By guest contributor Ethan Xing, analyst, Atchison Consultants

Within the fixed-income sector, government bonds are the safest of safe assets to hold. They are issued by sovereigns, which have minimal default risks due to their taxation and security powers.

Credit securities also have a risk of capital loss when issuers default, but this risk is higher than that of government bonds as issuers do not have the taxation powers of governments. Hence, credit securities usually offer investors returns which are higher than the returns of government bonds.

However, there were several periods in history when credit securities have delivered lower returns than government bonds.

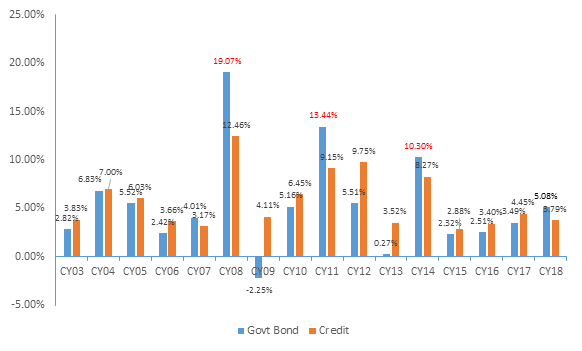

Chart 1 below shows total returns of Government bonds and corporate bonds, often referred to as “credit ” in professional circles, for the last 16 years. In this case, government bonds are represented by the Bloomberg AusBond Treasury Index and credit is represented by the Bloomberg AusBond Credit 0+ Yr Index.

Chart 1. Total Return of Bloomberg AusBond Treasury index and Bloomberg AusBond Credit 0+ Yr Index (2003 – 2018)

Source: Bloomberg, Atchison Consultants

As shown in Chart 1, in 5 out of 16 years from 2004 to 2018 government bonds outperformed credit. If insignificant outperformances are excluded, the frequency is down to 3 years. These figures are highlighted in red. The periods when the government bond index significantly outperformed credit are the years 2008, 2011 and 2014. What happened over these periods to make investors behave inconsistently with the “risk premium” rule of thumb?

These periods “coincided” with the Fed’s timeline of quantitative easing programmes (QE1, QE2 and QE3). QE1 started in November 2008 when the Fed announced a USD 600 billion programme of purchasing MBS. 2 years later in November 2010, QE2 kicked off with USD 75 billion longer-dated treasuries to be purchased every month until June 2011. QE3 began from September 2012 to December 2013 with the Fed purchasing USD 40 billion MBS and longer-dated treasuries on a monthly basis.