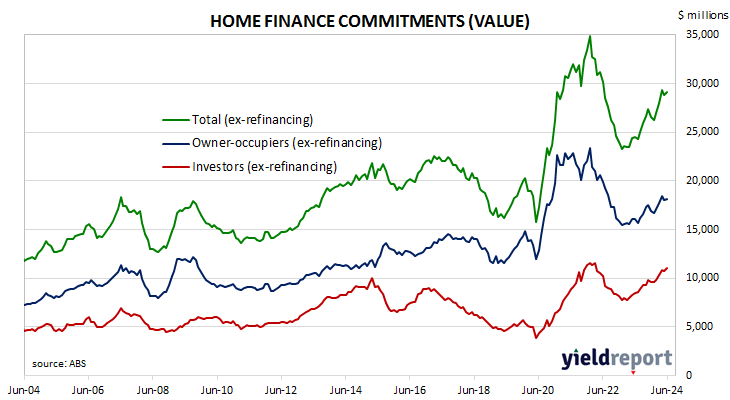

Summary: Value of loan commitments up 1.3% in June, above expectations; 19.1% higher than June 2023; Westpac: new lending increasingly led by investors; ACGB yields fall; rate-cut expectations firm; value of owner-occupier loan approvals up 0.5%; value of investor approvals up 2.7%; number of owner-occupier home loan approvals down 0.5%.

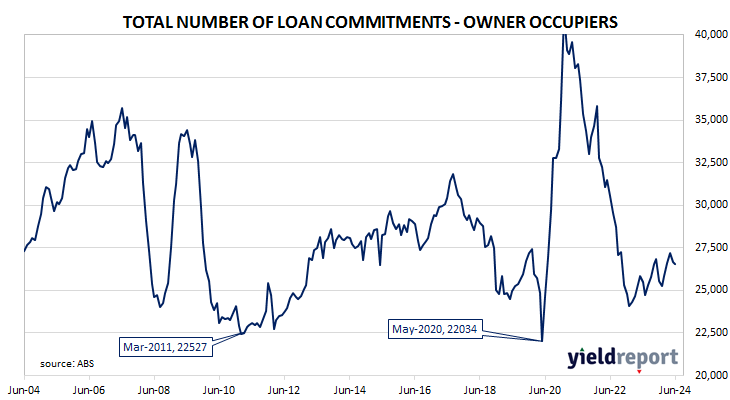

The number and value of home-loan approvals began to noticeably increase after the RBA reduced its cash rate target in a series of cuts beginning in mid-2019, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to record highs in 2021. After a considerable pullback in 2022 both the value and number of approved loans resumed rising in 2023.

June’s housing finance figures have now been released and total loan approvals excluding refinancing increased by 1.3% In dollar terms over the month, greater than the flat result which had been generally expected and in contrast with May’s 1.7% decline. On a year-on-year basis, total approvals excluding refinancing were 19.1% higher than in June 2023, up from May’s comparable figure of 18.0%.

“The detail continues to show similar themes to previous months; gains in new lending being increasingly led by investors and Western Australia the stand-out state in terms of strength,” said Westpac senior economist Matthew Hassan.

Commonwealth Government bond yields fell moderately on the day. By the close of business, the 3-year ACGB yield had shed 6bps to 3.64% while 10-year and 20-year yields both finished 3bps lower at 4.06% and 4.46% respectively.

Expectations regarding official rate cuts in the next twelve months firmed. In the cash futures market, contracts implied an average of 4.33% in August, 4.255% in November and 4.09% in February 2025. May 2025 contracts implied 3.865%, 47bps less than the current cash rate.

The total value of owner-occupier loan commitments excluding refinancing increased by 0.5%, a partial reversal of May’s 1.9% fall. On an annual basis, owner-occupier loan commitments were 13.2% higher than in June 2023, up from May’s comparable figure of 12.2%.

The total value of investor commitments excluding refinancing increased by 2.7%. The rise follows a 1.3% decline in May, taking the growth rate over the previous 12 months from 29.3% to 30.2%.

The total number of loan commitments to owner-occupiers excluding refinancing decreased by 0.5% to 26521 on a seasonally adjusted basis, a smaller decline than May’s 2.0% decrease. The annual growth rate accelerated from 3.1% after revisions to 4.0%.