08 January 2020

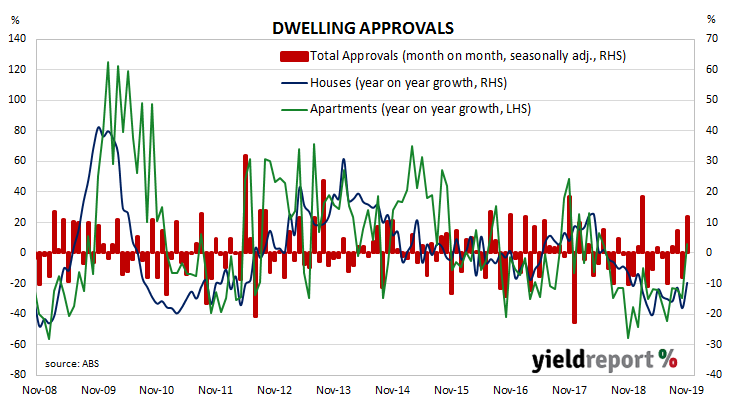

Approvals for dwellings, that is apartments and houses, have been heading south since mid-2018. As an indicator of investor confidence, falling approvals represent a worrying signal, not just for the building sector but for the overall economy. A recovery in 2020 is expected by some economists, while others are unwilling to be quite as definitive just yet.

The Australian Bureau of Statistics has released the latest figures from November and total residential approvals increased by 11.8% on a seasonally-adjusted basis, a larger rise than the 2% increase which had been expected and a marked turnaround from October’s revised figure of -7.9%. However, on an annual basis, total approvals were still down by 3.8%, although this figure is a large improvement on October’s comparable figure of -22.9% after revisions.

Westpac senior economist Matthew Hassan said, “Overall, the November update pares back some of the downside risks that were emerging from weak reads in previous months, although monthly volatility is making it difficult to be confident about trends.”

Domestic bond yields finished the day moderately lower. By the end of the day, the 3-year ACGB yield had lost 2bps to 0.76%, the 10-year yield had fallen by 4bps to 1.20% while the 20-year yield finished 3bps lower at 1.63%.

Prices of cash futures contracts moved to reflect a hardening of expectations of another cut in the cash rate target, some time in the next few months. By the end of the day, February contracts implied a 60% chance of a 25bps rate cut, up from the previous day’s 56%. March contracts implied an 80% chance of a cut, up from 73% while April contracts continued to imply another rate reduction was fully priced in.

07 January 2020

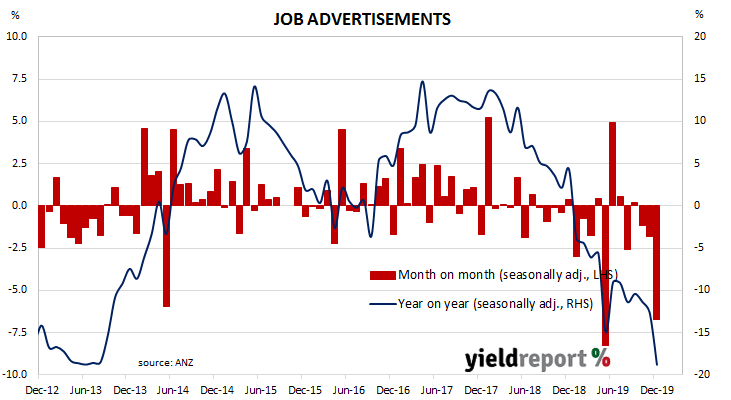

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising.

According to the latest ANZ figures, total advertisements fell by 6.7% in December on a seasonally-adjusted basis, following a 1.8% fall in November after revisions. On a 12-month basis, total job advertisements were 18.8% lower than the same month last year, a further deterioration from November’s comparable figure of -12.6% after revisions.

ANZ senior economist Catherine Birch said the latest figures provided an unwelcome surprise. “In the final two weeks of December, the number of job ads declined by more than we would expect for that time of the year, suggesting that the escalating bushfire crises had an impact.”

Domestic bond yields finished the day a little higher at the long end while shorter term yields were steady. By the end of the day, 3-year ACGB yields remained unchanged at 0.78%, the 10-year yield had increased by 2bps to 1.24% and 20-year yields had gained 3bps to 1.66%.

Domestic bond yields finished the day a little higher at the long end while shorter term yields were steady. By the end of the day, 3-year ACGB yields remained unchanged at 0.78%, the 10-year yield had increased by 2bps to 1.24% and 20-year yields had gained 3bps to 1.66%.

Prices of cash futures contracts moved to reflect slightly higher expectations of another cut in the cash rate target. By the end of the day, February contracts implied a 56% chance of another 25bps rate cut, up from the previous day’s 53%. March contracts implied a 73% chance of a cut, up from 71% while April contracts continued to fully price in another rate reduction.

03 January 2020

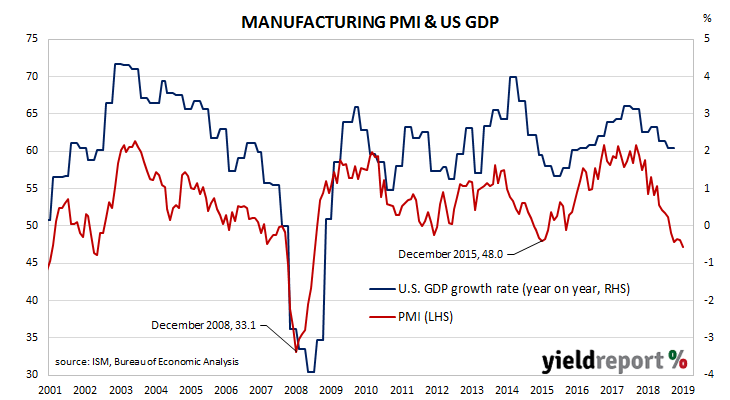

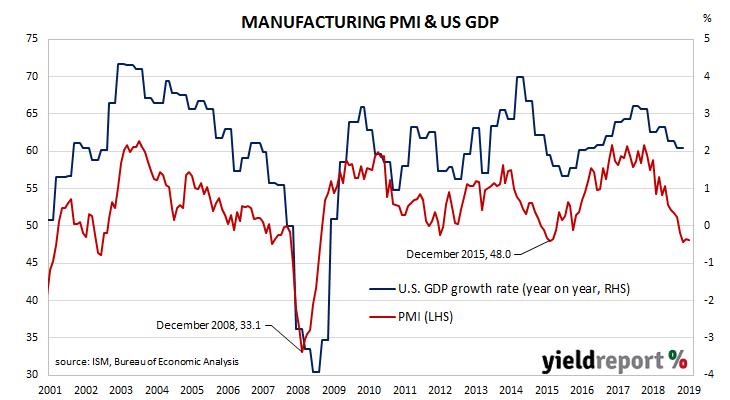

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Recent months’ readings appear to have stabilised, albeit at sub-neutral levels.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 47.2 for December, down from November’s reading of 48.1 and less than the market’s expected figure of 49. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

Despite the lower reading, the ISM’s Tim Fiore said “there are signs that several industry sectors will improve as a result of the phase-one trade agreement between the U.S. and China.”

Westpac’s economics team noted the ISM’s positive response to the figures. “Although the profile is one of contraction in production, the ISM write up suggested that sentiment was actually improving vs Q3 [the September quarter] and, despite global concerns, the report cited improvements due to the phase one trade deal with China.”

US Treasury yields fell noticeably across the curve but the falls were more a function of safe haven purchases prompted by news of the US assassination of a senior Iranian general. By the end of the day, the 2-year Treasury bond yield had lost 4bps to 1.53%, the 10-year yield had fallen by 9bps to 1.79% while the 30-year yield finished 8bps lower at 2.25%.

US Treasury yields fell noticeably across the curve but the falls were more a function of safe haven purchases prompted by news of the US assassination of a senior Iranian general. By the end of the day, the 2-year Treasury bond yield had lost 4bps to 1.53%, the 10-year yield had fallen by 9bps to 1.79% while the 30-year yield finished 8bps lower at 2.25%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut remained slim. The implied likelihood of a 25bps cut at the January meeting of the FOMC remained at zero while a move in March increased from 4% to 8%.

10 December 2019

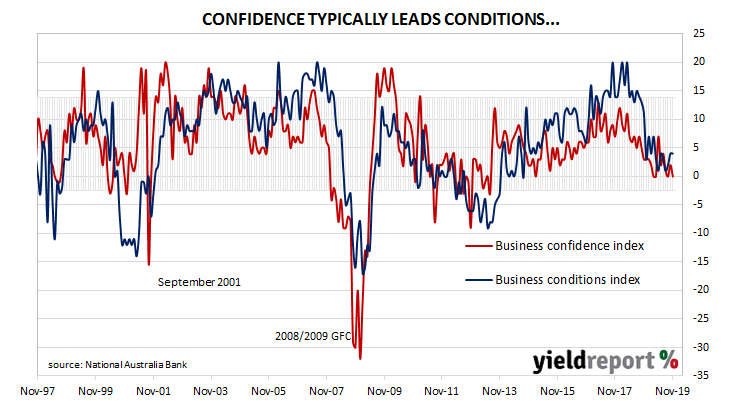

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April of that year. However, readings began to slip. By the end of 2018, they had dropped to below-average levels and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019. Since then, readings from NAB’s monthly surveys have varied very little.

According to NAB’s latest monthly business survey of 400 firms conducted in the latter part of November, business conditions continued to bump along at below-average levels. Since late 2018, NAB’s conditions index bounced between 3, which is on the low side of normal and 7, which is about average. The index then broke through this lower bound in May 2019. The latest reading registered 4, the same reading as in October after it was revised up from 3.

While the conditions index remained unchanged, the latest reading of NAB’s confidence index fell a couple of points, from October’s reading of 2 to 0 in November, well below its long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time.

NAB’s chief economist, Alan Oster, said business conditions look as if they “have stabilised at low levels”. Westpac senior economist Andrew Hanlan was less generous with his analysis. “The NAB survey suggests that weak conditions have extended into the December quarter and there is a lack of momentum heading into 2020.”

06 December 2019

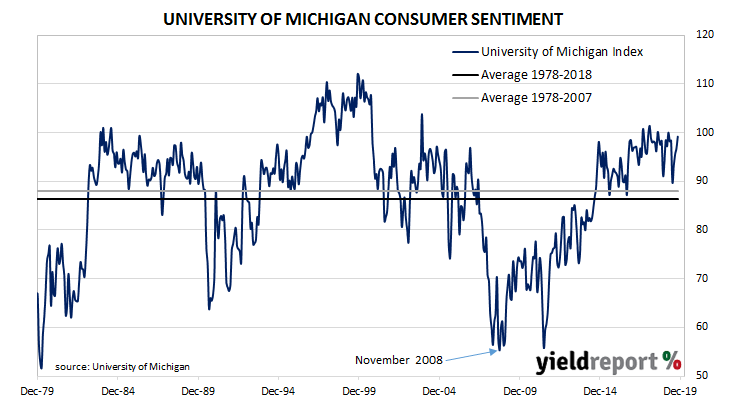

US consumer confidence started 2019 at average levels in a longer-term context, although readings were markedly lower than those which had been typical of most of the previous year. Since then, surveys have generally indicated US households maintained historically-high levels of confidence except for two short-lived plunges; one at the very start of the year and one in August.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households has increased for a fourth consecutive month. The University’s preliminary reading from its Index of Consumer Sentiment increased from November’s final figure of 96.8 to 99.2 in December, above the reading of 97.0 which had been expected.

The University’s Surveys of Consumers chief economist, Richard Curtin, noted the extended period in which the index had remained at elevated levels. “The Sentiment Index has averaged 97.0 in the past three years, the highest sustained level since the all-time record in the Clinton administration.”

US Treasury yields finished higher on the day, although a component of the increase should be attributed to the stronger-than-expected payrolls report released on the same day. By the close of business, 2-year Treasury yields were 5bps higher at 1.63%, the 10-year yield had gained 3bps to 1.84% and 30-year yields had increased by 2bps to 2.28%.

06 December 2019

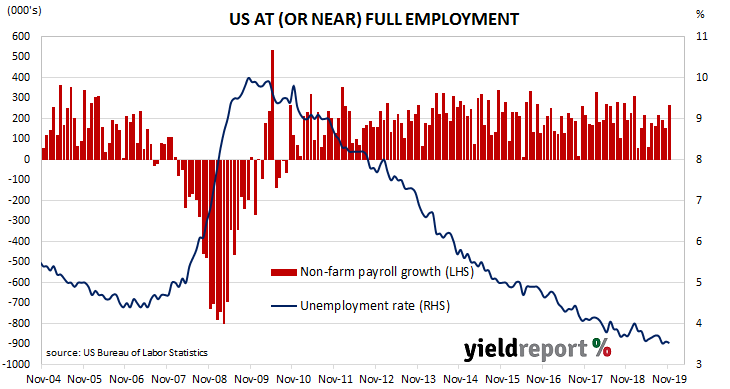

The US economy continues to produce more jobs despite being close to full employment. The unemployment rate has remained at or under 4% since April 2018 and the underemployment rate has been falling in trend terms. The latest employment report indicates the US economy is still producing jobs at a rate which is slowly grinding the US unemployment rate lower.

According to the US Bureau of Labor Statistics, the US economy created an additional 266,000 jobs in the non-farm sector in November, noticeably more than October’s revised increase of 156,000 and more than the 190,000 increase which had been expected. Employment figures for September and October were also revised up by a total of 41,000.

The November unemployment rate returned to September’s rate of 3.5% after climbing to 3.6% in October. The total number of unemployed decreased by 44,000 to 5.811 million while the total number of people who are either employed or looking for work increased by 399,000 to 164.764 million.

US Treasury yields finished higher on the day. By the close of business, 2-year Treasury yields were 5bps higher at 1.63%, the 10-year yield had gained 3bps to 1.84% and 30-year yields had increased by 2bps to 2.28%.

05 December 2019

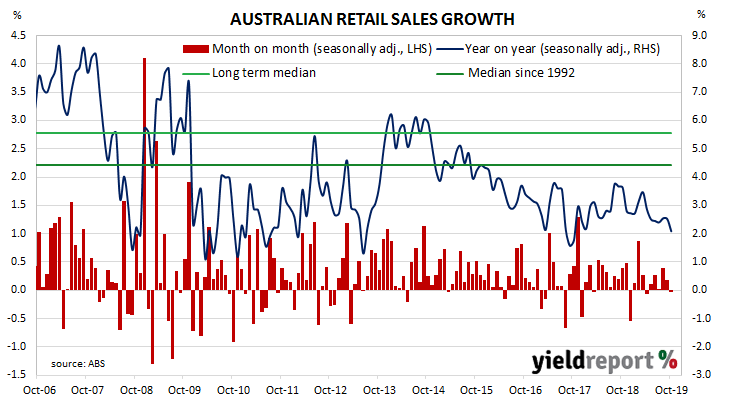

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered a growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018 before beginning another period during 2019 in which annual growth rates fell.

According to the latest ABS figures, total retail sales were flat in October on a seasonally-adjusted basis, under the expected increase of +0.3% and less than September’s 0.2% increase. On an annual basis, retail sales increased by 2.1%, a slower rate than September’s comparable figure of 2.5%.

Westpac senior economist Matthew Hassan said, “The spending ‘strike’ of Q3 looks to have extended into early Q4 with still no evidence of a boost from tax refunds or interest-rate cuts…” ANZ economist Adelaide Timbrell put the lack of consumer enthusiasm to spend down to a combination of “household debt levels, rising cost of living, consumer pessimism and increasing labour market risks”, noting annual sales growth had fallen to a two-year low. US Treasury yields had increased during the previous night, lending support for higher yields in the domestic market despite the lacklustre sales figures. By the end of the day, 3-year ACGB yields had crept 1bp higher to 0.69%, the 10-year yield had gained 3bps to 1.09% while the 20-year yield finished 5bps higher at 1.52%.

US Treasury yields had increased during the previous night, lending support for higher yields in the domestic market despite the lacklustre sales figures. By the end of the day, 3-year ACGB yields had crept 1bp higher to 0.69%, the 10-year yield had gained 3bps to 1.09% while the 20-year yield finished 5bps higher at 1.52%.

04 December 2019

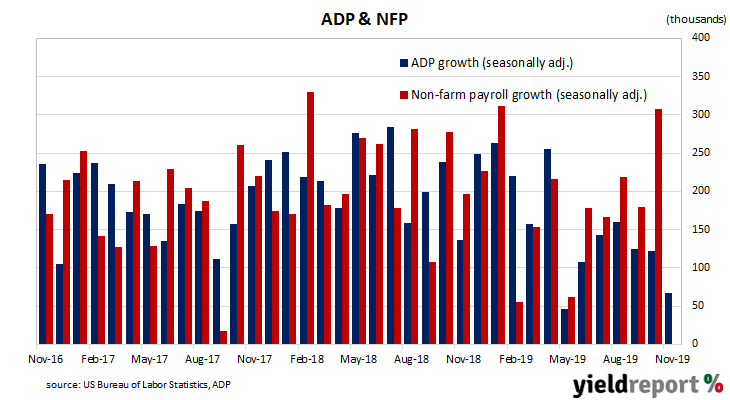

The ADP National Employment Report is published monthly by the ADP Research Institute. The report provides an estimate of US non-farm employment in the private sector. Since the report began to be published in 2006, its total private sector non-farm employment figures have exhibited a high correlation with the Bureau of Labor Statistics (BLS) non-farm payroll figures which are typically published a day or two later.

The latest figures indicate private sector employment grew by 66,900 in November, below the expected figure of 140,000 and less than October’s revised increase of 121,400.

ANZ economist Hayden Dimes noted the increase was the smallest in the last six months and only half the expected figure. “All the new jobs were in the service sector; however, this sector is also slowing.”

US Treasury yields increased along the curve. By the end of the day, 2-year Treasury bond yields had gained 3bps to 1.57%, the 10-year yield had increased by 5bps to 1.77% while the 30-year yield finished 7bps higher at 2.23%.

02 December 2019

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. However, readings appear to have stabilised lately, albeit at sub-neutral levels.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 48.1 for November, slightly less than October’s reading of 48.3 and less than the market’s expected figure of 49.5. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “Global trade remains the most significant cross-industry issue. Among the six big industry sectors, Food, Beverage & Tobacco Products remains the strongest, while Fabricated Metal Products is the weakest.” NAB economist Tapas Strickland said a fall in the New Orders sub-index is “suggestive that activity could weaken further in the months ahead.” ANZ senior economist Cherelle Murphy said the figures “suggest US manufacturing activity is still struggling.”

US Treasury yields increased along the curve, especially at the long end. By the end of the day, 2-year Treasury bond yields had inched up 1bp to 1.61%, the 10-year yield had increased by 4bps to 1.82% and the 30-year yield finished 7bps higher at 2.27%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of another rate cut in 2019 remained at zero. The likelihood of a 25bps cut at the January meeting of the FOMC declined a little, moving from 10% to 8%. A move in March is also viewed as unlikely, although the implied probability had increased from 18% to 20% by the end of the day.

02 December 2019

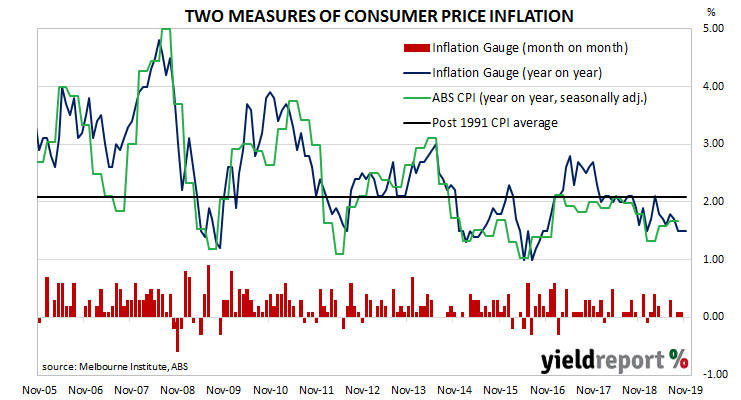

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed. The latest unofficial reading suggests consumer inflation is not likely to increase any time soon.

The Melbourne Institute’s latest Inflation Gauge index remained unchanged in November following 0.1% increases in both October and September. On an annual basis, the index increased by 1.5%, the same rate as in October.

Domestic bond yields finished the day noticeably higher, although it is unlikely the sell-off was driven by these figures or the other reports such as October’s dwelling approvals figures and ANZ’s latest Job Ads survey which were released at roughly the same time. By the end of the day, 3-year ACGB yields had gained 4bps to 0.69% while 10-year and 20-year yields had each increased by 6bps to 1.10% and 1.50% respectively.

Prices of cash futures contracts moved to lower expectations of another cut in the cash rate target, although one more rate cut is still largely expected within the next six months. By the end of the day, December contracts implied a 9% chance of another 25bps rate cut, down from the previous day’s 13%. February contracts implied a 70% chance of a cut, down from 77% while May continued to fully price in another rate reduction.