By Ken Atchison – Atchison Consultants

Focus groups have been driving the spending decisions by the Victorian Government. The notion that financial policy should reflect outcomes from focus group surveys is extraordinary, but it is happening. Spending by the Victorian government has been extravagant and irresponsible. In the 2022/2023 budget, growth in spending continues with no regard to the debt burden on future generations. Net debt will grow to $167 billion in 2026 or higher if, as is likely, the current government commits to even more spending in the remainder of the current term.

A policy initially applied by the Victorian Government to limit debt to 6% of Gross State Product (GSP) has been simply discarded. This reflects the government view of financial responsibility. It will reach 26.5% of GSP in 2026.

There is no evidence of any coherent policy for servicing the increasing amounts of Victorian debt. This is particularly concerning as interest rates rise.

Increased debt has been the result of the Victorian Government’s actions. It persistently locked down Victoria and, to an even-greater extent, Melbourne, through the pandemic. This damaged economic activity and the financial consequences were never considered. Only increased private sector activity will drive sustainable higher government revenue.

Now the Victorian Treasurer is demanding a greater share of national GST as Victoria has been hardest hit by the pandemic. Acceptance of any responsibility for this outcome is absent. No acknowledgement of the financial consequences for all Australians from the Melbourne lockdowns has been forthcoming from the Victorian Government. There is no acknowledgement of the 9.7% increase in Federal Government grants to Victoria. The Victorian Government’s reaction has the hallmarks of a petulant adolescent complaining about an inadequate allowance.

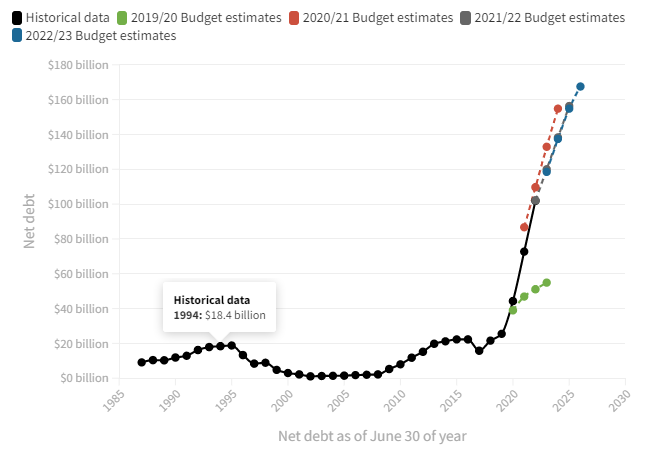

There is no recognition of the future decline in living standards for all Victorians which will occur from excessive debt. Victorian Government debt has grown at an extraordinary rate over the years since Labor’s election in 2014. This is shown in Chart 1 from The Age and the 2022/23 Budget Papers. Since Labor was re-elected in 2018, debt has exploded and will have grown by $147 billion to the projected $167 billion in 2026.

Chart 1: Net debt in Victoria over time

Government deficits emerge when excess spending occurs today for the benefit of individuals today. Responsibility for servicing falls on future generations. Today, deficits have arisen through draconian controls over activity in Victoria and by unconstrained spending. Eventually the debt level is unsustainable.

Projected Victorian debt in 2026 represents debt per person of $25,000, an increase of $20,850 per person from $4,150 in 2015 when this government was elected.

The population has declined by almost 45,000 in Victoria since the start of the pandemic. Private sector growth will be limited, reflecting business failures through lockdowns, lower employment and negative population growth, lower international student numbers and declining tourism.

Interest rates on debt have been at historic lows. This persisted as central banks, including the Reserve Bank of Australia, engaged in quantitative easing (QE), buying government bonds in secondary markets and therefore indirectly funding government deficits. However, QE is now being reversed in both the US and Australia.

Negative nominal and real interest rates only persisted because of central bank policies of QE. Historically, Commonwealth Government bonds have provided positive real returns. (A real return is the interest rate net of the inflation rate.)

The 10-year Commonwealth bond yield has risen from 1.6% to 3.5% as global yields have increased. Consumer price inflation in the March quarter in Australia was 5.1% and it is projected to rise further. Based on current Australian CPI, the 10-year bond yield offers a negative real yield of 1.6%.

Real yields on 10-year Australian Commonwealth Government bonds have historically ranged between 1.0% and 1.5%. Policy tightening by the RBA could result in 10-year bond yields in a range of 4.5% to 6.0%.

State government bond yields typically offer a premium of 0.3% above Commonwealth bond yields. This indicates interest rates on Victorian Government borrowings could increase to a range of 4.8% to 6.3%. Interest rates could be even higher should the credit rating of Victorian debt be downgraded further.

Rapidly increasing net debt, rising interest rates and a declining credit-rating status for Victoria will result in the interest-to-revenue rate increasing above 7% by 2026. With a previously stated target of 2%, such a rise indicates financial irresponsibility.

A reduction in public sector employment and public services in health, emergency services and education will occur. Government-sector employment expenses have grown at 8.5% per annum since Labor was elected in 2014, which is a real growth rate of 6.6% per annum.

Irresponsible financial management, especially when it leads to higher debt burdens, does matter. Moody’s concluded earlier this year that Victoria, uniquely in Australia, has a negative outlook.

Moody’s stated: “Despite the underlying strength of the Victorian and broader Australian economy we expect Victoria’s debt burden will not stabilise before the end of fiscal 2027, further increasing pressure on the state’s rating.”

The issues associated with Victoria’s poor position means future living standards have been put at risk.

Asset sales to reduce debt will be required. Privatisation of infrastructure projects will be necessary. New or increased taxes will be required. Public services will be terminated.