By guest contributor Ken Atchison, CEO, Atchison Consultants

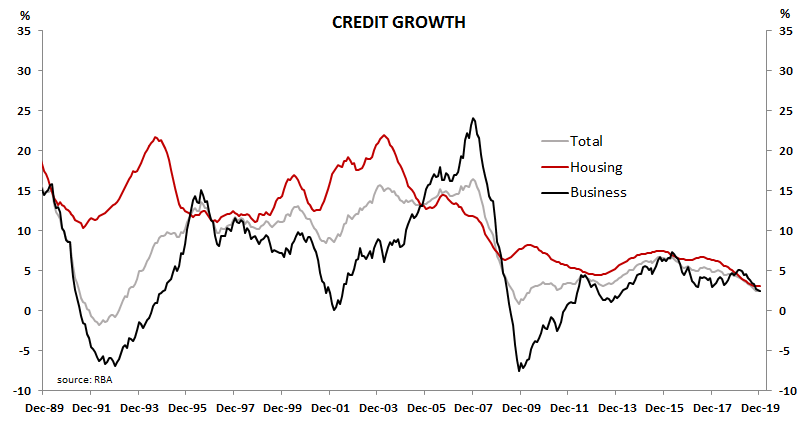

Despite very low official interest rates at 0.75%, lending for owner-occupied housing is the only sector experiencing material growth. Growth in investor loans remains negative while business lending by banks is growing at a very low rate. Additionally, any growth is in lending for large businesses and lending for small businesses is not growing.

In aggregate, money growth is very slow. This means that the reductions in interest rates by the RBA are not having any impact on lending. Bank lending is being restrained by other means.

Private credit data to end December 2019 shows continuing very slow growth in Australia.

Chart 1