0.3%. On a 12-month basis, both headline and seasonally-adjusted inflation registered 1.7%, both having recorded 1.6% growth rates in the June quarter. The RBA’s preferred measure of core inflation, the “trimmed mean”, remained at the same rate on a quarterly basis and an annual basis. The trimmed mean inflation rate for the September quarter was +0.4%, in line with the market’s expected figure and the same as in the June quarter. The 12-month growth rate also remained unchanged at 1.6%.

The RBA’s preferred measure of core inflation, the “trimmed mean”, remained at the same rate on a quarterly basis and an annual basis. The trimmed mean inflation rate for the September quarter was +0.4%, in line with the market’s expected figure and the same as in the June quarter. The 12-month growth rate also remained unchanged at 1.6%.

Investors and traders reacted by sending local bond yields lower, even though the figures were largely as expected and US Treasury yields had hardly budged overnight. By the end of the day, 3-year ACGB yields had lost 2bps to 0.78% while 10-year and 20-year yields had each shed 5bps to 1.14% and 1.53% respectively. The local currency moved a little lower after the report’s release but finished the afternoon session at around 68.65 US which is roughly where it was prior to the report’s release.

Contract prices in the cash futures market moved in a way which implied a lower probability of a rate cut in coming months. November cash contracts implied just a 7% probability of a 25bps cut, down from the previous day’s 14%. The implied probability of a rate cut at December’s meeting fell from 40% to 35% while February contracts finished the day implying a 65% likelihood, down from the previous day’s 67%.