20 September 2016

Upcoming meetings of the Bank of Japan and the FOMC are sucking the oxygen away from other topics in financial markets so the release of the RBA September meeting minutes have been somewhat pushed aside. Even so, the board’s views on unemployment, inflation and house prices were deemed to be main points of interest but other than those, the minutes were not expected to provide any surprises.

House prices, especially those in Sydney and Melbourne, have been a topic of discussion since the second rate cut of the year occurred in August. There have been reports of large prices increases and high auction rates and observers were keen to see how the RBA viewed these developments. The minutes indicate the RBA is ambivalent about prices, noting a decline in auctions and a rising trend in the average number of days a property was on the market. It also expects a “considerable volume of apartments scheduled to be completed over the next couple of years, particularly in the eastern states” to add to supply.

Here’s what the economists said:

Bill Evans, Westpac:

“We have been somewhat surprised at the more downbeat tone used around the housing market. Nevertheless this sentiment is not consistent with any imminent decision to adjust rates….While no one gives any chance to a policy move on October 4 there is still plenty of anticipation that the Bank will cut rates at its following Board meeting on November 1. We do not think that there is any evidence in the themes set out in these minutes or the recent Statement on the Conduct of Monetary Policy that would lead to a move in November. We remain comfortable with our view that the overnight cash rate will remain steady for the next few years. “

Tom Kennedy, JPMorgan

“Following today’s minutes we retain our view for the RBA to be on hold for the remainder of 2016, notwithstanding any unexpected deterioration in cyclical activity data….From here, the key uncertainty for the RBA is likely to be the persistence of low inflation. Our bias remains to think that the RBA will deliver a further 50bps of easing in 1H17, taking the cash rate to 1%.”

Su-Lin Ong, RBC

Despite some pickup in house prices more recently, the minutes continued to suggest a degree of comfort at the broad aggregate level. They highlight a general moderation in house price growth over the last year, a decline in turnover and lower housing lending growth as macro prudential measures exert some influence. At this juncture, we think that the case to cut again before the end of the year is not particularly compelling.

Paul Brennan, Citi

The RBA may have overestimated household consumption growth. The view was that “growth in household consumption was expected to have remained around average in the June quarter”. But the Q2 GDP data showed that household consumption growth had halved. The minutes also said that liaison contacts reported that employers had been more cautious in their hiring decisions, a remark that suggests the shock August employment data may not have been a one off event. Hence, we still hold the view that the RBA will need to cut again before the cycle in complete, with November being the next live meeting.

19 September 2016

ASX data released recently shows that investors have welcomed the ability to invest in fixed income via Exchange Traded Funds. Total funds invested have increased 41% to $2.3 billion as at the end of August 2016. The numbers are still dwarfed by equity ETFs but it is growing as investors and advisors gain more knowledge and comfort with the fixed income asset class.

In particular, YieldReport has noticed significant switching occurring over the past 12 months as investors amend their asset allocations from, say, corporate bonds to government bonds and back again. The ease of trading ETFs allows such asset allocations to occur smoothly and with limited cost. When corporate creditworthiness comes under pressure switching out of corporate bonds to government bonds becomes more pronounced.

Importantly the ease of trading an ETF for many is a lot easier than conducting a physical bond transaction.

Year to date the Bloomberg AusBond composite bond index has outperformed the S&P/ASX 200 and perhaps retail investors have cottoned onto this.

16 September 2016

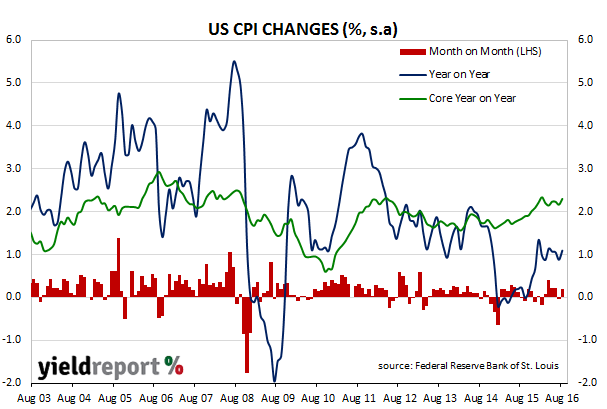

The US Fed may finally be getting what it wanted from the latest inflation figures. CPI figures released by the US Labor Department for August indicate consumer prices rose 0.2% for the month, 1.1% for the year and more than the 0.1% expected by financial markets. Core prices, the measure of prices which strips out food and energy prices changes, rose a higher-than-expected 0.3% for the month. Over the last 12 months the rise was 2.3% (seasonally adjusted) and back to pre-GFC levels (see chart below).

It is a little early to state definitely that inflation is rising; the headline CPI figure is still closer to 1% than 2% and other economic indicators such as retail sales and industrial production figures have been weak. However, both headline and core inflation figures beat expectations and US bond yields rose once the report was released. The USD was higher against a basket of currencies, which indicates exchange markets think higher interest rates in the US are more likely. On the other hand, cash market futures imply the probability of a rate increase at September’s meeting of the US Fed is still only 18%.

According to the Bureau of Labor Statistics rises in the overall price level was driven by housing and medical care costs. Medical care services rose 5.1% in the last twelve months while medicines and other medical care consumables rose 4.5% for the same period. Falling oil prices have been responsible for low consumer inflation figures in the last few years but in august energy costs were stable, although they were down 9.2% compared to August last year.

On the day US yields had drifted lower until the report’s release sparked a reversal. The US 2 year yield rose 3bps to 0.76% and 10 year yield finished 1bp higher at 1.69%.

14 September 2016

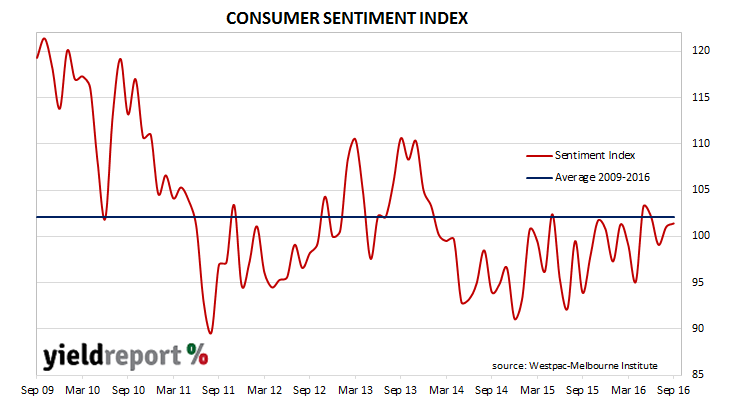

Consumer confidence has increased only marginally but it is still around the long-term average according to the latest consumer survey. The September Westpac Melbourne Institute consumer sentiment survey shows a rise from August’s reading of 100.0 to 101.4. Any reading above 100 indicates the number of consumers who are optimistic is more than the number of consumers who are pessimistic.

The RBA’s August rate cut and the mortgage rate reductions which followed are now water under the bridge, although Australians generally think the unemployment rate will fall and family finances are better than a year ago. However, these are at odds with an increase in the number of people who think family finances and economic conditions in general will deteriorate over the next twelve months.

Westpac’s chief economist Bill Evans described the readings as “remarkably stable…despite significant events that can usually be expected to impact confidence”. He does not expect any more rate cuts this year unless October’s inflation report contains unexpectedly low numbers.

The 3 year bond yield rose 1bp to 1.62% and the 10 year bond rate was up 3bps to 2.12%. The AUD rose marginally against the USD but fell against the euro and the yen.

13 September 2016

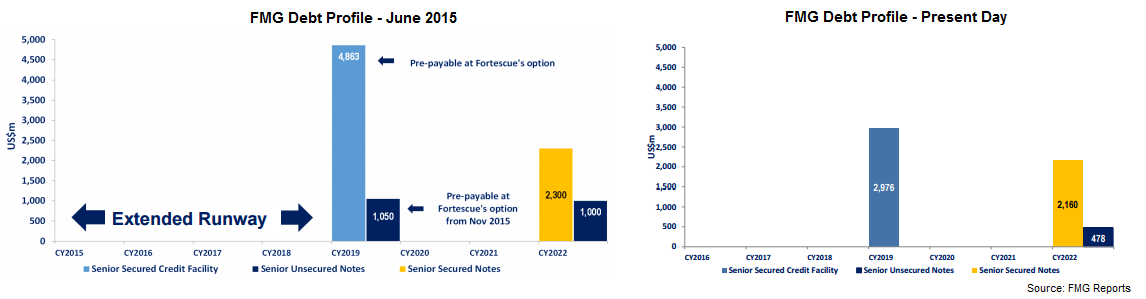

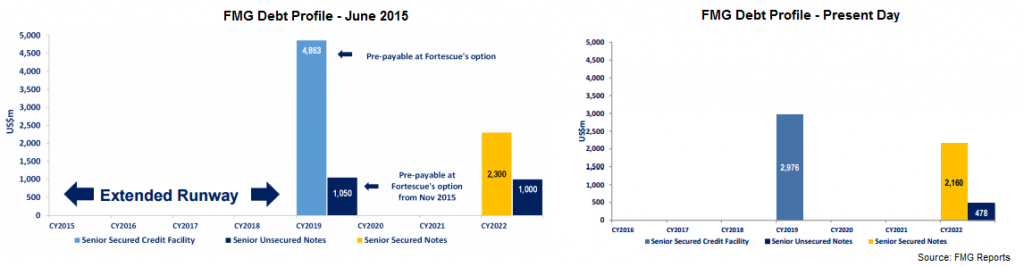

Fortescue is another step closer to winning an investment-grade credit rating after it announced another debt repayment. It has issued a notice of repayment on its USD$700 million 2019 senior secured credit facility with the repayment to be financed out of free cash flow. This latest repayment comes on top of USD$2.9 billion already repaid in the 2016 financial year.

Westpac estimate Fortescue’s credit ratios as exceeding the thresholds specified by S&P Global Ratings for a credit upgrade. However, the bank points out S&P’s guidance regarding future conditions where iron ore prices are lower and “we don’t see an upgrade from S&P occurring imminently. UBS are less positive and state the market still views Fortescue’s debt levels as a concern although it acknowledges any debt repayments are positive. Macquarie are the most bullish and expect the iron ore miner to be upgraded to investment grade in the near term if especially iron ore price holds up.

13 September 2016

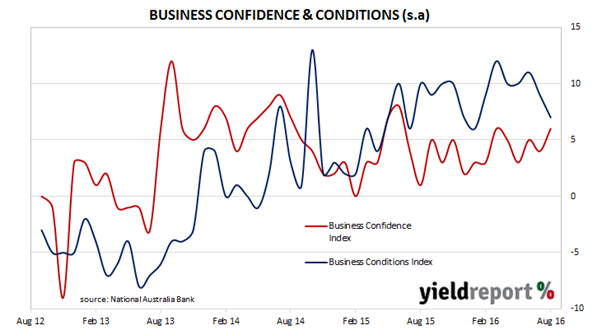

Australian businesses sentiment was generally buoyant in August, underpinned by business conditions which are still above the long-term average despite some headwinds in the retailing sector. In NAB’s latest monthly business survey, the Business Conditions Index moved 2 points lower from a revised July figure of 9 (previously 8) to 7 while the Business Confidence Index rose 2 points to 6. St. George Bank senior economist, Jo Horton, said the survey “results were relatively upbeat following some disappointing numbers released by the Australian Industry Group earlier in the month.”

Last month NAB’s chief economist Alan Oster changed his view on official interest rates over the next 12-18 months on the basis GDP growth is likely to slow, following a deterioration in conditions in the transport and wholesale sectors. August figures suggest the non-mining segment of the economy is improving but some parts are “a cause for concern”. “The strength in business conditions remains largely confined to the major services and construction industries, while relatively subdued conditions in wholesale and retail warrant close monitoring…It points to a patchy, but sustained, improvement in the non-mining economy.”

The latest figures have not altered the NAB economist’s views of what is in store for Australia and the two 25bps cuts he expects the RBA to hand out in 2017. “Beyond the near-term, as the effects of previous AUD depreciation, higher commodity exports and the housing construction cycle begin to wane, the outlook becomes more uncertain. All of these factors are expected to come to a head around 2018, and the economy will likely require additional policy support from the RBA ahead of this to firm up growth and stabilise the unemployment rate.”

13 September 2016

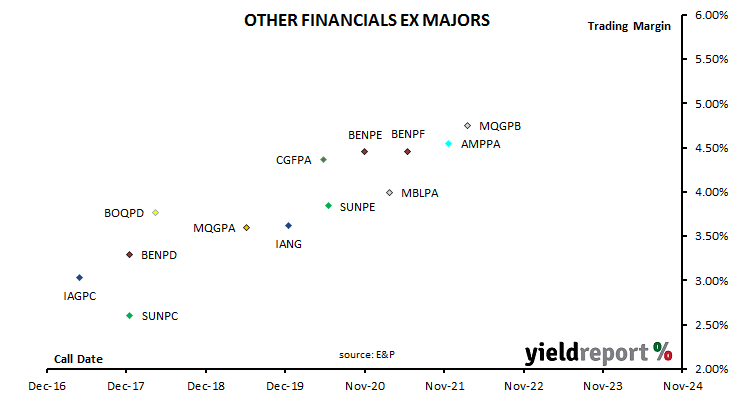

In a recent note to clients Evans and Partners Head of Income Products, Michael Saba, noted how the sell-off in the equity market had produced some higher yields in the hybrids market, especially those which are closer to maturity. “This may present opportunities to gain good short term yield.” He singled out Insurance Australia CPS 2 (ASX code: IAGPC), Bendigo and Adelaide Bank CPS (ASX code: BENPD) and Bank of Queensland CPS (ASX code: BOQPD) in particular. “Further weakness in these will be a buying opportunity.” The chart below shows trading margins at the close of business on 13 September, 2016.

12 September 2016

Bond markets have been reasonably complacent about continued low yields and in recent weeks YieldReport has warned readers that investors might be like ‘frogs in warming water’ whereby they become so used to the slowly changing environment, they don’t see the broader risks until it’s too late.

Last week was one of those sorts of weeks. The RBA left rates unchanged at its monthly board meeting as expected. On Wednesday, Australian GDP numbers showed the economy was growing faster than expected at an annual 3.3%. Bond markets would normally move higher on such news but inexplicably fell on the day. On Thursday the closely watched European Central Bank meeting decided to keep interest rates unchanged and not to increase the amount of bond-buying stimulus. This action began a bond market sell-off that saw offshore bond yields start to push higher and this move saw Australian bond yields push higher.

Following the ECB meeting eyes turned to US markets where a number of Fed governors such as Boston Fed President Eric Rosengren began to make perceived hawkish comments about interest rates. Rosengren is a known ‘dove’ and so his comments were taken as meaning rates a rate rise in September is more likely than it was a week ago. Given the perceived ‘blackout’ of Fed comments in the lead up to the US election, the latest comments are being seen as having a greater implication than they otherwise would have.

All in all it saw US and European bond yields move sharply higher and our market was not immune. 10 year bond yields closed the week up 11bps and early trading on Monday 12 September saw the 10 year bond yield move above 2.00% for the first time in two months. 10 year bonds were trading as low as 1.84% late last week so the latest move has numerous investors asking whether this is the start of a big move higher for bond yields.

Plenty have called the end of the 30 year bond bull market before this and there have been a number of false starts so the latest sharp move, albeit coming off a record low base level of bond rates, is sure to create nervousness among Australian bond investors.

08 September 2016

Investors have become used to seeing bonds trade at negative yields but last week YieldReport saw something that had long-time market watchers scratching their heads.

Two European companies, French pharmaceutical company Sanofi and German consumer goods company Henkel, issued corporate bonds at negative yields. It is believed to be the first time that non-bank corporates have issued negative yielding bonds. Sanofi sold €1 billion of 3 ½ year bonds with a yield-to-maturity of -0.05% while Henkel sold €500 million of 2 year bonds at the same yield.

The market is, in effect, paying money for the companies to borrow the money. It is somewhat mind-numbing to think that investors in Europe are now so worried about the security of their capital or deflation destroying the value of their capital that they see these bonds as a better investment than the alternatives.

Perhaps the more realistic assessment is that traders are simply betting that the European Central Bank will line up to purchase the bonds from traders at an even lower negative yield. The ECB, in its push to provide liquidity for banks to lend money via quantitative easing (or bond buying programme), is purchasing €80 billion worth of bonds per month. In other words, the traders may be looking to generate a capital gain on their bonds by front-running the ECB. As YieldReport has previously noted, markets have become so distorted that investors are buying bonds for capital gains and equities for income.

With the ECB charging banks 0.40% to deposit funds, the commercial banks see better value in investing in almost anything with a higher yield and, in this case, it is corporate bonds. The ECB is buying €80 billion of bonds every months and is rumoured to running out of bonds to buy.

It is estimated that there are around $US13.5 trillion-plus of bonds around the world that are at negative yields with around 1/3 of these in Europe.

08 September 2016

The European Central bank held it September meeting and announced no change to its official interest rate or to its €80 billion per month bond purchase programme. Markets were disappointed that there were no further additions to the ECB’s stimulus and reacted by sending yields higher. The German 10 year yield rose nearly 6bps to -0.05, the equivalent US yield rose 6bps to 1.60% and when the Australian bond market opened, 10 year bond yields rose sharply.

At the press conference following the announcement, ECB chief Mario Draghi said the ECB’s negative interest rate policy “is really working very well. It’s never worked better.” He also restated the scheduled for the monthly asset purchases to run to the end of March 2017, “or until it sees a sustained adjustment in the path of inflation consistent with its inflation aim.”

This means there is no evidence of the ECB looking to expand programme, which means the ECB may face the same issue as the Bank of Japan; a lack of assets to buy. There is a difference, however. In Japan’s case, the BoJ has bought so many bonds and stocks (via ETFs) a de facto nationalisation has occurred, albeit at market value. In Europe’s case, the asset purchase program rules limit purchases and, according to UBS, the Eurosystem may hit holding limits of German debt within the next 6 months.

ANZ Research said, “Despite downgrading its inflation and growth forecasts modestly, and certainly still maintaining an easing bias, it was the fact that the ECB supposedly didn’t consider an extension of its QE program at this meeting that seems to have been what disappointed the market.” Westpac’s Elliot Clarke said, “Market participants are becoming increasingly concerned over the ability of the ECB to continue its asset purchases past early 2017.”