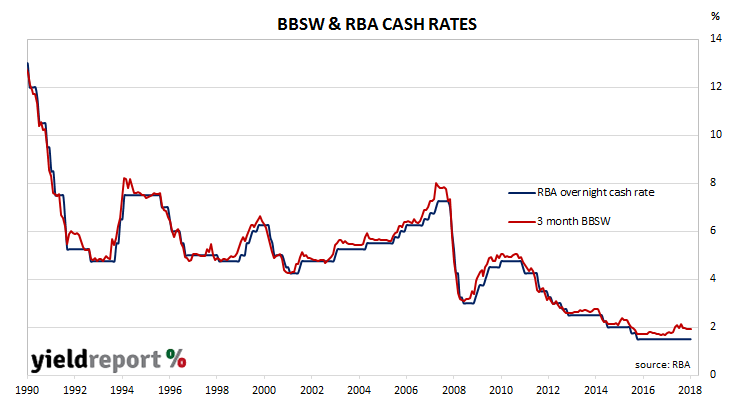

The RBA’s official interest rate has been at a historical low after the RBA reduced the cash rate from 2.0% to 1.5% in two steps in May 2016 and August 2016. While the ECB and the US Fed slashed their respective official rates to zero (or below) in the aftermath of the GFC, Australia’s central bank took a different path as Australia’s economy largely withstood the catastrophic falls in confidence faced elsewhere.

Since the RBA’s last rate adjustment, some commentators have called for it to be cut further, arguing a lower rate would be required to increase GDP growth and inflation to the RBA’s objectives. Other commentators have called for it to be increased given the apparent contradiction between a low rate and a non-recessionary economy.

The RBA has noted both positions in its discussions at the November Board meeting. “Arguments in favour of an increase in the cash rate included that the economy had more momentum than assessed by the Bank; financial stability risks from high levels of household debt required higher interest rates; and a higher cash rate would create room to cut the cash rate in future in response to an adverse event. The prime argument in favour of a decrease in the cash rate was that easier monetary policy could lead to faster progress in achieving the Bank’s monetary policy objectives.”

The RBA has noted both positions in its discussions at the November Board meeting. “Arguments in favour of an increase in the cash rate included that the economy had more momentum than assessed by the Bank; financial stability risks from high levels of household debt required higher interest rates; and a higher cash rate would create room to cut the cash rate in future in response to an adverse event. The prime argument in favour of a decrease in the cash rate was that easier monetary policy could lead to faster progress in achieving the Bank’s monetary policy objectives.”