Inflation was once a problem in Australia. Through the 1970s and 1980s, consumer inflation regularly exceeded 5%, even though real GDP growth rates were on the low side and far from buoyant levels. This combination of high inflation rates and low economic growth rates was termed “stagflation” and it existed in most advanced economies at the time. In the early 1990s, entrenched inflation was broken by the “recession we had to have” as it became known. Since then, consumer price inflation has averaged around 2.4%.

Figures for the December quarter have now been released by the ABS and the headline number was stronger than the expected 0.4% increase, while the seasonally-adjusted figures were in line. The headline inflation rate was 0.5% for the quarter while seasonally-adjusted inflation came in at 0.4%. On a 12-month basis, headline inflation registered 1.8%, down from 1.9% in the September quarter, while the seasonally-adjusted rate fell back from September’s revised figure of 2.0% to 1.8%.

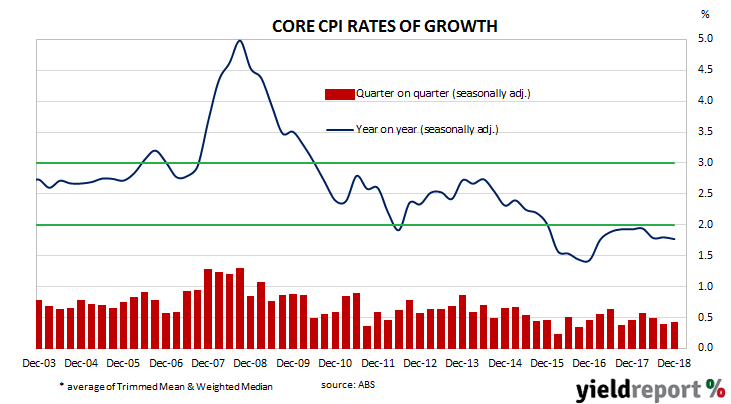

“Core” inflation measures favoured by the RBA, such as the average of the “trimmed mean” and the “weighted median”, remained unchanged on both a quarterly and annual basis. The average of the two measures was in line with the market’s expected figures of 0.4% for the quarter and 1.8% for the year. Westpac senior economist Justin Smirk said, “While this report does suggest we have at least found a bottom in the disinflationary pulse, it is still too early to call an inflationary pulse is underway and there are some hints in the December 2018 report that the current scenario has much longer to run.”

Westpac senior economist Justin Smirk said, “While this report does suggest we have at least found a bottom in the disinflationary pulse, it is still too early to call an inflationary pulse is underway and there are some hints in the December 2018 report that the current scenario has much longer to run.”

Financial markets reacted by sending local bond yields and the Aussie dollar higher, ignoring lower yields in US markets. By the end of the day, 3-year ACGB yields were 3bps higher at 1.74%, 10-year yields had inched up 1bp to 2.24% and the yield on 20-year ACGBs had gained 2bps to 2.61%. The local currency jumped from 71.50 US cents to 71.80 US cents and then finished the afternoon session at around 71.95 US cents.