Summary

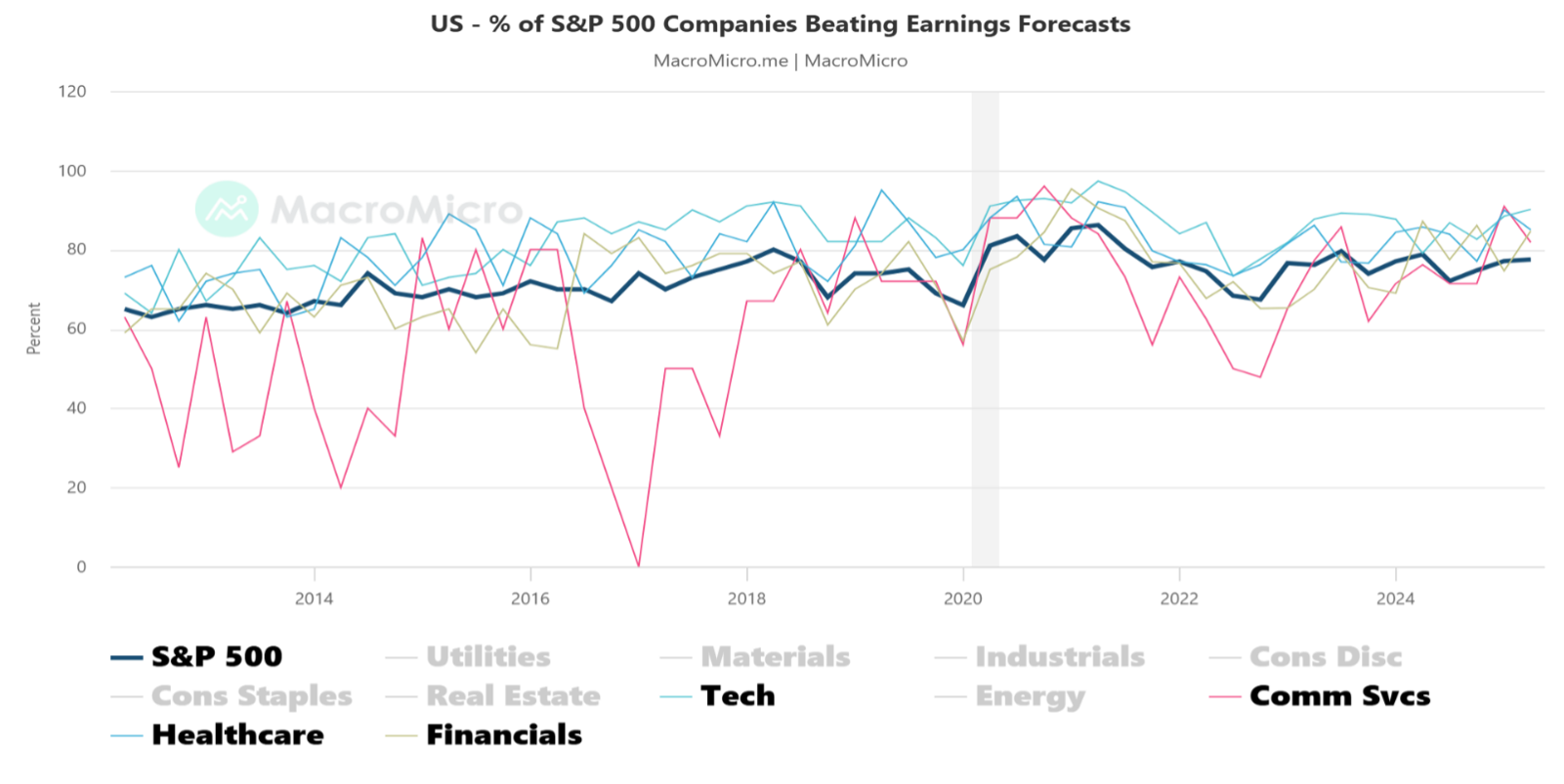

The Q2 U.S. earnings season delivered one of the strongest performances in recent years, providing powerful fundamental support for equity markets despite ongoing tariff uncertainty. A record 80% of S&P 500 companies beat analyst expectations, the highest rate in 12 months and well above the long-term average of 65–70%. Corporate profitability proved remarkably resilient, with earnings per share (EPS) growth accelerating to 10.7–11.8% year-over-year, more than double the initial 3–5% forecasts. This upward revision highlighted both the strength of U.S. business fundamentals and investor confidence in the face of global economic headwinds.

Sectoral Perspectives

The sector breakdown revealed that technology and financials were the clear leaders of the earnings expansion. Tech giants, including Meta, Google, Apple, and Microsoft, outperformed by an average of 10%, propelling the broader market. Communication services and information technology were the primary contributors to S&P 500 growth. On the financial side, JPMorgan Chase, Citi, and Goldman Sachs beat consensus forecasts by 15–18%, capitalizing on higher interest rate spreads and robust capital markets activity. In sharp contrast, the energy sector posted a double-digit EPS decline, weighed down by weaker oil prices, underscoring the uneven nature of earnings momentum across industries.

Exhibit 1: US Earnings Beats by Sector

Exhibit 2: US Earnings Growth by Sector

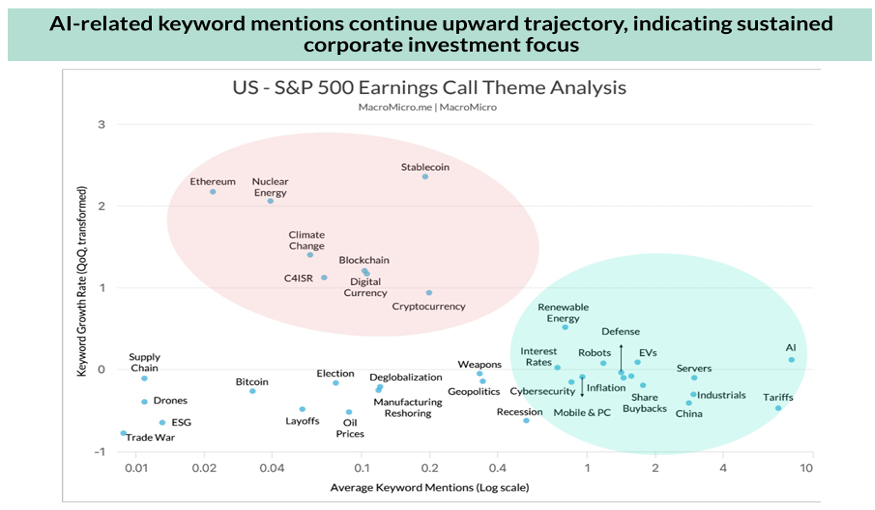

AI is a Dominant Theme

Beyond the numbers, AI remained the dominant corporate theme throughout earnings calls. Mentions of AI-related keywords such as servers, automation, and robotics continued their steep ascent, reflecting a sustained focus on capital allocation toward AI infrastructure. Rising technology capex, expanding data center construction, and accelerating adoption rates reinforced confidence in the AI investment cycle and countered concerns of a speculative bubble. At the same time, mentions of tariffs and recession risks declined, signalling stronger corporate confidence and successful cost management. Interestingly, the non-cyclical consumer sector exceeded expectations, shifting from a projected 5% decline to a 3–5% gain, while industrials and materials leveraged pricing power to protect margins.

Exhibit 3: AI Theme Dominates

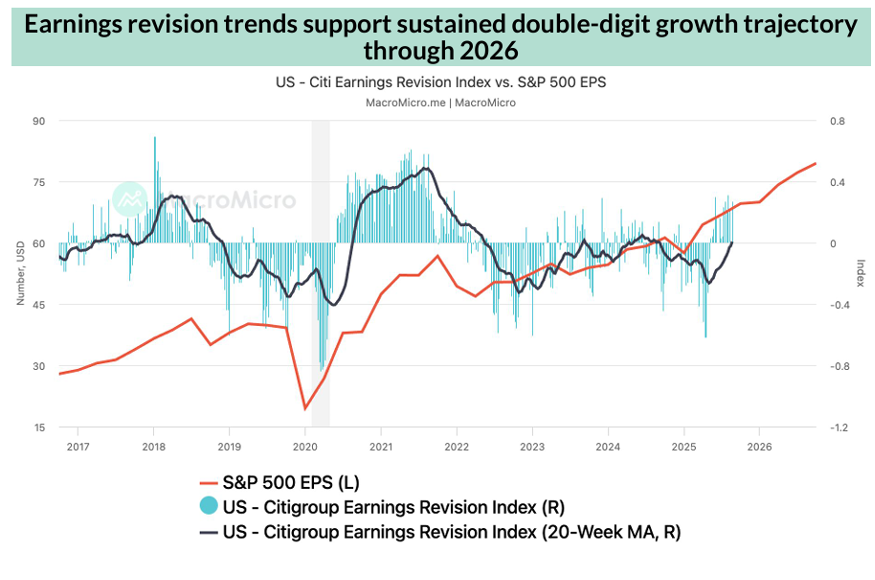

Outlook

Looking forward, the momentum is expected to persist. Consensus forecasts project earnings growth of 13.0% in Q3 and 13.7% in Q4, extending the double-digit trajectory. For the full year 2025, EPS growth is anticipated at 10.7%, rising further to 16.4% in 2026. Crucially, around 80% of sectors now show rising earnings forecasts, pointing to broad-based resilience rather than narrow sectoral strength.

Policy developments are also shaping the corporate narrative. Mentions of stablecoins, nuclear energy, and defense technology rose notably, reflecting Trump administration initiatives such as the GENIUS Act on cryptocurrency regulation, executive orders supporting nuclear power, and elevated military spending. Meanwhile, market concentration continues to grow, with the Magnificent Seven reaching a record 34.7% of S&P 500 market capitalisation, highlighting both their dominance and the increasing reliance of overall market performance on mega-cap tech firms.

Exhibit 4: Earnings Momentum Sustains