By Alberto J. Boquin, research analyst, Brandywine Global Investment Management

The COVID pandemic highlights the quality differentials within the EM debt universe.

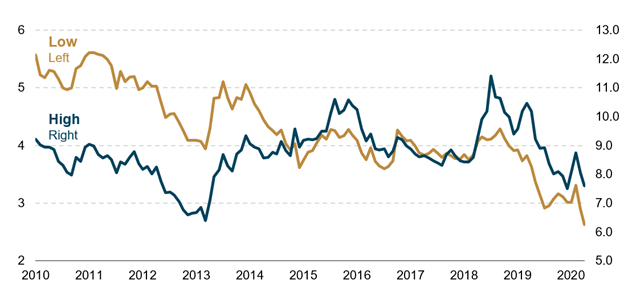

This year’s COVID shock accelerated a secular decline in interest rates around the world. Emerging market (EM) rates are no exception. The yield on the JP Morgan Emerging Market Local Currency Index (GBI-EM) declined to a series low of 4.6% compared to a 6.3% average in the prior decade. However, looking at the index can be misleading as there is plenty of dispersion beneath the surface. Higher-quality EMs have seen their interest rates converge toward developed market levels, but there remains a posse of lower-quality EMs where equilibrium rates continue to hover around the high-single digits (Chart 1).

Chart 1: GBI-EM High and Low Yielders

Yield to Maturity %, As of 6/18/2020

Source: Bloomberg Finance LP. Past performance is no guarantee of future results. Indexes are unmanaged, and not available for direct investment. Index returns do not include fees or sales charges. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

What differentiates the two groups? For starters, inflation-fighting credentials. It’s one thing to look at inflation in the present or even forecasts a year out. These are influenced by a number of temporary factors including the stage of the domestic business cycle, global oil markets and currency pass-through inflation. A cleaner measure for inflation credibility is the willingness of markets to lend a country money for a nominal fixed rate at long maturities. Some EMs have weighted average maturities of their debt of over 10 years while some have been forced to borrow at much shorter terms. See Chart 2.