14 July 2016

The number of primary market transactions with a yield below zero have been small and mostly limited to shorter- dated bonds. In only one country, Japan, have 10 year bonds been sold at negative yield in a primary market transaction. Now there is another. Germany issued zero coupon 10 year bonds at a yield-to-maturity of -0.05% during the week. The price investors paid for these bonds will exceed the face value received ten years from now. Buyers either believe the yield will fall further and the bonds will increase in value or they do so in the belief deflation will accelerate over the life of the bond.

In early May we published a short list of countries with negative yielding bonds and there were ten countries in the list. All of them are European except for Japan. While many of those countries’ bonds have been trading on secondary markets at negative yields for some time now, 10 year bonds get more attention as they are used as the benchmark yield for all sorts of assets. Not just in the fixed interest markets but also in the equity and property markets. So when the 10 year yield goes negative more people take notice. Japan’s economy has been stagnating since the early 1990s and to some degree a negative yield for longer-term bonds has been viewed as an aberration particular to that country but bonds markets are increasingly predicting the “Japanfication” of Europe.

12 July 2016

Krone-denominated bond issues are quite common…in Norway and Denmark. In Australia, a corporate issuing bonds in the Norwegian version of the currency is quite unusual, although it has been known to happen from time to time. For instance, AusNet issued NOK900 million (AUD$160 million at the time) worth of June 2029s in mid-2014. However, one bond issue every two years does not a plethora make.

In any case, Transurban has announced it has priced NOK750 million ($117 million) worth of 2027 bonds via a private placement. Transurban said it would swap the proceeds into Australian dollars and then reduce existing bank debt. It also noted the transaction would further diversify its funding sources and currencies.

Whilst the buyer of the bonds has not been identified, market watchers have pointed to the Norwegian sovereign wealth fund – one of the largest in the world – as the obvious buyer.

Perhaps other Australian borrowers will see the attractions of issuing krone-denominated bonds. However, for the time being, the practice will still be seen as somewhat on the exotic side until other issuers give it their approval by issuing their own krone bonds.

12 July 2016

Australian businesses are benefitting from a combination of a low exchange rate and low interest rates according to according to NAB’s latest Monthly Business Survey. NAB’s Business Conditions Index moved two points higher to 12 and the Business Confidence Index rose 3 points from 3 to 6. This was in spite of the survey being carried out immediately after the UK’s EU vote and amid the uncertainty of the lead-up to the Federal election.

Alan Oster, NAB’s chief economist said, “The results point to further improvement in the non-mining economy in Q2, with growth potentially becoming more broad-based – although evidence is mixed.” Mr Oster thinks while the RBA’s August meeting is “live”, rates will remain unchanged, although he acknowledges the decision will be a close call.

Andrew Hanlan, a senior economist at Westpac said, “This confirms that the non-mining sectors are benefitting from low interest rates and a sharply lower currency. Importantly, the dip in conditions evident late in 2015 and in early 2016 has proven to be a temporary soft spot.”

Not all businesses are doing so well, however. Business conditions are still negative in Western Australia, a hang-over from the end of the mining investment boom but in all other states, conditions are positive. Especially in New South Wales and Victoria.

Bond and currency markets reacted to the new figures in a manner which suggest higher interest rates are more likely. The AUD immediately rose from 75.7 US cents to 75.9 US cents while implied yields on 3 year bonds rose 3bps to 1.51% and yields on 10 year bonds rose 4bps to 1.95%.

11 July 2016

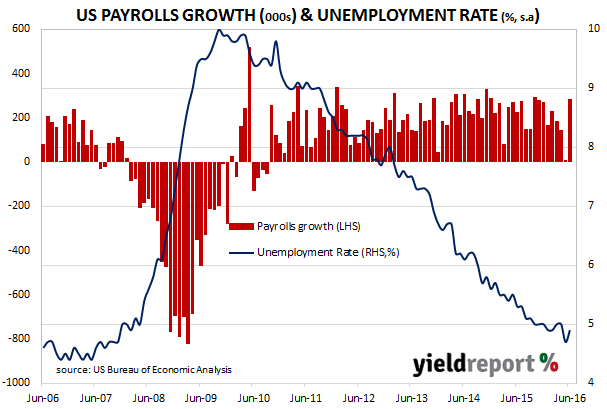

Unemployment in the US rose from 4.7% in May to 4.9% in June even though the US created another 287,000 jobs in June. The number of jobs created far exceeded consensus forecasts of around 180,000 and while US 10 year bond yields initially rose on the news to 1.44%, they soon traded back lower to finish the day at 1.36%, down 3bps. The 2 year bond yield also fell back after the initial rise to 0.65% but still finished up 2bps at 0.61%.

Westpac’s fixed income trading desk referred to the bond market reaction as “astonishing” but senior economist Elliot Clarke pointed out the report contained both positive and negative aspects; jobs growth was higher than expected but the unemployment rate rose all the same; the participation rate was higher but the percentage of the entire population in work was lower. “All told, the June employment report reasserts that the US employment market remains in robust shape….For the FOMC, this is not enough to justify another rate hike; but it does allow them to keep their options open.” NAB took a similar view. “The data was seen as validating a continued wait-and-see approach from the Fed, with no US primary dealer surveyed after the data believing the Fed will move before December…”

11 July 2016

The pace of corporate bond issuance appears to be picking up as the third of the four major banks has announced a large USD transaction. This time it is ANZ and it is in the form a two-tranche deal with one 3 year tranche worth $1 billion priced at US Treasurys + 85bps and a 5 year tranche worth $500 million at US Treasurys + 97bps.

When NAB was the first of the majors to conclude a substantial deal after the British EU referendum, some observers noted the pricing and commented on the higher spread. In May ANZ issued USD-denominated bonds which included a USD$850 million tranche of 5 year bonds which were priced at Treasurys + 95bps and, as with NAB’s recent issue, ANZ will pay more on this latest offering. However in this case it appears ANZ has got a better deal on the 5 year component.

08 July 2016

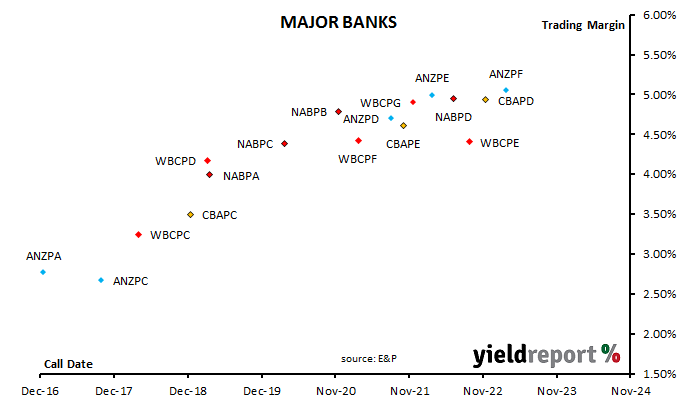

NAB’s newest hybrid issue, Capital Notes 2 (ASX code: NABPD), began trading on the ASX today. With a first call date of 7 July 2022 and an issue margin of 4.95%, trading in the hybrids began on a deferred delivery basis. Normal trading is expected to begin on 12 July. The first trade was at $100.50 and the hybrid closed the day at $100.35, a modest gain from the $100 issue price.

NAB’s new issue was announced only a few days after Westpac’s Capital Notes 4 offer was made public. Between then and now, financial markets around the world have experienced some severe gyrations in the wake of the Brexit vote. NAB and Westpac applicants may have had a few sleepless nights over the last few weeks but the first few days of trading in Westpac’s capital Notes 4 (ASX code: WBCPG) will have eased any anxiety Westpac holders may have been feeling and given some comfort to NAB applicants. Westpac’s notes started trading at a modest premium and have stayed above face value in trading to date.

The NAB issue raised approximately $1.5 billion and the first distribution payment date is set for 7 October 2016. The chart below shows how trading margins stood at the end of NAB’s first day’s trading. For the technically-minded, the issue date volume-weighted average NAB share price, the price used to determine the maximum conversion ratios and the satisfaction of mandatory exchange conditions (in the event of the hybrids being converted to shares) has been announced as $25.27.

06 July 2016

This week’s release of the minutes from the July FOMC meeting was greeted with less enthusiasm than usual. The minutes did not provide any new insights into Fed officials’ thinking and only served to confirm markets’ views of FOMC thinking; a weak employment report from May had raised uncertainty among Fed officials and this, along with the then upcoming UK EU vote had added weight for a decision to delay raising US interest rates. Perhaps the most interesting thing to come from the minutes is the level of disagreement among FOMC members. Some officials thought employment gains in May possibly understated the underlying pace because of one-off events but others saw the numbers as “indicative of a broader slowdown in growth of economic activity.” Westpac described the minutes as being in line with Janet Yellen’s “cautious yet hopeful” narrative.

Ahead of the release, prices in US cash markets were implying no chance of a July rate rise and a small chance of a rate cut. This remained the case after the minutes were made publicly available. This is a far cry from the 51% probability attached to a July rise after the release of May’s minutes. US bond rates went marginally higher on the news. 2 year yields rose 2bps to 0.58% and the 10 year yield rose 1bp to 1.37%. The US dollar was weaker against most other currencies.

The UK vote has moved markets to take a view the Fed is less likely to raise rates and, as the minutes pre-date the vote, the market is somewhat dismissive of a meeting which did not have access to new information which the market deems important. Locally, Westpac said, “There’s not much new here, and given the meeting pre-dates the UK Brexit vote, [it] is somewhat stale.” NAB were almost as excited as Westpac. “…perhaps the most that should be said about them is the ‘uncertainty’ word count reached a new high of 13. They were completely non market-moving.

06 July 2016

Corporate issuers were thin on the ground in the weeks before the UK EU vote but now the vote is out of the way and despite some lingering uncertainty, issuers have returned. If NAB’s latest bond sale is indicative of conditions, then conditions are basically back to normal, even though some commentators have suggested spreads have widened.

NAB was one of two of the major banks which completed large bond sales this week. It issued USD$4 billion of bonds via four tranches of fixed and floating bonds to investors in the US market. The tranches comprised 3 year bonds priced at Treasurys + 85 bps, 10 year bonds at Treasurys + 122 bps, 5 year fixed-rate bonds at Treasurys + 100 bps and 5 year floating-rate bonds at US Libor + 100 bps. By all accounts, the issue was well bid, with around $10 billion of orders, so there was no shortage of investor interest.

Margins may have risen a little in the last few months but not in any substantial manner. In May ANZ issued 5 year fixed and floating bonds into the US market. The fixed-rate bonds were issued at Treasurys + 95bps, while the floating-rate notes were done at Libor + 99bps, so while NAB’s latest offering may be a tad more expensive, it may be a little bit of a stretch to suggest margins have widened noticeably. Coincidentally, a similar package of 3 year and 5 year bonds NAB issued in July last year was priced at identical spreads to Treasurys, only in that case there was no 10 year bond tranche.

06 July 2016

The latest Inflation Gauge reading for June indicates consumer prices rose 0.6% during the month.

Petrol prices rose 7.6%, travel and accommodation prices rose 7.4% and fruit and vegetable prices rose 6.4%, while items whose prices fell did so in very small amounts. On the day, yields implied by 2 year bond futures rose by 5bps to 1.51% while the implied 10 year yield rose 6bsp to 2.02%.

12 month inflation (blue line below) reversed the course set in the last few months and rebounded back to 1.5% after reading 1.0% for the year to May. The trimmed mean measure of the Inflation Gauge rose by 0.2 per cent in June, after falling by an equivalent amount in May.

Dr Sam Tsiaplias, Senior Research Fellow at the Melbourne Institute, pointed to petrol prices and forecast the next CPI figures released later this month would be positive. “Given this rise, it seems unlikely that we will get a repeat of last quarter’s negative CPI result for the current quarter… Both trimmed mean inflation and the inflation gauge excluding volatile items rose this month, although they are still below their long‐term averages.”

06 July 2016

One month ago at the June meeting, the RBA left the official rate steady at 1.75% in a widely expected decision. While there was no change made to the cash rate, what caught pundits’ attention at the time was the lack of an “easing bias” which had previously been present in statements which accompanied prior announcements. Westpac had been expecting something from the statement in this regard. “While the cash rate is unlikely to move…The key question here is whether the Board chooses to make more ‘forward-looking’ comments and/or signal a clearer easing bias.”

In this week’s RBA July meeting, once again the official rate was left unchanged at 1.75%. There were some changes to the language and tone of the statement but there was no consensus as to whether an easing bias had been re-introduced. ANZ thought there had been. “The reintroduction of an explicit easing bias, albeit a soft one, into the RBA’s post-meeting statement yesterday opens the door to an August rate cut.” It was a view shared by JP Morgan’s Ben Jarman. “The guidance today more explicitly represents a data-dependent easing bias… Given the trend in core inflation we expect over the next year, this is consistent with the cash rate moving toward 1% as per our forecast.”

Paul Brennan from Citigroup took a different view. “There was some speculation that the easing bias would be reinstated, but in our view this was not likely given the glass half full commentary on the domestic economy from the June Board Minutes…The rise in house prices since the May cut was noted again by the Governor. We believe this is something that the RBA will be closely watching, and which will need to be considered in coming to a decision on any changes to policy.”

A commonly-held position amongst Australian economists is the RBA will not move until June quarter CPI figures are released in late July. ANZ Research summed-up this view after the RBA announcement. “The Q2 CPI is crucial to the decision, but we expect that weak inflation and rising uncertainty will see the RBA cut the cash rate to 1.5% next month.”

Domestic cash markets reacted in a manner which suggests a little more doubt has crept in, albeit in a technical sense, by reducing probabilities of rate cuts in any given month. The market still rates the chance of a rate cut as good, with prices implying an August rate cut as a 51% chance (down from 58%), while a September cut went from 70% to 61%. However, a 25bps rate reduction is fully factored in for December.