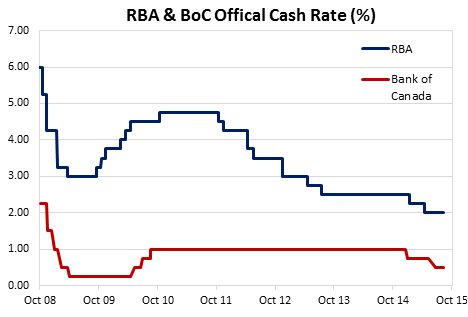

Canada and Australia are often viewed in similar terms because of their large land masses, relatively small populations, commonwealth heritage and, of course, their huge reserves of natural resources. Naturally it’s the last one that drives the economic outlook and the huge dive in energy and commodity prices has buffeted both countries with both having to make rapid adjustments for the end of the ‘once in a lifetime resources boom’.

The reported 0.5% decline in Canada’s second quarter GDP this week suggests Canada is in a technical recession as it follows a 0.8% decline in first quarter GDP. A recession is defined as two consecutive quarters of negative growth. The recessionary view is not universal as Canada’s employment rate has not fallen but most agree the short-term outlook remains poor.

Canada’s growth rate compares with US growth over the same period of 3.7% and makes Canada the only one of the G7 nations to be facing this issue.

The main culprits are Canada’s oil and mining sectors that have collapsed by 15.4% and 5.9% respectively. This has created a flow-on effect throughout the economy and is showing a disturbing similarity to the outlook in Australia.

Australia’s second quarter GDP figures were also released this week and at 0.2% for the quarter, were half the expected 0.4% by analysts. Annual growth fell to just 2.0%. Nominal GDP at 1.8% is the lowest since 1961/62. Growth in the first quarter was 0.9%. The ‘R’ word is beginning to enter the dialogue about our economic prospects.

The RBA in its 7 August release of the quarterly Statement on Monetary Policy said the Australian unemployment rate had peaked but that it expected the rate to remain relatively steady for the next 18 months. This was largely due to population growth slowing. Annual growth was expected to be between 2.00% and 3.00% in 2016 revised down from 2.5% to 3.5% previously.