27 April 2017

NextDC Ltd has announced it will be issuing another series of senior unsecured notes shortly. The company builds and operates data centres in Australia and New Zealand and it is seeking to raise a minimum $200 million.

The funds raised will be used to replace two series of notes issued in June 2014 and December 2015 which have a combined face value of $160 million. The balance will be used for general purposes. However, under the terms of the notes already on issue, optional redemption by NEXTDC before the June 2019 maturity date activates a bonus clause in each series. In both series 1 and series 2 notes, redemption in June 2017 is the second optional redemption date. For series 1 notes, the payment amount on this date is 103.50% of the principal while for series 2 notes it is 102.00%. Thus around $4 million will be used up in this way on top of any other costs of the issue.

In a move which is common for debt and hybrid securities listed on the ASX, NEXTDC will possibly offer existing noteholders the option to exchange holdings in existing series 1 and 2 notes for holdings in the new series. This brings up the question as to whether holders who take this option will still be eligible for the bonus optional redemption payments.

Series 1 and 2 notes have a June 2019 maturity date, but series 1 notes have a 8% coupon while series 2 notes have a 7% coupon. No further details on the new notes are available at this point but it is reasonable to speculate a similar structure to the first two series is likely. Swap rates have come down since then so perhaps the coupon on this next series will be lower again.

26 April 2017

Unlike the weeks prior to recent CPI reports, the level of attention given to this latest CPI report has been relatively scant. The latest RBA board meeting minutes indicate Australia’s central bank is focussed on the employment market and risks in the housing markets (Sydney and Melbourne). Mentions of underlying inflation were mostly limited to stating how any rise was expected to be gradual. While some commentators noted the importance of the upcoming CPI report, other issues, such as Trump’s tax plans, tended to divert attention away from it.

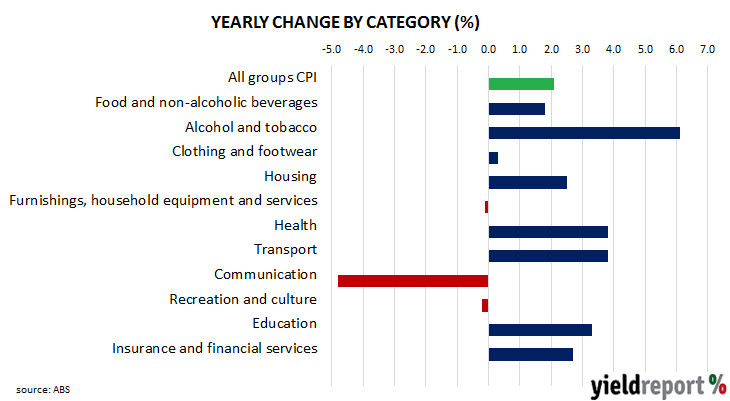

The figures have now been released by the ABS and they were weaker than the market expected, for all three inflation measures (headline, seasonally-adjusted and core). Both headline and seasonally-adjusted inflation came in at 0.5% and 2.1% for the year, each 0.1% under market expectations.

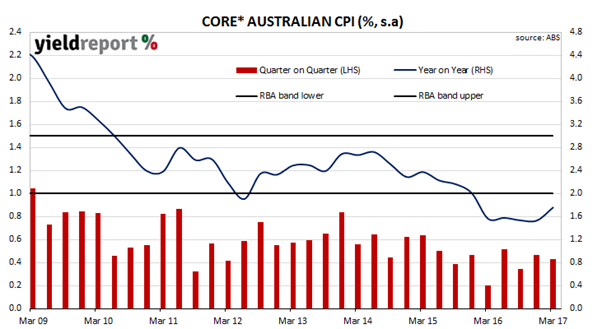

“Core” inflation measures favoured by the RBA, such as the “trimmed mean” and the “weighted median”, were slightly below consensus when considered together. For the quarter, both the trimmed-mean and weighted-median measures increased by 0.4% and the average of the two annual rates came in at 1.8%. Market expectations were for 0.5% for the quarter and 1.9% for the year.

Bond yields went higher on the day. 3 year yields were up 3bps at 1.88% and 10 year bond yields finished the day 4bps higher at 2.66%. The AUD dropped immediately from 75.45 US cents to 75.20 US cents and then fell further during the evening. A weaker currency with higher bond yields seems to be at odds until one realises the Australian bond market was also reacting to two days of higher yields in offshore markets after the ANZAC Day holiday.

25 April 2017

Consumer confidence surveys are important private sector surveys even though economists view them as lagging indicators. Their importance lies in the confirmation of spending patterns and as consumption in developed countries may amount to 60%-70% of GDP, knowing how it is behaving is important for financial markets’ forecasts for GDP growth rates, which in turn flow into demand for credit and inflation rates.

The Conference Board Consumer Confidence Index is one of two U.S. consumer sentiment indices, the other being the University of Michigan’s Consumer Sentiment Index. The Conference Board’s index is based on perceptions of current business and employment conditions, as well as expectations of business conditions, employment and income six months into the future.

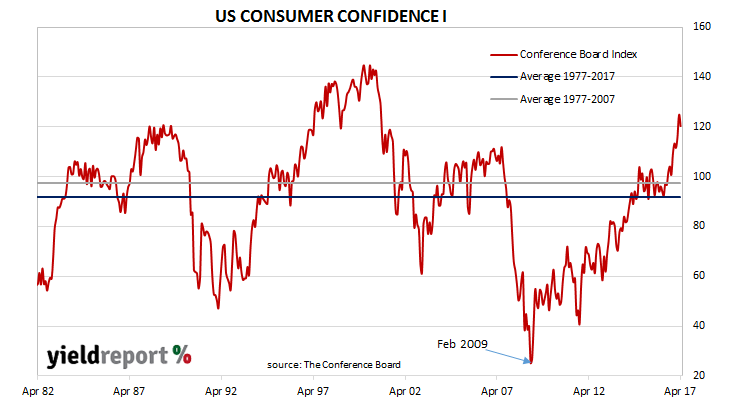

The latest release from the Conference Board’s April survey suggests U.S. consumers are optimistic about the near-term, although not as much as they were in March. The April reading came in at 120.3, down from March’s revised reading of 124.9 but well up on the 2016’s comparable figure of 94.2.

Since the GFC survey results have not been consistently over 100 and the months in which the index has been above 100 have been sporadic. However, since August 2016, all readings have been above 100 and recent months have returned almost boom-time conditions. As ANZ described it, “…the fall only partly reversed the surge in March, with the headline index still close to a 16-year high. The details point to a strong labour market with respondents saying that jobs are plentiful rather than hard to find, remaining close to a 16-year high…”

24 April 2017

- YieldReport has commenced on-line coverage of the peer-to-peer investment sector.

- Makes finding higher yielding investments in a low interest rate environment easier.

- Plans to expand the coverage of investment opportunities.

Today we officially launch our coverage of the peer-to-peer lending sector on our website. As a relatively new but fast growing investment sector, peer to peer lending has seen a number of new entrants. While there are many investment opportunities available in this space, the ability to find those opportunities has up until now been difficult.

We have witnessed the rapid growth in demand at both the retail and institutional level for credit based investment opportunities, led by the banks issuing large levels of debt to help sure up their balance sheets.

This increased demand in credit based investing has seen the peer to peer lending market (which sits as a sub-set of credit markets) continue to grow and attract investor attention. What is also helping to drive interest and growth in this investment sector is the historically low interest rate environment, and the search for yield. Some commentators report that the value of loans made through peer-to-peer lending platforms in Australia is expected to surge to $22 billion by 2020.

Investors of all types, including self-managed super funds and institutional investors are finding it difficult to meet their investment objectives in the current low interest rate environment. While one year term deposit rates can currently provide a return of around 2.5%, peer to peer investment opportunities provide an attractive alternative, where returns can be 7% plus.

Market information about equities is generally freely available and covered by almost all and sundry. However, there is still a distinct lack of access to quality information in the mainstream about yield focused investment opportunities such as peer-to-peer lending that provides an income stream. YieldReport seeks to address that gap by providing relevant information about the income and yield related investment opportunities.

19 April 2017

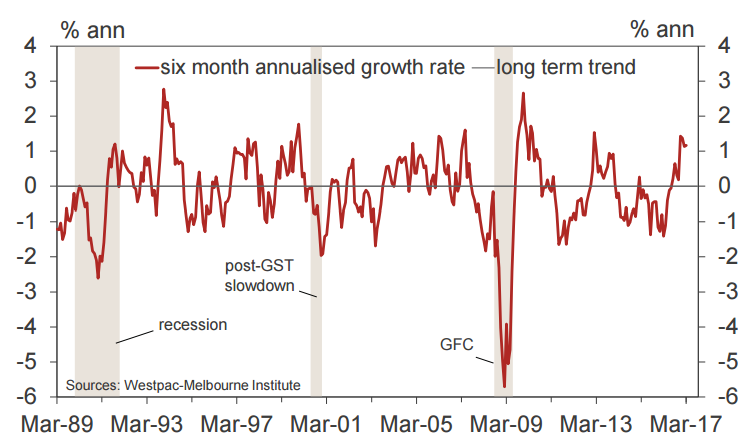

2017 is shaping up as a year in which Australian GDP growth is likely to be around 3.0% if the Westpac-Melbourne Institute’s Leading Index maintains its record of being a reliable indicator. According to Westpac, the Leading Index indicates the likely pace of economic activity relative to trend three to nine months into the future.

This latest April reading rose to 1.17% from its March reading of 1.14%, which for all intents and purposes is a stable reading but it is also the eight month in a row where the index has been at or above trend (indicated by a zero reading). Trend growth was once taken to mean around 3% but recently the RBA and private sector economists have been suggesting it may mean 2.75%. As the index relates to growth rates above trend, GDP for the can be expected to be in excess of 2.75% unless the index deteriorates as the year goes on.

3.0% is in the mid-point of the RBA’s forecast range of 2.5%-3.5% growth for 2017 which it stated in its February Statement on Monetary Policy (SoMP). Westpac’s Bill Evans, thinks GDP growth is likely to be 3% through 2017. “…the ongoing positive signal from the Index gives us some comfort that we can expect solid growth in the first half of 2017….Westpac concurs with the Bank’s current forecast of 3% growth through 2017.”

18 April 2017

The April meeting of the RBA held on the first Tuesday of the month left the overnight cash rate steady at 1.50%, as expected. Historically, RBA meetings in April have been uneventful as rate changes are typically made in February, May, August and November after quarterly CPI figures have been released. However, the minutes from such meetings provide clues with regards to the RBA’s state of mind and where their focus is likely to be in coming months.

The minutes covered all the usual territory; the global economy, the domestic labour market, international financial markets and stability of the domestic financial system. “Conditions in the global economy had continued to improve over 2017” and international financial markets “generally had been relatively stable over the preceding month.” Cyclone Debbie received a mention but the RBA did not consider it to have a major effect. However, the minutes from the meeting indicated the RBA board is focussed on two major issues.

One of these is the state of the labour market and its effect on consumer confidence and spending. The other is the risk to the banking system which emanates from high levels of household debt, which is tied to the state of house prices, especially in Sydney and Melbourne. The labour market “had been somewhat weaker than had been expected” while the domestic financial system was facing “[r]isks related to household debt and the housing market more generally…” Perhaps in an ominous tone, the minutes pointed out these risks “had increased over the preceding six months.”

Bill Evans, Westpac’s chief economist, singled out the final sentence in the “Considerations for Monetary Policy” section as a sign of the RBA’s concern. “The Board judged that developments in the labour and housing markets warranted careful monitoring over coming months.” Adam Boyton, Deutsche Bank’s chief economist, agreed. “We think the key point there is the final sentence – namely it will take time to see how these measures play out.”

14 April 2017

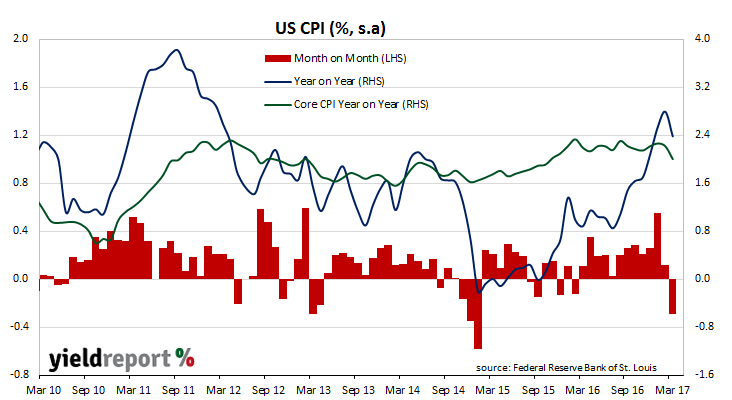

Consumer inflation went backwards for the first time in a year in the US. Although the consumer price index (CPI) is not the US Fed’s preferred measure of inflation, rises and falls in the rate of CPI inflation add to the overall picture of the US economy’s price level. March CPI figures released by the Bureau of Labor Statistics indicate consumer prices fell by 0.3% for the month, another fall from the previous month’s comparable figure of 0.1% and lower than the consensus market forecast of 0.0%.

On a year-on-year basis, the CPI increased by 2.4%, which is down from February’s comparable figure of 2.8%. Core prices, the measure of prices which strips out food and energy price changes, fell 0.1% for the month and in line with expectations. Over the last 12 months, core inflation has slipped down to 2.0% from February’s 2.2% (seasonally adjusted).

(The figures came out on Easter Friday which is not a trading day for U.S. bond markets.)

13 April 2017

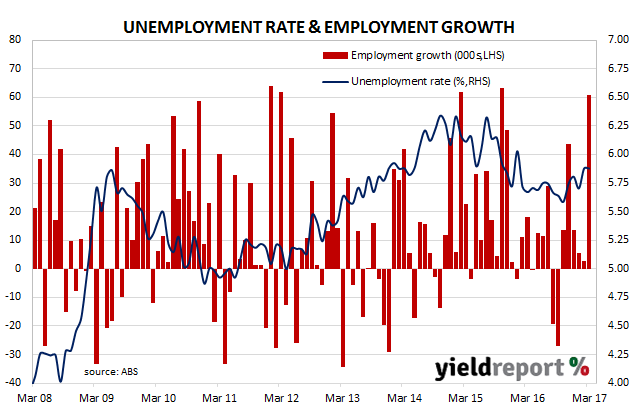

Australia was effectively quarantined from the GFC and its aftermath. Many other countries’ economies went through the wringer and unemployment in these countries skyrocketed to 10% and above. In Australia, peak unemployment was reached in 2014 at the relatively low rate of 6.3%. While Australian unemployment may have escaped the worst of the GFC, the unemployment rate is now higher than rates in the UK, the US, Germany and New Zealand.

Australia’s unemployment rate remained steady in March as employment growth was offset by a higher participation rate. The Australian Bureau of Statistics has released employment estimates which indicated Australia’s unemployment rate remained at 5.9%. The total number of people employed in Australia in either full-time or part-time work rose by a massive +60,900 during the month, in contrast with the market’s expectation of +20,000. The participation rate increased from 64.6% to 64.8% and the total hours worked rose by 0.2% over the month or 0.8% more than the comparable number from March 2016.

Yields had increased overnight in offshore markets so it appears the employment figures were responsible for at least some downward pressure on yields. 3 year bond yields fell 1bp to finish the day at 1.78% while 10 year yields fell 3bps to finish at 2.50%. The Aussie lifted quickly to 75.70 US cents after the announcement and it was at 75.90 US cents at the close of business.

The reaction from economists and other commentators was generally positive, although doubts over the reliability of the data have surfaced again. The massive increase in total employment raised the odd eyebrow and the admission by the ABS of some errors regarding the number of under-employed did not help. Doubts regarding ABS figures have been around for some time now. In an era of fake news, these sorts of errors by government departments just add fuel to claims the public should not believe anything.

12 April 2017

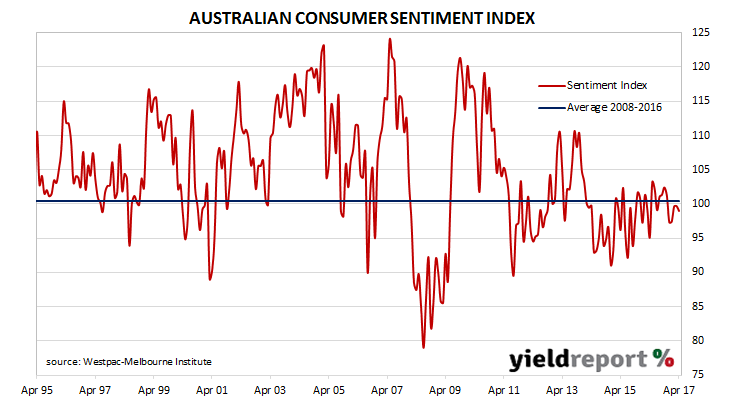

Australian households are copping it from all sides. Wages and salaries are rising at historically low rates while householders are being warned about the dangers in the property market and how many (other) borrowers may suffer were mortgage rates to increase. So, it is not really a mystery when a survey of consumer sentiment does not indicate rampant optimism.

The Westpac-Melbourne Institute consumer sentiment index limped a little lower in April, and recorded a decrease from 99.7 to 99.0. Any reading below 100 indicates the number of consumers who are pessimistic is more than the number of consumers who are optimistic. Bill Evans, Westpac’s chief economist said he thought it was going to be worse. “This is a surprising but welcome result.”

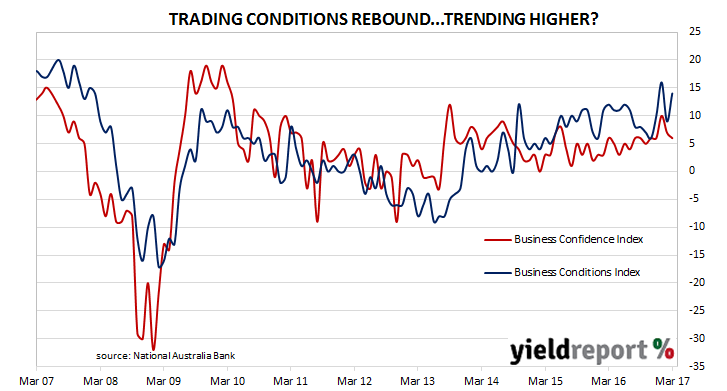

11 April 2017

Apparently Australian businesses are enjoying buoyant conditions across almost all industries and confidence levels are above average. According to NAB’s latest monthly business survey of 400 firms in March, its Business Conditions Index rose 5 points to 14 while its Business Confidence Index eased back 1 point to 6, which is the average over the life of the series.

Trading conditions were good, profitability solid, employment conditions improved and spare capacity was reduced. However, there was one sector of Australian business which was the exception to all this good news. ANZ’s Felicity Emmett said the retail sector has been doing it tough and it is likely to continue. “The retail sector, however, continues to struggle, with competition and weak sales continuing to put downward pressure on prices.” February retail sales figures out last week indicated how the pace of growth in retail sales has fallen since a post-GFC peak was reached in 2013/2014 and the NAB survey is another piece of evidence which provide confirmation.