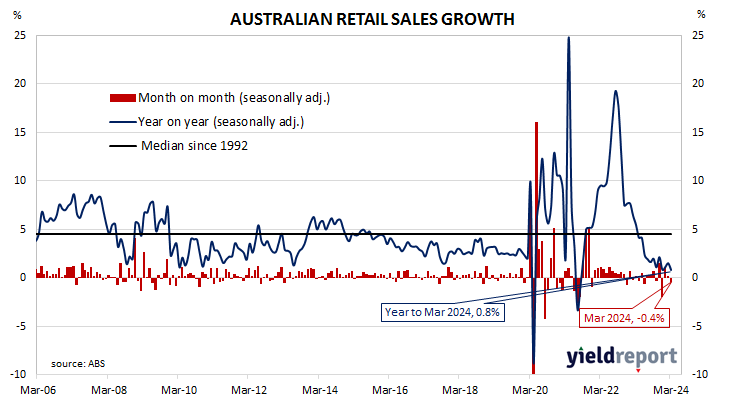

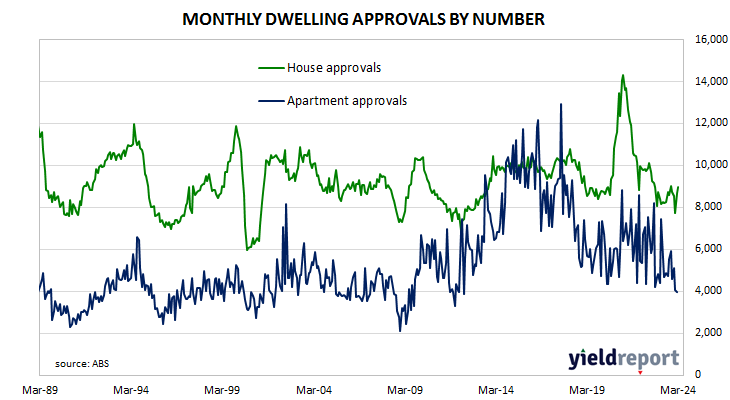

Home approval numbers up 1.9% in March, less than expected; 2.2% lower than March 2023; Westpac: uncertain as to continuation of weakness from December-February period; ACGB yields down; cash rate expectations sending mixed messages; Westpac: more-volatile private units segment may be playing larger role; house approvals up 3.6%, apartments down 1.8%; non-residential approvals up 28.7% in dollar terms, residential alterations up 8.3%.

Building approvals for dwellings, that is apartments and houses, headed south after mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and the early months of 2020 painted a picture of a recovery taking place, even as late as April of that year. Subsequent months’ figures then trended sharply upwards before reversing course and falling back through 2021, 2022 and 2023.

The Australian Bureau of Statistics has released the latest figures from March and they show total residential approvals rose by 1.9% over the month on a seasonally-adjusted basis. The rise was less than the 3.0% gain which had been generally expected but it contrasted with February’s 0.9% decline after revisions. Total approvals fell by 2.2% on an annual basis, up from the previous month’s revised figure of -5.3%. Monthly growth rates are often volatile.

“Overall, it remains uncertain whether the signs of weakness over December-February is signalling a renewed underlying downtrend in dwelling approvals,” said Westpac economist Ryan Wells.

Commonwealth Government bond yields fell nearly uniformly across the curve on the day, somewhat in line with the falls of US Treasury yields on Wednesday night. By the close of business, the 3-year ACGB yield had lost 5bps to 4.06%, the 10-year had shed 6bps to 4.46% while the 20-year yield finished 5bps lower at 4.74%.

In the cash futures market, expectations regarding the cash rate changes over the next 12 months continued to send mixed messages. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.325% through May and 4.345% in June. However, November contracts implied a 4.42% average cash rate, February contracts implied 4.33%, while May 2025 contracts implied 4.23%.

“At face value, March’s lift in headline approvals was not as strong as expected, but its compositional detail suggests that the more-volatile private units segment may be playing a larger role,” Wells added. “More data is needed to form a judgement on the underlying trend.”

Approvals for new houses rose by 3.6% over the month, down from February’s 12.2% after revisions. On a 12-month basis, house approvals were 7.0% higher than they were in March 2023, up from February’s comparable figure of -0.9%.

Apartment approval figures are usually a lot more volatile and March approvals for this category declined by 1.8% after a 20.7% fall in February. The 12-month growth rate fell from February’s revised rate of -13.4% to -18.1%.

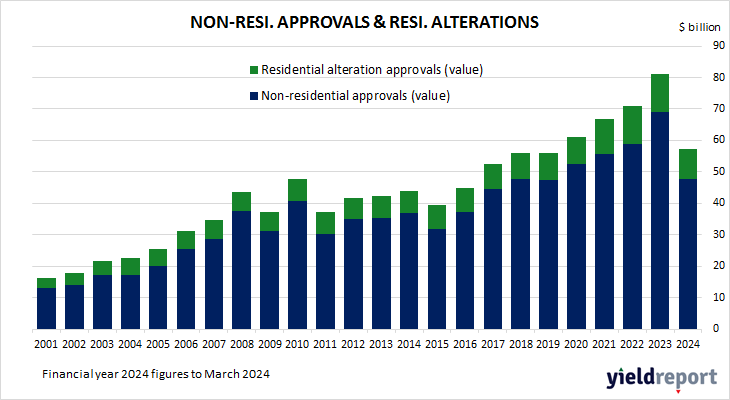

Non-residential approvals increased by 28.7% in dollar terms over the month but were 5.7% lower on an annual basis. Figures in this segment also tend to be rather volatile.

Residential alteration approvals rose by 8.3% in dollar terms over the month and were 9.2% higher than in March 2023.