In recent years, when one of a company’s existing hybrids approaches its first call date (or first optional exchange date in this case), speculation turns to the likelihood of a replacement hybrid security. There is a sound basis for this speculation; most issuers of ASX-listed hybrids have replaced the hybrids which have been called. Now Suncorp is replacing its Convertible Preference Shares 3 (ASX code: SUNPE) securities which were first issued in May 2014.

Suncorp plans to raise $250 million via an issue of Capital Notes 2 (ASX code: SUNPH) securities, with the ability to raise more or less than this amount. The new securities will be perpetual, convertible, subordinated, unsecured notes and the proceeds will be used for “general corporate and funding purposes” as well as the partial refinancing of Suncorp’s “CPS 3” (ASX code: SUNPE) securities.

There are $400 million worth of SUNPEs on issue (in terms of their face value) and Suncorp has stated it “will consider converting, redeeming or reselling the outstanding CPS3 that are not reinvested in Capital Notes 3 on that date, subject to various factors…” One could expect Suncorp to issue more than $250 million of the new hybrids just to cover the need to finance the rollover into the new securities or the likely redemption/ resale of the remaining SUNPEs in June of next year.

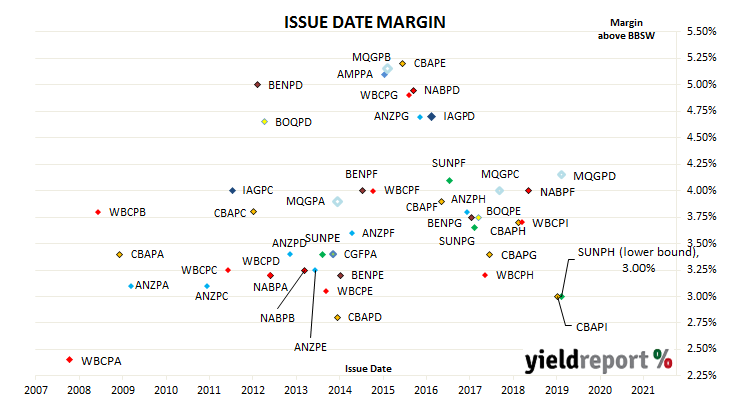

The new notes have some features in common with equities and some features in common with debt securities. Distributions are at the discretion of directors but they are calculated according to a set formula with reference to the $100 face value of the securities. The notes will qualify as Additional Tier 1 (AT1) capital under the Basel III bank regulatory framework, which means they have the now-standard “trigger event” clauses which may lead to early conversion into ordinary shares or a write-off of the capital notes should APRA require it. In the event Suncorp were wound up (and APRA had not already forced a write-off), its hybrids would rank above ordinary shares but below ordinary debt securities and other liabilities. The new capital notes have an indicative distribution rate equivalent to 3 month BBSW plus a margin of 300bps to 320bps, which is the same as the indicative margins of CBA’s PERLS 12 (ASX code: CBAPI). The final margin will be determined by a “book build” on 18 November 2019. A book build is a tender process managed by investment banks on behalf of the issuer in which investment institutions each place bids for a set volume at a price/yield. (This is the same way as the AOFM holds tenders to sell government bonds each week). If recent history is any guide, then the margin is likely to be set at the lower end.

The new capital notes have an indicative distribution rate equivalent to 3 month BBSW plus a margin of 300bps to 320bps, which is the same as the indicative margins of CBA’s PERLS 12 (ASX code: CBAPI). The final margin will be determined by a “book build” on 18 November 2019. A book build is a tender process managed by investment banks on behalf of the issuer in which investment institutions each place bids for a set volume at a price/yield. (This is the same way as the AOFM holds tenders to sell government bonds each week). If recent history is any guide, then the margin is likely to be set at the lower end.