Summary: Headline inflation up 0.2% in Sep quarter, up 2.8% over year, slightly less than expected; annual rate of RBA preferred measure slows from 4.0% to 3.5%; ACGB yields rise modestly; rate-cut expectations soften slightly; transport prices main driver of result.

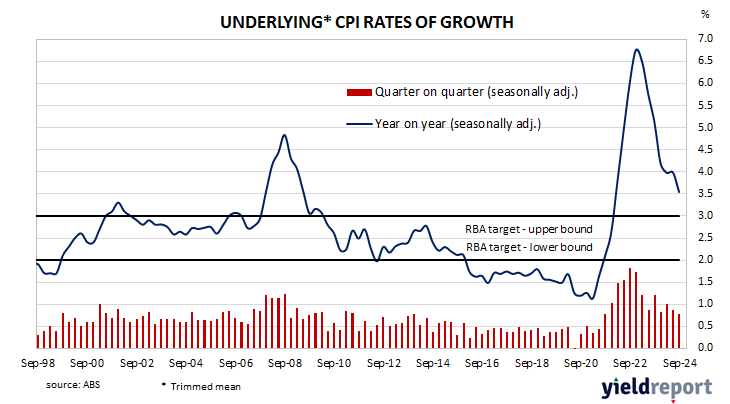

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

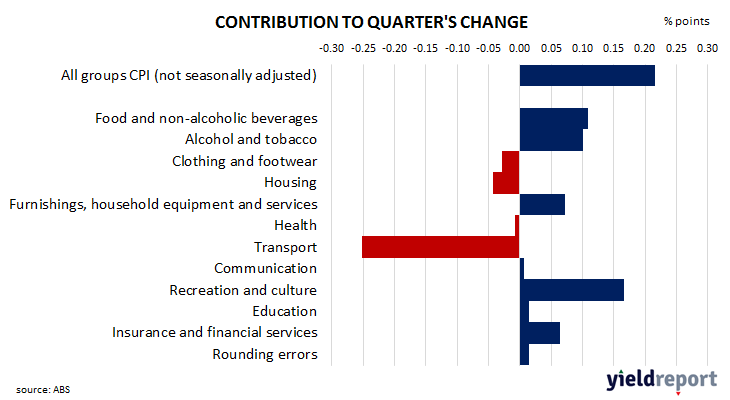

Consumer price indices for the September quarter have now been released by the ABS and the inflation rate came in at 0.2% before seasonal adjustments. The result was less than 0.3% rise which had been generally expected as well as the June quarter’s 1.0% increase. On a 12-month basis, the inflation rate slowed from 3.8% to 2.8%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.8% over the quarter, slightly more than the 0.7% increase which had been generally expected but slightly less than the June quarter’s 0.9% rise. The 12-month inflation rate slowed from 4.0% after revisions to 3.5%.

Domestic Treasury bond yields rose modestly across the curve on the day, in contrast with the modest declines of US Treasury yields on Tuesday night. By the close of business, 3-year, 10-year and 20-year ACGB yields had all gained 2bps to 3.95%, 4.48% and 4.83% respectively.

Expectations regarding rate cuts in the next twelve months softened slightly, with a February 2025 rate cut now viewed as less likely. Cash futures contracts implied an average of 4.33% in November, 4.305% in December and 4.265% in February 2025. September 2025 contracts implied 3.885%, 46bps less than the current cash rate.

The largest single effect of the headline inflation figure in the quarter came from a 2.2% fall in transport costs, contributing -0.25 percentage points to the total.

Here’s what a few economists said about the figures:

Josh Williamson, Citigroup

The Q3 CPI was largely in-line with expectations, with trimmed-mean inflation increasing by 0.8%, despite large number of utilities subsidies reducing headline inflation to a 0.2% rise over the quarter. In our view, while some housing and goods related inflation is showing signs of easing, it is only gradual, and services inflation remains sticky. This was further bolstered by still-strong administrative price increases, all implying that trimmed-mean inflation will remain outside the target band until H2 2025.

Catherine Birch, ANZ

We do not think the decline in trimmed mean inflation will be enough to convince the RBA it should begin the easing cycle this year, particularly as there does not appear to be an urgent need to support the labour market, given its resilience over recent months.

Justin Smirk, Westpac

Non-discretionary prices are where we have been finding inflationary pressures lurking but due to the cost-of-living assistance, prices here fell 0.1% in the September quarter taking the annual pace down to 2.9%, the slowest pace since March 2021. However, before we get too excited, we should note this follows a run of solid prints. The six-month annualised pace is still 4.7% at this stage and, as we are expecting to see cost-of-living assistance to come to an end, we should see a jump up in non-discretionary prices as we move into and through the first half of 2025.

Chris Read, Morgan Stanley Australia

The Q3 CPI broadly lines up with the RBA’s existing forecasts and narrative; headline CPI is being driven lower by volatile and temporary factors while outside of this, underlying disinflation remains relatively slow. Coupled with strong labour market data and continued government stimulus, we expect this will see the RBA continue patient messaging at its meeting next week, keeping rates on hold at 4.35%. Greater signs of disinflation, particularly across services categories, alongside more meaningful signs of labour market capacity, remain key to seeing the RBA shift to easing.