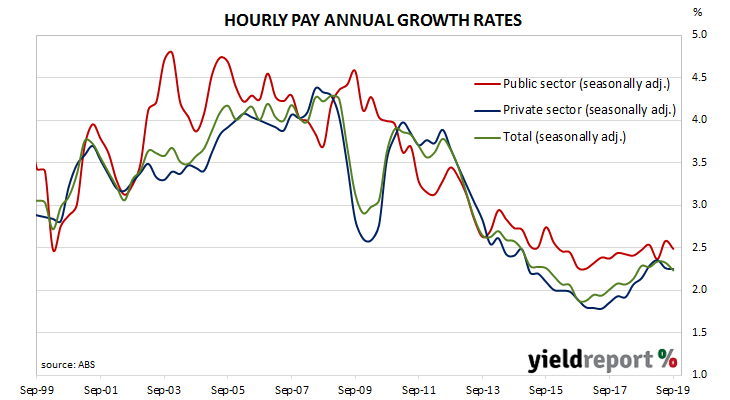

After unemployment increased and wage growth slowed during the GFC, a resources investment boom prompted a temporary recovery back to nearly 4% per annum. However, from mid-2013 through to the September quarter of 2016, the pace of wage increases slowed until mid-2017 when it began to slowly creep upwards. The latest report on aggregate wages indicates this slow process may be ending.

According to the latest wage price index (WPI) figures published by the ABS, hourly wages grew by 0.5% in the September quarter, in line with the expected figure and the same rate as in the June quarter. However, the year-on-year growth rate slipped for a second consecutive quarter, to 2.2%, after recording 2.3% in the June quarter.

ANZ senior economist Catherine Birch said slowing wages growth was “not unexpected” given the level of labour market underutilisation and lower wage increases in enterprise bargaining agreements “since late 2018.” The figures came out on the same day as the November consumer sentiment report but neither one made much of an impact on local Treasury bond yields. By the end of the day, the yield on 3-year ACGBs had lost 2bps to 0.83%, the 10-year yield had slipped 1bp to 1.28% while the 20-year yield finished unchanged at 1.69%.

The figures came out on the same day as the November consumer sentiment report but neither one made much of an impact on local Treasury bond yields. By the end of the day, the yield on 3-year ACGBs had lost 2bps to 0.83%, the 10-year yield had slipped 1bp to 1.28% while the 20-year yield finished unchanged at 1.69%.

In the cash futures market, traders reacted by slightly trimming the likelihood of further official rate cuts in 2019 and 2020. The implied probability of a 25bps cut at the RBA’s December meeting moved from 18% to 13% while February contracts eased a little from 53% to 51%. End of day prices of May 2020 contracts implied another cut in the cash rate target from 0.75% to 0.50% was viewed as an 81% probability.