23 June 2016

The last twelve months has provided a few examples of large corporates buying back bonds prior to maturity. Rio Tinto and Fortescue have both bought back bonds worth billions of dollars and, in Rio’s case, only just recently. The individual reasons vary but with yields at historic lows the actions suggest that companies believe this is the best use of their excess funds. It says a lot about the opportunities for business to grow.

Barclays Bank plc has now joined the growing list of issuers reducing their outstanding bonds. Through its Australian branch, Barclays has just announced the repurchase of $261.88 million 4.50% April 2019s and $235.15 million April 2019 FRNs. The buy-back leaves $338.12 million worth of fixed rate notes and $464.85 million worth of FRNS outstanding.

First flagged at the start of June, Barclays said the transaction was made as part of the “group’s ongoing transition to a holding company capital and term funding model in line with regulatory requirements”. Barclays announced in April it would be converting to a two division structure, with one division to house the UK bank and the other left with everything else. The notes not repurchased will be transferred from the Australian branch which issued the notes in April 2014, to Barclays Bank plc.

Barclays Bank was rated A by S&P and A2 by Moody’s at the time of the 2014 issue. It has since suffered a one notch downgrade but its Moody’s credit rating of A2 remains intact.

22 June 2016

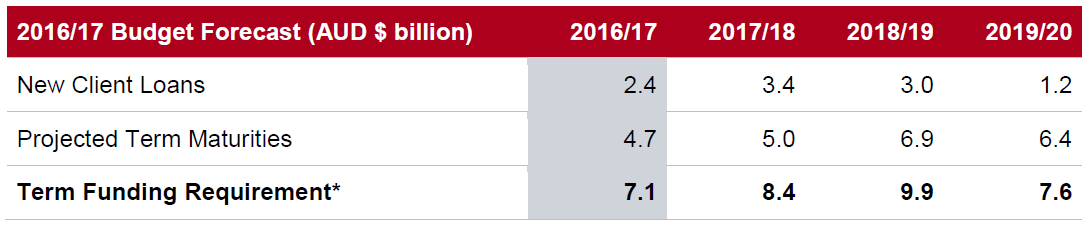

Despite swimming in property sales stamp duty, NSW will be issuing just over $7 billion of debt in the 2016/2017 year. One of two state governments with a AAA rating, NSW has now released its funding requirement for the next financial year and the three years which follow. The figures don’t take into account proceeds from proposed long term leases of AusGrid and Endeavour and therefore the actual amount of new debt issued may well be vastly different.

Of the $7 billion of debt expected to be issued, $4.7 billion will be to cover existing debt which reaches maturity during the financial year and another $2.4 billion will be issued as new, additional debt. However, TCorp said the funding requirement would be “materially affected” by the finalisation of leases for AusGrid and Endeavour as these leases would trigger the repayment of outstanding loans made to the businesses by TCorp, which is the financing arm of the NSW Government. The loans are worth around $9 billion for AusGrid and just over $4 billion for Endeavour.

21 June 2016

Unlike the minutes of the RBA‘s May meeting, minutes from June meeting contained little in the way of any new information. According to Westpac “The minutes to the June monetary policy meeting of the Reserve Bank Board were largely as expected, repeating the key themes and wording of the Governor’s decision statement and providing no explicit guidance on the outlook for policy.”

While there was little to chew on, the minutes did clearly acknowledged the upside surprise on GDP growth. “Members began their discussion of the Australian economy by noting that growth in real GDP in the March quarter was stronger than anticipated in the May Statement on Monetary Policy.”

However, at this stage economists are still expecting the RBA to ease monetary policy further and cash markets are still largely factoring in 25bps of cuts, although prices are currently indicating a little less certainty than before the minutes were released.

JP Morgan economist Sally Auld said, “The RBA acknowledged in the minutes that leaving policy unchanged in June was consistent with returning inflation to target over time.” Even so, she thinks a rate cut is coming. “… recent currency strength and the latest iteration of the Fed’s re-think of how rate normalisation is likely to proceed will mean that the current pause is relatively short lived, and that risks continue to remain biased towards a cash rate of 1% in 2017.” Westpac’s Matthew Hassan does not think the RBA will cut quite that far. “[It] remains our assessment that the June quarter inflation read will reconfirm to the Board that, on a ‘no policy change’ basis, inflation is unlikely to return to the Bank’s 2%-3% target over the forecast horizon and that another 0.25% cut is necessary with that cut being delivered at the Board’s meeting on August 2.”

Click here for the full version of the June minutes.

21 June 2016

An interesting take on the Brexit polls from Singapore-based fund manager, Stephen Fisher of First Degree Asset Management. In his blog, Mr Fisher looks at the pre-vote polling on the UK’s plebiscite and why in the past, pre-vote polls have been ‘way off the mark’ when it comes to the actual result.

Financial markets around the globe have been fixated on the Brexit poll and the potential effects of Britain leaving the European Union. Volatility has increased markedly as investors position themselves ahead of the vote. On one side of the argument you have the ‘remain’ vote, characterised by some as ‘Project Fear’ , scaring voters as to the great cost to the nation if the UK votes to leave and supported by Prime Minister David Cameron. On the other side is the leave vote, characterised by Britain’s lack of sovereignty over its laws and borders and the unhealthy dominance of British life by the ‘superstate’ EU. The major supporter is Boris Johnson, the recent former mayor of London.

The UK votes on Brexit on 23 June 2016 with the polls closing at 7:00am on Friday 24 June (AEST). New Zealand and Australia will be the first markets to react to the result.

A link to Stephen Fisher’s blog can be found here.

17 June 2016

Elders has announced it has raised $102.4 million via a share placement and rights issue in order to fund the repurchase of its hybrid securities at $95.00 each. Elders CEO Mark Allison said, “The proposed simplification of our capital structure is the final step in the transformation of Elders from the complex and highly-geared conglomerate it once was to the simplified and efficient business we now are.”

15 June, 2016

Back in the days when Elders was known as Futuris, it issued convertible unsecured notes with discretionary, non-cumulative distributions and a face value of $100. When the company hit hard times in 2009 and stopped paying distributions on the hybrids, the price plummeted and remained a fraction of its face value for years. Only when the company announced a buyback of $30 million worth of the hybrids at $80 in August last year did the price recover.

Now Elders has announced its intention to make another buyback offer. Details have not yet been released but the last sales price before trading on the ASX was halted was $89.00, so a higher buyback price is to be expected. The previous buyback was “on-market” due to Corporations Law restrictions and purchases were made on a first come first served basis.

One issue for long-suffering holders is whether to accept the buyback terms or to remain as holders. Back in 2011 when the Elders did not implement a remarketing process as the first remarketing date approached, under the terms of the prospectus the distribution rate was stepped up by 250bps. Now another remarketing process has not been initiated, another step-up amount of 250bps has been added, which takes the margin to 720bps. At this stage the margin is notional as distributions are at the discretionary of directors and one has not been paid since 2008. However, before ordinary shareholders can be paid a dividend, hybrids holders have to have received at least 12 months’ worth of distributions. This may put pressure on directors to resume hybrid distributions. In any case, this is a security not for the faint-hearted.

17 June 2016

US inflation rose less than the 0.3% expected in May, according to the latest consumer prices index (CPI) figures released this week by the US Labor Department. The headline CPI rose by 0.2%, taking the year-on-year rate to 1.1%.

Core inflation, which strips out food and energy price changes, began to accelerate again after slowing in March and April. The annual rate rose back to 2.2% after dropping to 2.1% in April and any further increases in its rate will take it back to pre-GFC levels.

The index is based on prices of food, clothing, shelter, fuels, transportation fares, charges for medical services, medicines, and other goods and services bought for day-to-day living. The largest price increases were in the fuels and rents segments.

AMP Capital’s Shane Oliver said the figures were consistent with a core PCE figure of between 1.6% and 1.7%. Core PCE (underlying personal consumption expenditure) is known to be the FOMC’s preferred measure of inflation and thus useful as an indicator of FOMC’s policy leanings.

In a week in which markets increasingly focussed on the upcoming “Brexit” vote, US CPI figures registered on few radars, especially as the numbers were not far from those which were expected. On the day, US 2 year bond yields rose 3bps to 0.69% while 10 year bond yields rose 3bps to 1.58%.

16 June 2016

The two series of Crown notes (ASX codes: CWNHA, CWNHB) have been put through the wringer since speculation arose in November 2015 of a privatisation bid by the James Packer camp. A privatisation bid was viewed as potentially leading to more highly geared structure, which is generally viewed as being unfriendly to debt holders

The latest announcement by Crown seemed to have put all this concern aside. Crown plans to demerge into two entities with Crown Resorts owning the Australian operations and another yet-to-be named company holding the international businesses. There is also the possibility of a separate property trust being set up to sell a 49% interest in the Casino’s Australian properties.

Westpac summed up a typical reaction. “This provides a positive boost on two levels; firstly, we have a resolution and secondly, we have a resolution that is bondholder friendly.” Evans and Partners view was pretty much the same. “The announced transaction has removed previous downside risk for hybrid holders.”

The yields on both series of Crown notes plummeted on the day as the prices of the two securities rocketed. The day before the announcement, according to Evans and Partners, series I notes (ASX code: CWNHA) and series II notes (ASX code: CWNHB) had trading margins of 8.65% and 10.07% respectively. By the end of the next day, these margins had dropped to 6.59% and 7.43% as investors decided risks associated with the notes needed a re-assessing.

Crown’s presentation of its intended strategy made it clear they had debt holders in mind. When outlining its dividend policy Crown said, “The adoption of this new dividend policy does not alter Crown Resorts’ intention to maintain a strong balance sheet and credit profile…” Apart from this pledge, Evans and Partners’ credit analyst Harry Dudley said the dividend policy “extinguishes any doubt that Crown has a plan to stop paying dividends to then be able to remove coupons on hybrids.” It should be noted that James Packer is said to own around $150m of the series II Crown Notes.

The one negative out of plan was Standard & Poor’s and Moody’s move to place Crown on negative watch. S&P said any downgrade would be limited to one notch. Referring to the rating agencies likely moves Westpac said, “Regardless of the short term rating outcome, this transaction will remove the potential for a significant downward rating move from Crown which will remain supportive of spreads.

Related articles

Crown notes speculation

Crown series 2: how far will they go?

Hybrid securities cop fallout from share market sell-off

Crown notes 13% yield not for the faint-hearted

16 June 2016

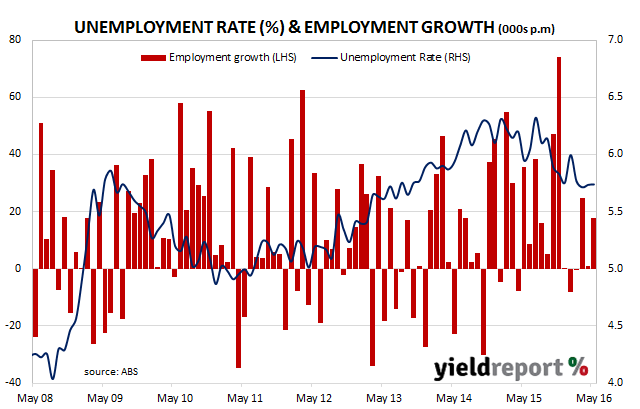

Australia’s job market expanded again in May, with an extra 17,900 new jobs in net terms. The growth in employment and a steady participation rate at 64.9% kept the seasonally-adjusted unemployment rate steady at 5.7%. The job figures were more than the 15000 expected but, as with the figures in April, the composition of the increase are a source of concern to analysts. Part-time jobs were entirely responsible for the increase but unlike April’s figures, full-time jobs remained steady in May. Monthly hours worked in all jobs rose by 27.7 million hours to 1,643.1 million hours.

Commonwealth Bank noted the downward revisions to previous months’ data. It also singled out a “sharp rebound” in reported hours worked but put this down to sampling process issues in April. With markets largely fixated on the upcoming “Brexit” vote, the numbers were largely ignored, although yields on 3 and 10 year bonds did fall 5bps and 7bps respectively on the day.

15 June 2016

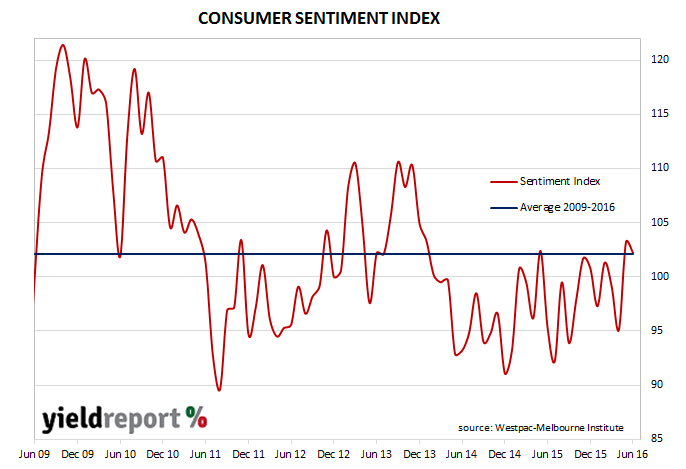

The latest Westpac Melbourne Institute consumer sentiment survey shows a small decline to 102.2 from May’s reading of 103.2. Any reading above 100 indicates the number of consumers who are optimistic is more than the number of consumers who are pessimistic. The fall was partly driven by consumer’s views of economic conditions over the next year and over the next five years.

Westpac’s chief economist Bill Evans said it is common for consumer confidence to slip back a touch the month after an interest rate cut and the resultant surge in confidence. “Coming after an 8.5% surge in May, the small decline in June mostly represents a consolidation at improved levels.” He also singled out the “family finances” component, which he believes the RBA pays particular attention to as an indicator of demand, noting the 4.3% increase over the last month

Westpac is currently expecting the June quarter CPI figures to provide the RBA with the ammunition required to cut the official rate to 1.50% in August. Australian 10 year bond futures finished the day at 97.9175, implying a yield of 2.0825%.

14 June 2016

The ongoing recovery in the non-mining sectors of the economy continues and remains close to “post-GFC highs” according to NAB’s latest Monthly Business Survey. Its Business Conditions Index remained at 10 (April’s figure was revised from 9 to 10), while the Business Confidence Index fell 2 points from 5 to 3.

NAB chief economist Alan Oster said the drop in confidence was mostly limited to the manufacturing and transport sectors while other forward indicators such as spare capacity were “reasonably good” and noted signs of a moderate pick-up in inflation.

Westpac senior economist Andrew Hanlan thought the numbers suggested business conditions were “positive outside of mining and construction” and added, “This confirms that the non-mining sectors are benefitting from low interest rates and a sharply lower currency.” He too noted the fall in spare capacity, although he linked it to weak investment spending.

Australian bond yields generally ignored the positive result and followed offshore leads. On the day implied yields on 3 year bonds dropped 3bps to 1.55% while yields on 10 year bonds fell 5bps to 2.05%.