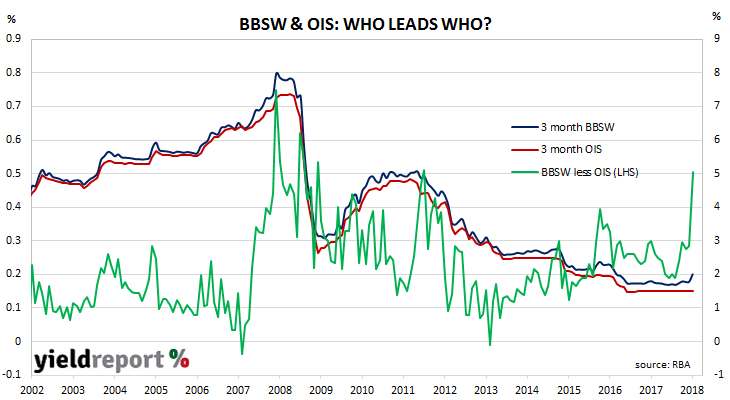

There has been quite a bit of commentary on the gap between BBSW and the official rate in recent weeks and Bill Evans, Westpac’s chief economist, joined the fray. He said the recent increase in the spread between BBSW and various overnight indexed swap rates (OIS) is not a sign bank risk has increased.

OIS may be viewed as a proxy for future RBA cash rates in a manner similar to cash futures prices. It has been largely unchanged and very close to 1.50% in recent months as cash rate increases have been largely discounted until 2019. BBSW, on the other hand, is also a leading indicator for future cash rates but it has increased by around 30bps-40bps since February. So, why the difference?

In the past, as these two rates tended to move in line with each other, any change in the BBSW-OIS spread had been indicative of a change in the market’s view of bank risk. A change in the expected path of the official rate typically led to changes in both rates and not just one or the other. A noticeable change in the spread of the two rates is therefore interpreted as indicative of something.