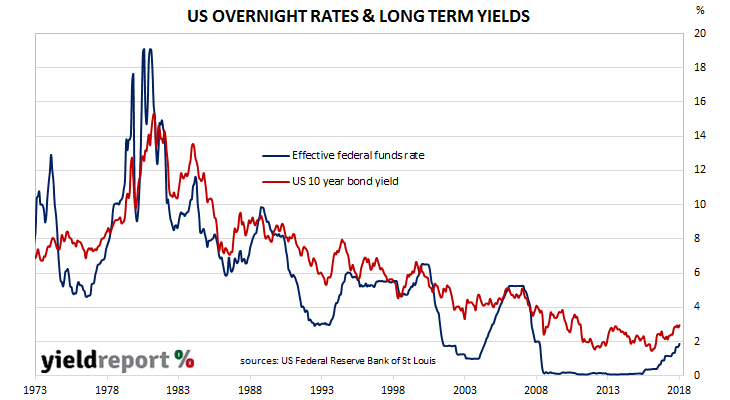

The US Federal Reserve began raising its official interest rate, known as the federal funds rate, in December 2015. Prior to the first increase of this economic cycle, the federal funds rate had been in a range of 0.00% to 0.25%, usually somewhere close to the mid-point. It had been set in this range back in 2009 when the US had gone into recession after a disastrous property boom which was accompanied by massive speculation in the US mortgage market.

After 2015, the US Fed waited another year before it raised its official interest rate again in December 2016. However, since then, it has raised rates another two times, once in March and one at this latest Federal Open Markets Committee (FOMC) meeting.

The change was expected, as for some time, prices of US futures contracts had built in a high probability of an increase at the June meeting. Fed officials had periodically referred to a need to normalise US interest rates from historically low levels and, through speeches and other comments, had left the market with very little uncertainty as to the Fed’s likely actions.

Although US bond yields and the USD initially moved higher, by the end of the day, yields were only a little higher and the USD was weaker against the yen and the euro. 2 year bond yields increased by 2bps to 2.56% and the 10 year yield inched up by 1bp to 2.97%. The USD finished around 0.2%-0.4% weaker against the yen and the euro but flat against sterling.

The 25bps increase takes the target range to 1.75% to 2.00% but the actual rate at which overnight lending between banks typically is at the mid-point of this range, at what is known as the “effective” rate.