By guest contributor Ethan Xing, analyst, Atchison Consultants

The focus of financial markets in 2018 has been on a number of eye-catching events, such as the “tit for tat” impositions of tariffs between US and China, the US Republican tax reforms and the US-North Korea summit. None of these issues seemed to weaken the US Federal Reserve’s resolve in tightening monetary policy.

So far in 2018, the US federal funds rate has been increased three times from 1.50% in early March to 2.25% in late September on the back of the strengthening US economic outlook. One more increase is expected in December 2018, with another two or three increases currently expected in 2019.

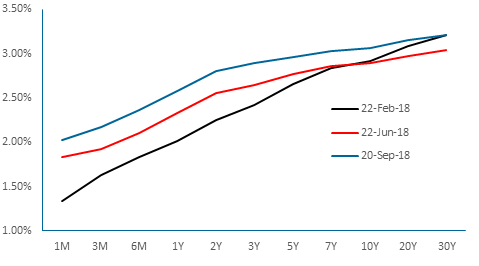

Unlike the short-term Fed rate, US long-term debt rates have been relatively static. This has led to a flattening of the US yield curve. Specifically, the spread between the yields of the 2 year Treasury note and the 10 year Treasury note narrowed down to a low of 26 basis points on 20 September 2018 from 67 bps on 22 February 2018 (Figure 1).

Figure 1. The flattening US yield curve

Source: US Treasury, Atchison Consultants