06 September 2016

The RBA left the cash rate unchanged at its September board meeting in a widely-expected decision. Few, if any, economists expected another rate cut so soon after the August 25bps rate cut and so economists and other observers were really only looking for clues as to the RBA’s thinking.

According to Westpac’s Bill Evans the RBA’s statements regarding inflation, employment and the global outlook were unchanged. “Inflation continues to be described as “quite low” and is expected to remain so for some time. Labour market indicators are still described as “somewhat mixed”. The global outlook remains the same. The global economy is expected to grow at a lower than average pace and “China’s growth appears to be moderating”.

However, he does note the change in the language surrounding house prices and hence the likelihood of another rate reduction. “Today’s statement really only provides a reasonable signal that the confidence around housing we saw in August has been shaken a little, slightly lowering the chances of that November cut…Overall we do not expect any change at the October meeting and are also anticipating steady rates in November.”

CBA senior economist Michael Workman took a different view. “The housing market commentary remains interesting….The RBA sees the tighter lending guidelines implemented by APRA as reducing the risks that were building in the housing market. Additionally, the large amount of new supply to be delivered over the coming year, mainly apartments in the major cities, should moderate price growth in that segment. We still expect another RBA rate cut at the November meeting after the next inflation update in late October.”

Cash markets responded to the RBA statement by reducing the likelihood of rate cuts in the short term. After the decision, the probability of an October rate cut edged down to 8%, while a November cut went from 44% to 34%. The months of February, May, August and November are viewed as the most likely months for RBA changes for three reasons; they are placed shortly after quarterly CPI figures are released, they follow the quarterly Statement on Monetary Policy reports and they are the months in which most RBA rate change decisions have been made in the past.

06 September 2016

Buybacks in the semi-government sector have been more popular in recent months; NSW Treasury Corporation bought back $502 million worth of November 2020 capital indexed bonds in late August and QTC last rolled out of $300 million July 2017s and into an equivalent amount of July 2025s in late July. QTC has now bought back another $500 million worth of the July 2017s and issued $500 million worth bonds split over four tranches with maturities from 2023 to 2026.

Pricing was more favourable, which in the context of narrower spreads between ACGBs and semis, is to be expected. Using the pricing of the 2026s as an example, this latest issue of bonds was done at 5bps less than the pricing on the same line in July.

Perhaps this is an end of month thing for QTC. There are now $4.069 billion worth of July 2017s left and about ten months left before their maturity date. The last two buy backs have averaged $400 million so at this rate QTC are on schedule to refinance the 2017 bonds before their actual maturity.

05 September 2016

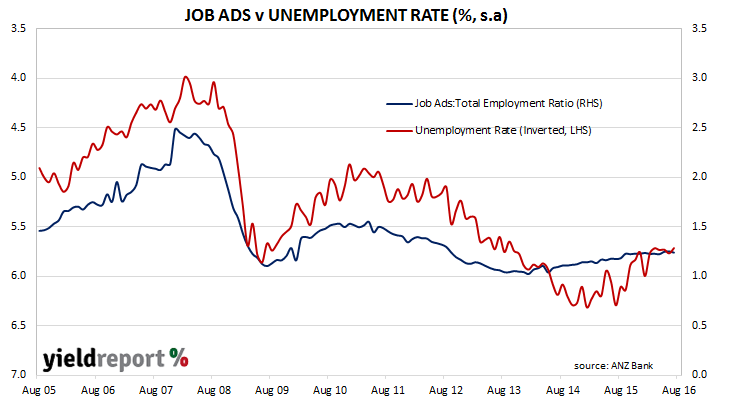

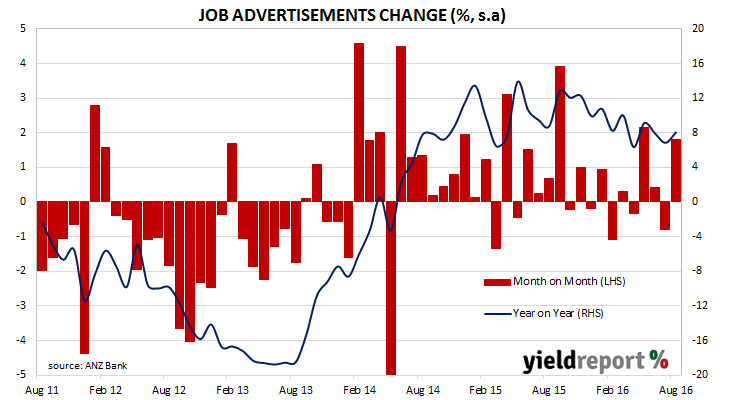

Total job advertisements rose in August after falling back in July, according to ANZ’s monthly jobs ads survey. The month-on-month figure rose by 1.8%, although the year to August figure moved back to 8.0%, or where it was in June. In response, the 3 year bond yield increased by 1bp to 1.43% while the 10 year bond yield moved up 4bps to 1.91% on the day. The AUD was also a little higher.

The survey’s results produce what economists call a “leading indicator”, or a statistic which gives a strong hint as to the future direction and strength of the economy. In the case of ANZ’s job ads survey, it provides a preview of conditions in the employment market, especially with regards to employer demand for labour. More advertisements generally means more hirings, a stronger economy ahead and thus lower unemployment rates.

After the release of the previous report for July, ANZ’s Head of Australian Economics, Felicity Emmett had predicted job advertisements would rebound in August on the back of a cut in the official rate and solid business conditions. After the August results she said, “The rise in job ads is consistent with the ongoing strength in business conditions and increasing capacity utilisation reported in the business surveys….Overall, this is consistent with our view that the unemployment rate will slowly improve over the next year, supported by low interest rates and solid business conditions.”

31 August 2016

Nissan withdrew from Australian car manufacturing over a decade ago to service the local vehicle market purely through imports. This week, however, it returned to Australia in a sense for a transaction in local financial markets. Nissan Financial Services usually issues bonds denominated in yen or USD but in Nissan’s debut in the domestic bond market the Australian arm issued $300 million worth of September 2019 fixed-rate bonds.

The issue was priced at Swap + 100bps and it was arranged by ANZ and Westpac. The sale in the local bond market is a welcome increase in the diversity of investment-grade bonds available for investors and it follows other recent debuts by Apple and The Coca Cola Company. Nissan Financial senior bonds are rated A- by S&P Global Ratings.

30 August 2016

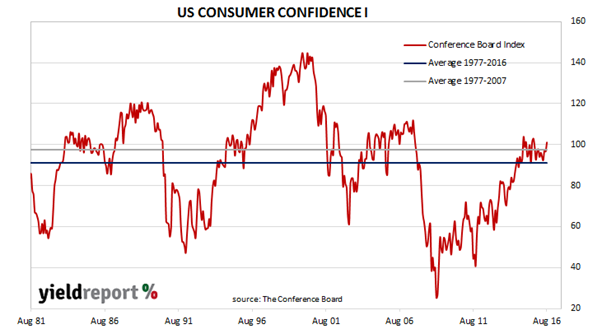

Consumer confidence surveys are important private sector surveys even though economists view them as lagging indicators. Their importance lies in the confirmation of spending patterns and as consumption in developed countries may amount to 60%-70% of GDP, knowing how it behaving is important for financial markets’ forecasts for GDP growth rates, which in turn flow into demand for credit and inflation rates.

The latest release from the US Conference Board’s August survey is especially important in light of the US Fed’s stated “data dependent” approach to normalising US official interest rates. The August reading came in at 101.1, up from July’s revised reading of 96.7 and considerably higher than the market forecast of 97.0.

Since the GFC survey results have not been consistently over 100 and the months in which the index has been above 100 have been sporadic, the most recent one in August 2015. Lynn Franco, Director of Economic Indicators at the Conference Board noted the figures suggested a rise in consumer spending in coming months could be expected. “Consumers’ assessment of both current business and labour market conditions was considerably more favourable than last month. Short-term expectations regarding business and employment conditions, as well as personal income prospects, also improved…”

Despite the higher-than-expected figure, the US bond market’s reaction was mixed. 2 year yields fell 2bps and 30 year yields rose 1bp on the day, although how much the moves were caused by the report and how much was caused by the US Fed vice chair’s comment regarding the US economy at near full employment is debatable.

26 August 2016

The core CPI in Japan has dived to -0.5% year on year in a worrying sign for the world’s 3rd largest economy and putting pressure on the government of Shinzo Abe to follow through with more stimulus.

The monthly CPI fall for July was 0.4% (annualised). This was the fifth consecutive monthly fall.

25 August 2016

Fortescue has made another step in the direction of corporate respectability. Moody’s has raised the credit rating of the iron ore producer to Ba2/stable and, while this rating is below “investment grade”, Fortescue needs two more upgrades to reach this target.

Moody’s Senior Credit Officer Matthew Moore said Fortescue’s debt strategy had led to the ratings upgrade. “The upgrade to Fortescue’s ratings reflects the considerable progress that the company made in reducing its debt levels in fiscal 2016 and Moody’s expectation that it will continue to reduce debt further in fiscal 2017.”

Fortescue CFO Stephen Pearce said, “You’ve seen our credit improve quite significantly over the last twelve months and you would expect that ratings would follow.” S&P Global Ratings currently rate Fortescue senior long term debt as BB after a downgrade was issued in April 2015 from BB+.

25 August 2016

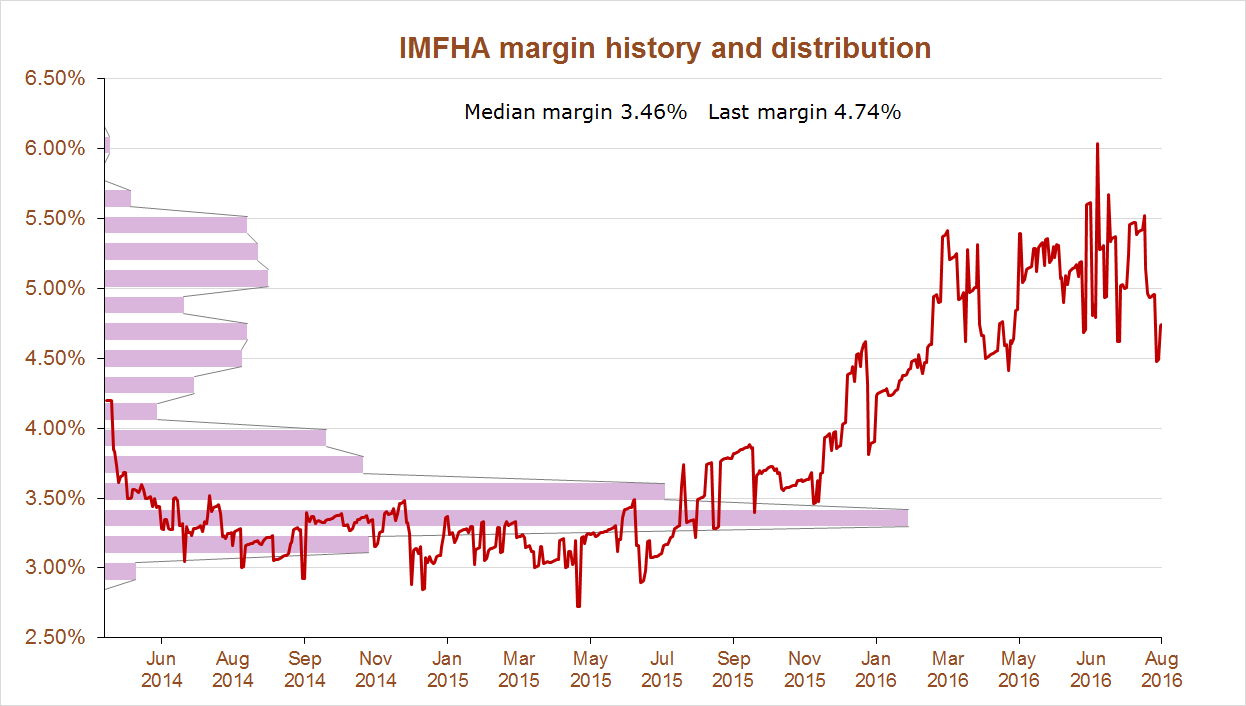

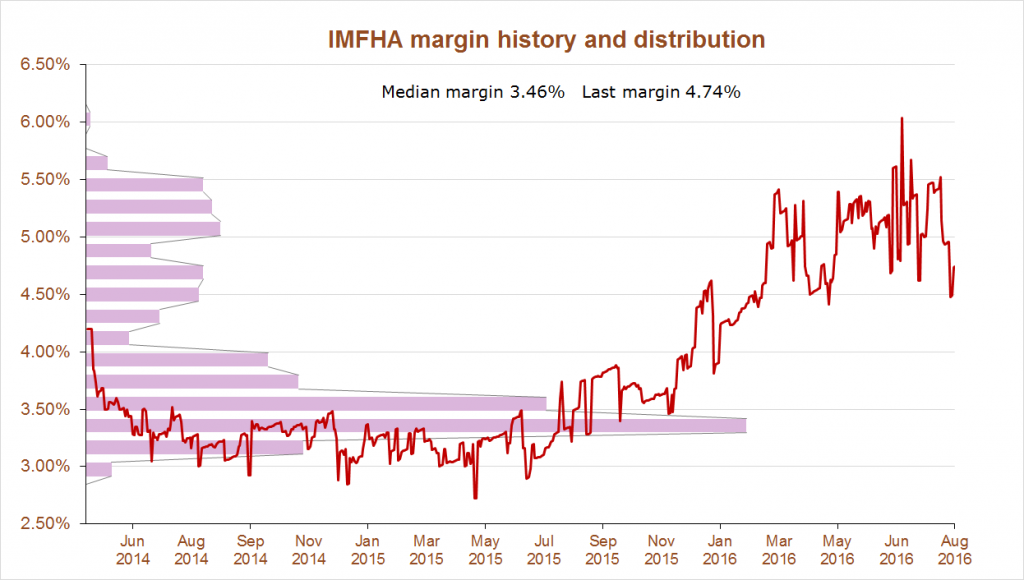

Fixed income broker Evans and Partners thinks the bonds issued by litigation funder IMF (ASX code IMFHA) might be worth a look. In a recent note to clients E&P pointed out the bonds were issued in 2014 at a 420bps margin to BBSW. “The trading history as below shows the margin widened in 2016 to well over 5% at times. This was a function of a falling share price over 2015 (especially late) and poor credit markets in the first quarter of 2016. Subsequently the markets and the share price have recovered strongly with the share price up 30% so far in 2016. The notes margin has just started to improve and given the thirst for yield [it] may have some more room to fall to levels seen in 2014.” On current trading margins the yield is around 6.50%. Investors will note that the recent ANZ hybrid was issued at an initial yield of around 6.45% and might ask why the IMF bonds would seem appealing. One of the answers lies in the fact that the IMF notes are a senior debt obligation and therefore higher in the capital structure than the ANZ hybrid.

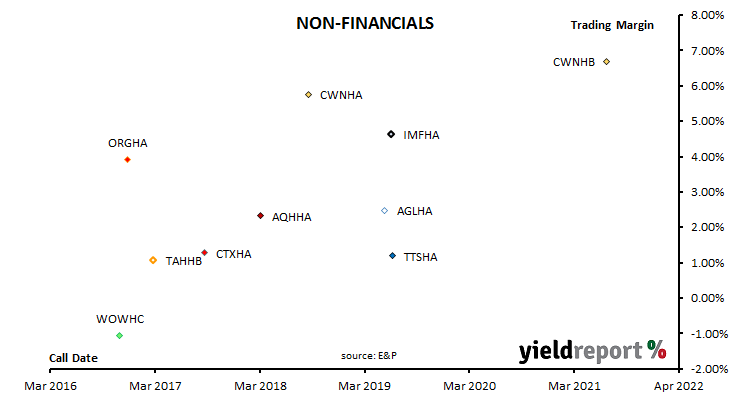

Here’s another chart as at 24 August for the sake of comparison with other notes trading on the ASX.

23 August 2016

The prospect of an Australian 30 year bond has emerged again. After an investor update held in Hong Kong, Australian Office of Financial Management chief Rob Nicholl, was reported in the media to have said a 30 year bond would likely be issued by June next year. When YieldReport checked with the AOFM about the accuracy of the report, the agency was a little coy but did confirm that lengthening the yield curve out to 30 years was always under “active consideration”.

It has been suggested to YieldReport that several life offices and superannuation funds have spoken with the AOFM to offer support if such an issue were to eventuate. Given the investment mandates of many of these funds and those of foreign buyers such as from Japan, finding support would seem to us to be a given.

From 2012 onwards, the AOFM has been lengthening the average maturity of its debt and given the state of sovereign yields it is not a surprise that issuers would think of locking in a historically low financing rate for an extended period of time. Currently the longest dated ACGB on issue is the June 2039 series.

The introduction of a 30 year bond was flagged by the AOFM chief in a May 2015 Australian Business Economists speech where he said the introduction of a 25 or 30 year line was likely in the “coming year”. Just over a year later, nothing has eventuated.

Deutsche Bank strategist David Plank said the extension of the Australian yield curve would have some impact. “Indeed, the recent bounce in the 10Y/20Y bond slope may have been in anticipation of maturity extension by the AOFM.” However, he expects when such a bond issued, the effect on the yield curve will be only “modest”.

22 August 2016

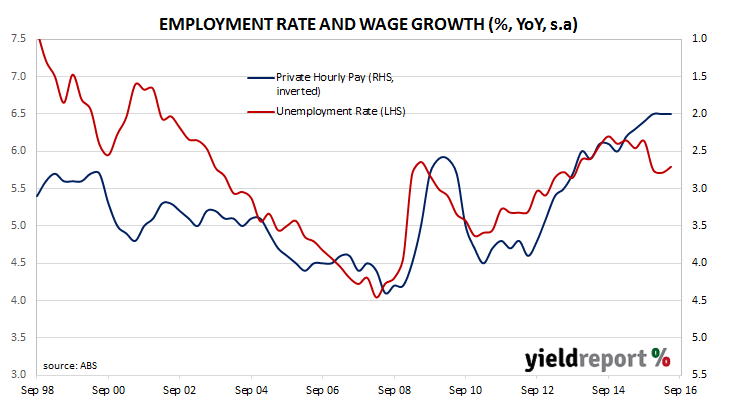

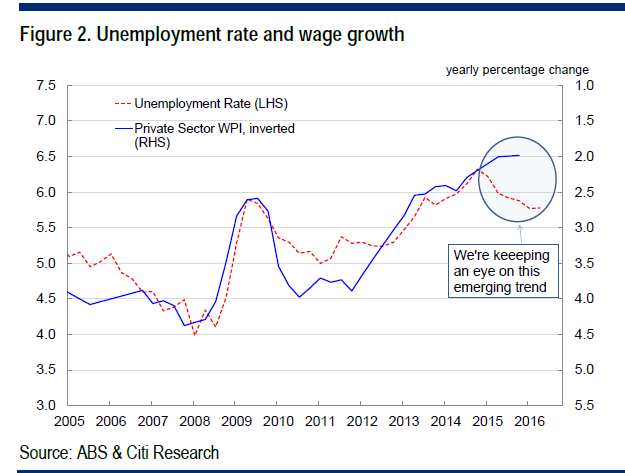

YieldReport loves a good chart where two separate economic variables line up with each other, thereby illustrating a firm relationship between the two. After the release of wage inflation figures, Citi Research put together a chart of the unemployment rate against private sector hourly wage inflation. Citi thinks there’s a good fit between the two or, for the technically minded, a high correlation and their chart seems to indicate this. Recently the unemployment rate has fallen (red line below), diverging from private sector wage inflation (blue line) and as citi notes in their chart, they are keeping “an eye on this emerging trend”.

Wage inflation is important in developed economies as a major cost component for businesses is the wages and salaries bill. Wages growth will either cut profit margins or lead to price rises or a combination of both. Inflation is defined as a general rise in prices so higher wages may lead to inflation in the absence of productivity gains. Central banks, including the RBA, are currently obsessed with raising inflation and so any early indicator of future inflation is of interest and perhaps that’s why Citi thought the relationship between unemployment and private sector wages growth worth studying.

YieldReport thought it may be interesting to look a bit further back to when the hourly rate of pay survey was first introduced in 1998 and this is what it looks like: