By guest contributor Blair Kirkhope, Head of Specialist Investments, Sequoia Specialist Investments Pty Ltd

What is driving inflation?

We believe the major drivers of inflation over the last few years are as follows:

- Covid lockdowns crushing many supply chains and giving rise to shortages across various commodities;

- The global clean transition away from fossil fuels in response to climate change leading to oil and natural gas pipelines, oil drilling leases and coal fired power plants being cancelled or set for decommissioning;

- The Ukraine/Russia war and subsequent sanctions imposed on Russia and the impact this is having on the supply of natural gas, oil, nickel, and wheat to mention a few; the EU agreeing to ban 90% of all Russian oil imports by the end of 2022 is a good example. Will demand for oil be destroyed to the same extent to which it will be removed from the market by the end of the year, or will there be another source of supply entering the market which replaces that which is withdrawn due to the EU ban on Russian oil; and

- Increasing food protectionism as some Asian countries in particular prevent the export of various commodities reducing global supplies (e.g. India’s recent ban on wheat exports).

Will a rise in interest rates really bring inflation under control?

We further believe that unless the world suddenly sees a resolution to the conflict in Ukraine and a sudden backflip on global climate change policies, the above-mentioned inflation drivers are here to stay for the foreseeable future. This is the case especially for agricultural commodities and energy. Increasing interest rates will also do nothing to address these issues in our opinion. Interest rates can reduce demand but they do not fix disrupted supply chain or outright shortages. If anything, higher interest rates could further increase input costs for companies due to higher funding costs leading to higher consumer prices.

For these reasons, we believe high US inflation should therefore continue into at least the 2023/2024 period. As such, it can still make a lot of sense to consider an allocation to possible inflation hedging solutions until this fundamental picture changes.

What other asset classes can investors consider during a high inflationary environment?

So how can investors reallocate part of their portfolios to hedge against the impact of inflation? Rather than focusing on history for an answer to this question, lets focus on asset price movements over the last six months. The reason we prefer the approach is because the cause of inflation today is very different to the many high inflationary episodes of the past. i.e. Inflation today is caused by supply shortages and not excessive demand.

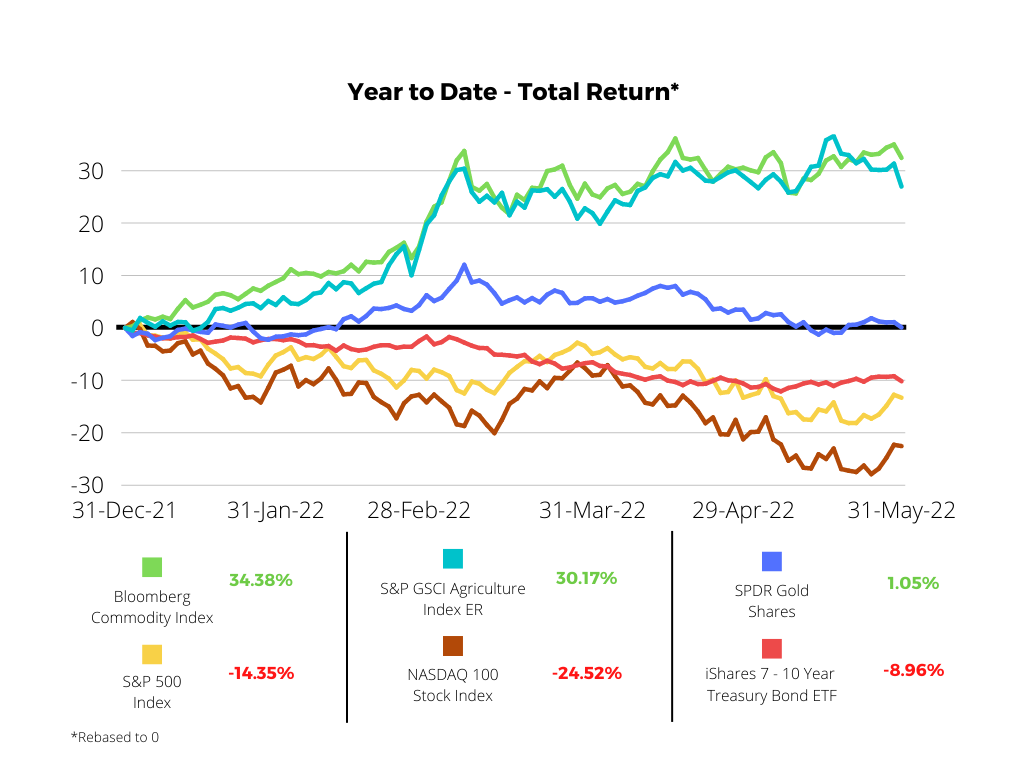

Firstly, we can say for certain that one asset class that has outperformed the rest since the highs formed in tech shares in November 2021 is commodities.

Source: Bloomberg. Past performance is not a reliable indicator of future performance.

The reason for this is obvious. If commodity prices are increasing then the cost of raw materials is increasing which leads to higher consumer prices. This is most obvious with energy and the cost of petrol, electricity and some food items. The fact that the US excludes food and energy from the calculation of CPI makes no difference. These are real world inflation measures.

How to invest in commodities

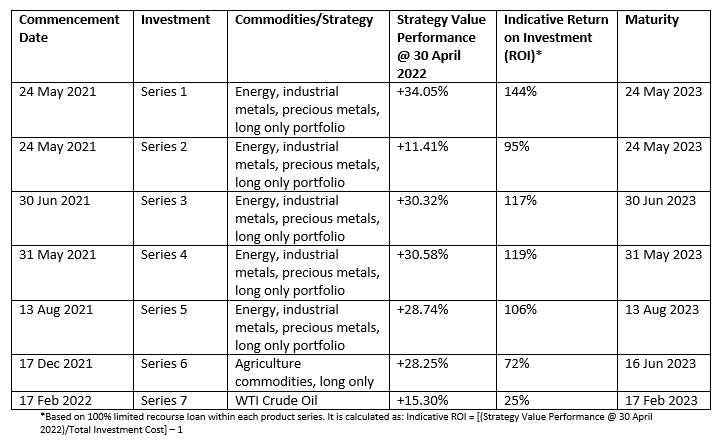

This for the most part can be rather difficult. Unfortunately, in Australia there is no direct commodity investment listed on the ASX. There are direct commodity ETFs listed in the US which can be considered, however, this may force investors to crystallize losses or lower potential gains on their equity or bond portfolios which many investors will be reluctant to do. To this end, Sequoia Specialist Investments have been offering a variety of commodity investment solutions over the last 12 months which require only a small portfolio allocation to obtain a much larger exposure. Please refer to the table for their performance as at 30 April 2022. For investment opportunities currently available from Sequoia Specialist Investments until 30 June 2022, please refer https://www.sequoiasi.com.au/

Key risks in relation to the investments listed above generally include the following:

- Risk of 100% loss or partial loss in relation to the Total Investment Cost and Upfront Adviser Fee specified in the Termsheet PDS or Termsheet IM;

- Significant timing risk because the Investment Term is fixed and the performance of the Strategy Value or Index (adjusted for changes in the AUD/USD exchange rate) needs to exceed the Total Investment Cost and Adviser Fee by the Maturity Date in order for investors to generate a profit;

- There is no guarantee that the Units will generate returns in excess of the Prepaid Interest and Fees, during the Investment Term;

- Gains (and losses) may be magnified by the use of a 100% Loan. However, note that the Loan is a limited recourse Loan, so you can never lose more than your Prepaid Interest Amount and Fees paid at Commencement;

For a full description of all the risks associated with each of the above listed investments, please refer to the relevant Termsheet PDS or IM and Master PDS or IM as per the relevant page of each investment found at https://www.sequoiasi.com.au/commodities/.

IMPORTANT INFORMATION

This article is written by Sequoia Specialist Investments Pty Ltd (ACN 145 459 936) (“SSI”). SSI is an issuer of structured investments that are arranged by Sequoia Asset Management Pty Ltd (ACN 135 907 550, AFSL 341506) (the “Arranger”). Investments in Sequoia Commodities Series can only be made by completing an Application Form attached to the relevant Term Sheet Product Disclosure Statement (“TSPDS”) or Term Sheet Information Memorandum (“TSIM”), after reading the Master PDS dated 14 August 2017 or Master IM dated 11 April 2019 and submitting it to Sequoia Specialist Investments Pty Ltd. A copy of the relevant Term Sheet PDS can be obtained by contacting Sequoia Specialist Investments Pty Ltd at invest@sequoia.com.au. If you are a retail investor you should consider the Term Sheet & Master PDS as well as the Target Market Determination before deciding whether to invest in any investment issued by Sequoia Specialist Investments Pty Ltd.

Sequoia Specialist Investments Pty Ltd declares that it deals in financial products as part of its’ business and consequently it may have a relevant interest in the investment strategies or financial products referred to herein. Sequoia Specialist Investments Pty Ltd provides General Advice only in its role as an issuer of investments arranged by Sequoia Asset Management Pty Ltd (ACN 135 907 550/AFSL 341506). General advice is advice which is provided to you without regard to any individual’s personal objectives, financial situation or needs. It is not specific advice for any particular investor and it is not intended to be passed on or relied upon by any person. Before making any decision about any general advice provided, you should consider the appropriateness of the general advice presented, having regard to your personal objectives, financial situation and needs. Any indicative information and assumptions used may change without notice to you, particularly if based on past performance.

Past performance is not a reliable indicator of future performance. Further, no representation is given, warranty made or responsibility taken about the accuracy, timeliness or completeness of information sourced from third parties.