By guest contributor Damien Wood, Spectrum Strategic Income Fund

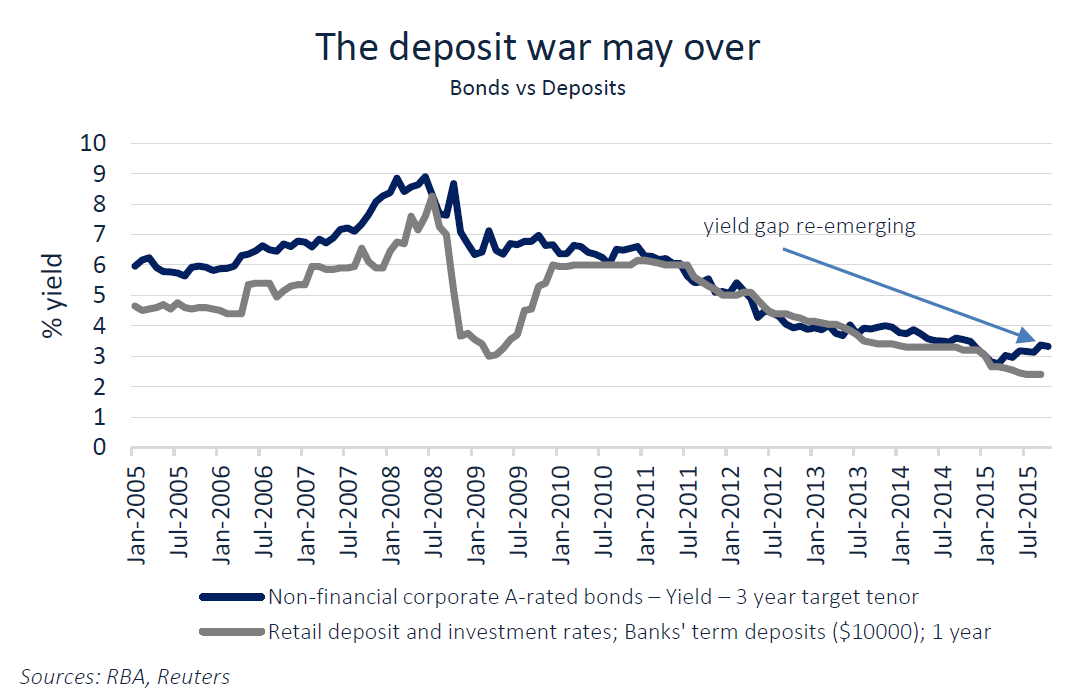

Australian superannuation investors have largely shunned corporate bonds. Post the GFC this was logical for many. Why invest in Australian corporate bonds when you could get the same yield for less risk and less hassle by sticking with Australian bank deposits? This rationale is changing however and low-risk short-dated corporate bond yields are now moving higher than those on deposits.

We see this as a return to “normal”. If sustained, as we expect it will be, corporate bonds may be part of the solution for those frustrated with current deposit rates.

Why the deposit premium?

The so called “deposit war” between banks appears to be either over or in a state of cease fire. The battle began during the GFC when there was heightened sensitivity to bank creditworthiness across the globe. For Australian banks, the key weakness was deemed to be too much funding dependence on foreign bond investors and not enough local deposits. “Encouraged” by regulators and credit rating agencies, the banks took steps to address this and in doing so, they raised the relative level of bank deposit rates and so began the deposit war.

The graph above shows that post the GFC, the yield on one year bank deposits was largely the same as one could get on a 3 year “A” rated corporate bond. Deposits, however, had some other appeal. These were and currently are, as follows:-

- Deposits up to $250,0001 carry a AAA/Aaa rated government guarantee

- Deposits over $250,000 with the big four banks have the higher Aa2 credit rating

- Deposits are shorter dated compared to the corporate bonds

- Deposits are relatively simple to invest in

Investors accordingly voted with their wallets and kept their superannuation out of fixed income and in equities and bank deposits.

Spectrum believes the recent deposit war was a large reason why Australian pension or superannuation funds have far less exposure to fixed income than their peers around the world.

For self-managed super funds, fixed income accounts for less than 1% of investments and investors do not so much shun fixed income as an investment class but rationally used deposits as an alternative for the reasons noted above.