Commentary courtesy of Spectrum Asset Management’s Lindsay Skardoon.

| Close | Prev Close |

Change | |

| Aust. 90 day bank bill% | 1.79 | 1.79 | 0.00 |

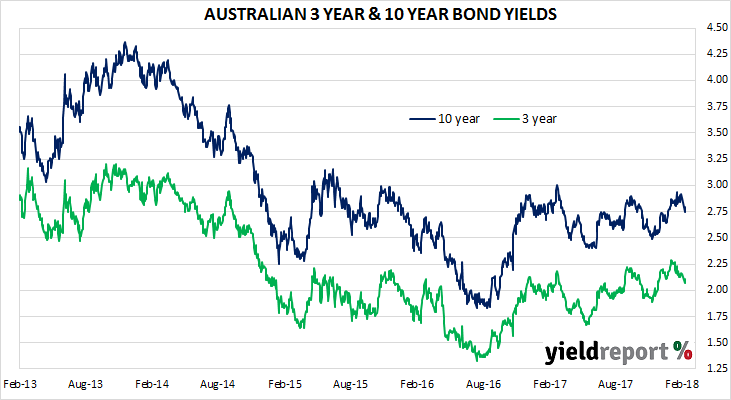

| Aust. 3 year bond%* | 2.11 | 2.07 | 0.04 |

| Aust. 10 year bond%* | 2.80 | 2.75 | 0.05 |

| Aust. 20 year bond%* | 3.22 | 3.18 | 0.04 |

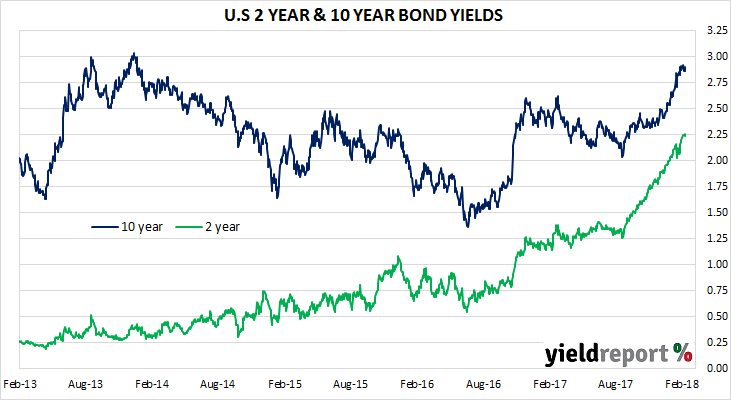

| U.S. 2 year bond% | 2.24 | 2.26 | -0.02 |

| U.S. 10 year bond% | 2.86 | 2.90 | -0.04 |

| U.S. 30 year bond% | 3.13 | 3.16 | -0.03 |

| * Implied yields from Mar 2018 futures | |||

LOCAL MARKETS

Bonds are likely to have a better day today following a selloff yesterday. Expect some squaring of positions leading to some choppiness in the market.

U.S. BOND MARKETS

Offshore investors have been hurt on the forwards and basis swaps as the Fed has hiked several times over 2017. The carry trade is less attractive despite the large differential between a U.S. 10-year and a ten-year bund for example. Last year for example many European investors could purchase a U.S. 10-year swap it back to euro and make a good turn. That arbitrage has now ceased. And for the U.S. treasury market this saps the interest a significant portion on important and large investors. For example, in 2015, European investors accounted for more than half of foreign purchases of U.S. treasuries, they are now net sellers.

Banks are now reluctant to lend dollars in the short term because of regulatory rules designed to make finance safer. Combine that with fewer traders and central bank purchases slowing the U.S. treasury market will be an interesting place to trade bonds. The target of 3% for a ten year looks likely to be breached soon and if we get a mix of bad policy, slowing tax receipts or some political upheavals the bond vigilantes may yet get their part to play. Should that happen even 4% is not that far away.