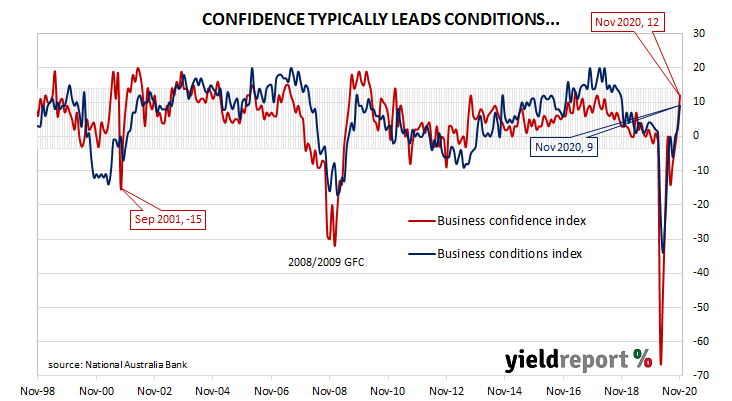

Summary: Business conditions, confidence improve; solid expansion is underway; Victorian conditions “to improve” as lockdown impact fades; capacity usage rate increases again; difference between employment and profitability sub-indices sends “mixed signals”.

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s indices then began to slip, declining to below-average levels by the end of 2018. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and the indices trended lower, hitting a nadir in April 2020 as pandemic restrictions were introduced. Conditions have improved markedly since then.

According to NAB’s latest monthly business survey of over 550 firms conducted in the latter part of November, business conditions improved for a third consecutive month. NAB’s conditions index registered 9, up from October’s revised reading of 2.

“The positive readings in most states suggest a solid expansion is underway, although we note the level of activity remains low, given all states saw large hits to activity earlier in the year,” said NAB chief economist Alan Oster.

Business confidence improved for a fourth consecutive month. NAB’s confidence index rose from October’s revised reading of +3 to +12. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

Oster noted two states had reported worse conditions but he expected Victorian “conditions to improve as the impact of its recent severe lockdown wears off.” Leading indicators such as capacity utilisation and forward orders had improved and the latter’s substantial rise suggested “the pipeline of work has begun to build.”