31 May 2016

All four major banks have now either recently issued hybrid securities or are in the process of issuing hybrids. ANZ is one that has announced it too will be issuing a hybrid security however, unlike the other major banks, ANZ will be making the issue offshore and in USD.

This is the first time for many years that a foreign currency hybrid will be issued will be issued by an Australian bank and comes as a result of an Australian Tax Office ruling that will allow distributions not to be franked. For some time, there have been rules in place to stop companies ‘streaming’ dividends – for example paying an unfranked dividend to an offshore share holder and paying franked dividends to a domestic shareholder – and as YieldReport understands it, the Private Binding Ruling allows the banks to now pay unfranked distributions on hybrid securities to offshore holders. Evans & Partners say the ATO’s requirement to frank such issues has been waived and this is of great significance for hybrid issuers. “The implications for the Australian market, wholesale and listed, are that the banks can now satisfy their AT1 (Additional Tier 1 capital) requirements in two markets rather than mainly the ASX…Going forward the banks will issue in all open hybrid markets in a regular fashion rather than be subject to roll-over risk and potentially a poor market at that time.”

Some of the benefits of issuing offshore, especially in USD are obvious; US markets are deeper and more liquid so funds can be raised more quickly and without moving prices in the market. Other incentives for issuers include being able to diversify one’s funding base and potentially lower transaction charges. In a further twist, the contingent convertible securities, otherwise known as CoCos, will be issued out of ANZ’s London branch. The term contingent convertible refers to the clauses which force conversion into common equity. These clauses are comparable to common-equity ratio clauses which are characteristic of Basel III compliant bank hybrids issued in Australia. As such, the new hybrids will qualify as AT1 capital. They will also qualify as having intermediate equity content according to Standard & Poor’s which is important for the company’s credit rating debt requirement.

ANZ said the hybrids are the part of a process to replace $2 billion worth of ANZ’s CPS 2 (ASX code: ANZPA) which are due for conversion in December. The bank is said to be looking to raise between USD$750 million and USD$1 billion with the proposed transaction, which is expected to be 550 bps over the benchmark rate. In addition, an AUD-denominated capital notes offer is to be considered before the end of September and the two capital raisings would presumably complete the replacement of the CPS 2.

31 May 2016

CBA’s newest hybrid has started trading in the last week and Westpac’s latest replacement for its soon-to-be-redeemed Westpac TPS units has had a trading margin set at 4.90% above the Bank Bill rate. Now NAB has announced that it too will be issuing a hybrid security, NAB Capital Notes 2 (ASX code: NABPD). These instruments will qualify as Additional Tier 1 (AT1) capital under the Basel III bank regulatory framework. With the prevailing level of interest rates, they will pay around 6.95% pa inclusive of franking credits.

The issue of NAB Capital Notes 2 seeks to raise $750 million, with the ability to raise more or less depending on demand. The indicative margin range is 495bps to 510 bps, which is broadly in line with Westpac’s indicative range of 490bps to 510bps. The margin on Westpac has been set at 490bps and so NAB’s indicative range may be seen as a deliberate attempt to offer subscribers at least an extra 5bps for the extra 6 months to maturity.

The first call date will be on 7 July 2022 and subject to APRA approval, NAB may elect to convert, redeem or resell NAB Capital Notes 2 at this time. If not called by 8 July 2024 the new notes will mandatorily convert in NAB shares.

Investment is all about relativities. If one invests in this latest offering, what other investment opportunities are foregone? The most relevant question is of where the new hybrid fits relative to current trading margins available to investors. Commonwealth Bank’s PERLS VIII were issued two months ago with a margin of 510bps but as the chart below indicates, any buyer in the secondary market will now get closer to 450bps.

For readers who are interested in the issue margins of other hybrids, there is a chart in a recently published article about Westpac’s Capital Notes 4 issue.

The issue is open to holders of Westpac’s various ASX-listed securities registered on or before 26 May 2016 and clients of the joint lead managers and co-managers to the issue. There is no direct public offer. Trading on the ASX is expected to commence on 8 July 2016.

26 May 2016

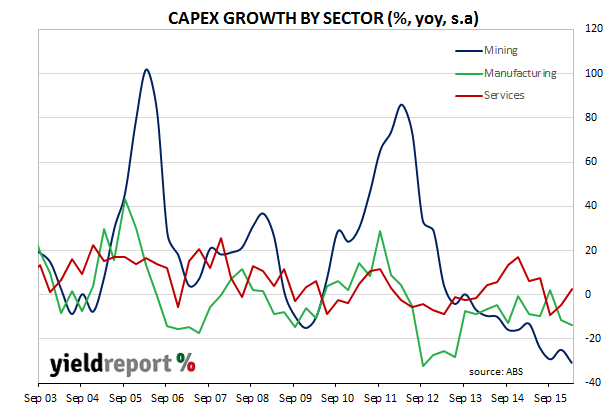

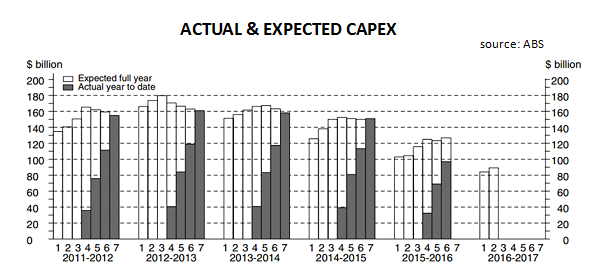

First quarter private capital expenditure figures have now been released by the ABS and the -5.2% quarter-on-quarter figure was worse than the 3.5% decline expected by economists. Year on year, capex was 15.4% lower, the result of business investment falling back after the mining investment spike of 2011/2012.

10 year bond yields initially fell before recovering slightly to finish the day 3bps lower at 2.245%.

The AUD similarly was sold off against the USD before finishing the day higher at 72.25 US cents, which indicates the currency market viewed the data in less negative light than the bond market. Generally the figures were greeted without enthusiasm, with ANZ describing the downgrading of non-mining firms’ investment intentions for 2016-17 result as “disappointing”. However the bank pointed out the survey “misses some key non-mining industries.”

Prior to the release Westpac had expected a pessimistic result but added policymakers, especially at the RBA, would be particularly interested in the investment intentions of the service sectors which are “a key element in the economy’s successful transition from growth led by mining investment to strength across the broader economy.”

Estimate 6 for 2015/16 capex plans is now $126.8 billion, 2.3% higher than February’s Estimate 5 of $124 billion but 15.3% lower on the previous year’s Estimate 6 of $149.8 billion. Estimate 2 for 2016/2017 is now $89.2 billion and 6.3% higher than Estimate 1 but also less than the corresponding estimate from one year ago.

25 May 2016

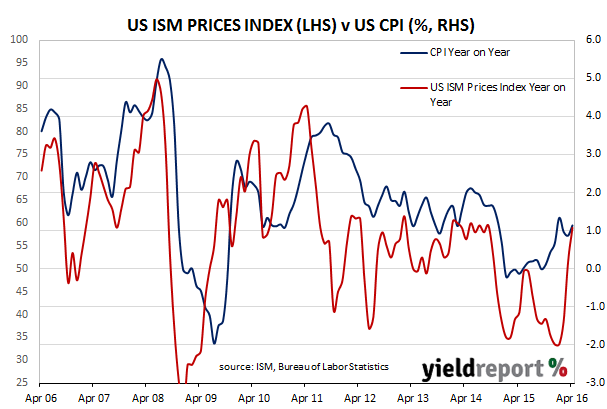

BlackRock is the world’s largest asset manager and operates in 30 countries. Its global chief investment officer, Richard Turnill, says US deflation is over and his thinking is, at least in part, based on the relationship between the Institute of Supply Management’s (ISM) Prices index and the US CPI.

Here’s a chart of the two since 2006:

Mr Turnill thinks recent rises in forward-looking surveys such as ISM’s Prices Index will feed through to higher CPI figures, especially as oil prices rise instead of fall in the absence of further shale oil production and factory gate prices are passed on to consumers. He also expects the USD to cease rising against other currencies, which will stop currency-related price falls of imports, while wage rises, which have been modest, are expected to continue to be so.

However, having said that, Mr Turnill still only expects “one to two rate increases this year amid slow U.S. growth.” Mr Turnill still believes the US Fed will be very cautious in raising official rates despite the presence of building inflationary pressures.

25 May 2016

T Rowe Price is a US fund manager based in Baltimore and founded in 1937. It operates fixed interest and equity funds in sixteen countries around the world. Its head of international fixed income, Arif Husain, was in Sydney this week speaking at a lunch briefing and he has made some observations which raised a few eyebrows.

The controversial part of his comments related to his views on Australia, and how it was in a similar economic situation to Germany’s ten years ago. “Australia is different right? I was in Germany five years ago, they said they were different. Now look at that, they are pretty much like Japan.” Many German bonds now trade at negative yields and Mr Husain thinks the same could happen here. “Australian investors have so far escaped the worst of the low yields in fixed income – I’ve seen clients in Europe doing some dumb stuff just to get back up to zero rates – but I would not be surprised to see negative yields hit this market at some point.”

24 May 2016

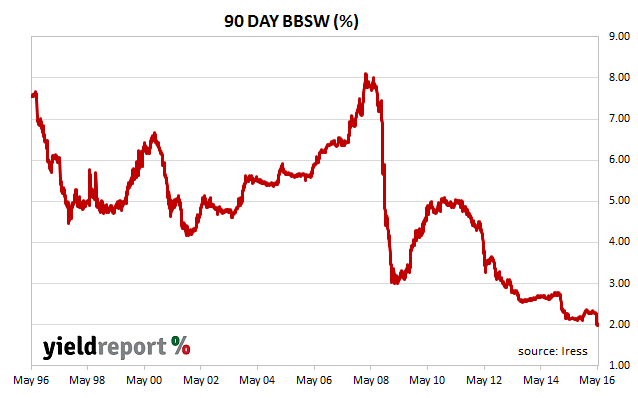

Westpac’s latest hybrid security offering has had its margin set after the completion of a book-build process. The margin on Westpac Capital Notes 4 will be 4.90% and, when added to the current 90 day bank bill swap rate (BBSW) of 2.00%, investors will receive 6.90% annually, inclusive of franking credits.

The distribution rate is set on the first business day of each payment period and therefore the total rate holders will receive for the period will depend on the BBSW rate on that first day. The margin is fixed at 4.90% but as BBSW varies from day to day, so too will the distribution rate of each payment period. There has been an exception made for the first payment period where the BBSW rate is taken from the issue date.

The book-build was closed early on what Westpac describes as “strong demand”. Westpac has increased the offer size to a total of approximately $1.45 billion but the final size will be dependent on how many Westpac TPS (ASX code: WCTPA) holders decide to roll over into the new hybrids and the level of applications made by other eligible security holders. Eligible security holders are those who have registered to receive a prospectus and a personalised application form.

19 May 2016

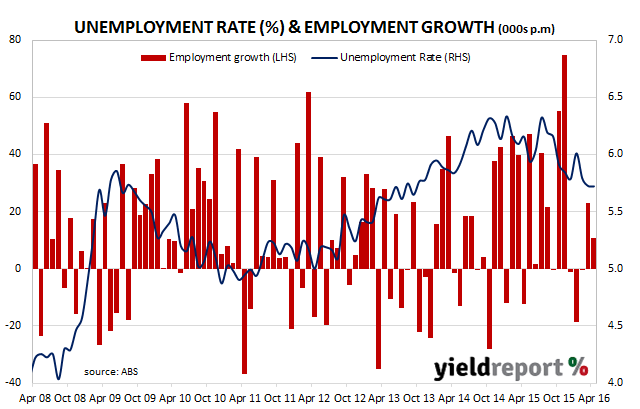

Australia’s job market has rebounded in April, creating 10,800 new jobs in net terms. The figures were not far from the expectation of 12,000 new jobs but the composition of the increase may not please everyone; part-time jobs increased by 20,200 while full time positions fell by 9,300. Another concerning figure is the fall in hours worked. Monthly hours worked in all jobs decreased 17.9 million hours to 1,613.8 million hours. The growth in employment and a fall in the participation rate from 64.9% to 64.8% kept the seasonally-adjusted unemployment rate steady at 5.7% instead of moving to 5.8% as economists had generally expected.

The numbers were greeted by markets in a fairly neutral manner. ANZ pointed out “momentum has slowed” and said it expected unemployment to remain near 5.7% for the rest of the year. CBA also noted the drop off in momentum, describing the jobs data as “soft, but not disastrous” and said this and a poor March GDP figure would add pressure on the RBA to cut rates in June. Australian 10 year bond yields rose 5bps to 2.30% while the AUD rose initially against the USD before settling back.

Here’s what the economists thought:

Shane Oliver, AMP Capital: “[It is] hard to get excited…soft beneath the surface.”

National Australia Bank senior economist Tapas Strickland: “It could also indicate under-utilised labour and could help explain why the recent falls in the unemployment rate are yet to translate through to a pick-up in wages growth.”

JP Morgan senior economist Ben Jarman: “There appears to be some dialling back of hours for existing workers too.”

Westpac senior economist Justin Smirk: “This highlights the big shift in employment growth from the previously booming resources sectors to the more modestly growing services sectors, as these sectors have a much higher proportion of female and part-time workers.”

18 May 2016

Usually minutes from a central bank are assessed for the nuances they contain. Is there an easing bias? Is there a focus on inflation or GDP growth? However, the release of the minutes from the April FOMC meeting contained a message plain for all to see. ANZ described them as having “a fairly dramatic impact on the market on their release” and Westpac said they were “far more hawkish than expected.” Commonwealth just referred to them as “blunt”.

The minutes said a June rate rise was “likely” if the second quarter data improved. “Most participants judged that if incoming data were consistent with economic growth picking up in the second quarter, labour market conditions continuing to strengthen and inflation making progress toward the committee’s 2% objective, then it likely would be appropriate for the committee to increase the target range for the federal funds rate in June.”

Ahead of the release, prices in US cash markets were implying a 19% chance of a June rise. After the minutes were made publicly available, the probability rose to 34% while the probability for a July increase rose from 38% to 51%. US bond rates went higher on the news. 2 year yields rose 7bps to 0.90% and the 10 year yield rose 9bps to 1.86%. The US dollar firmed against other currencies.

Locally, banks such as NAB said the UK June “Brexit” referendum may give the FOMC a reason to delay until July, noting one FOMC member had described the vote as “another variable in the mix”. ANZ’s view was “the negative feedback loop on monetary conditions, as we know, means the FOMC will proceed with great caution”, even though ANZ expects higher US rates this year.

Click here for the full April minutes.

18 May 2016

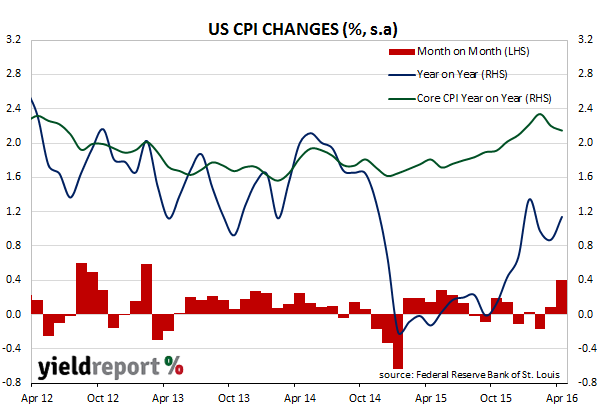

The headline inflation rate came in at 0.4%, a rise from the March figure of 0.1% and in line with the 0.4% rise expected. Energy prices were substantially responsible for the index’s rise, with petrol jumping 8.1% over the month. Clothes, vehicles and non-energy commodities fell. The year-to-date CPI figure rose to 1.1% from 0.9%, and it is now back above February’s comparable figure of 1.0%.

Core inflation, which was seen as a long-run measure of price increases across the economy, continued to edge down. The annual rate hit a short-term peak at 2.3% in February before slipping to 2.2% in March and then 2.1% in April. Core inflation strips out the more volatile food and energy components.

ANZ did not have much to say about the results other than to note “the core measure of inflation (which covers 80% of the CPI) has now been at 2% or higher for six months” while Westpac said, “US CPI, industrial production, capacity utilisation and house building all beat estimates.” NAB took a different tack and looked at the implications for the personal consumption expenditure figure (PCE). “On an annual basis, core CPI dipped to 2.1% from 2.2% in March and it would suggest there is downside risk to the core PCE deflator (the Fed preferred inflation measure) due for release on the last day in May. “

The CPI figures, along with statements from FOMC members Williams and Lockhart alluding to the next few meetings being ”live”, sent treasury yields higher. 2 year bond yields rose from 0.79% to 0.83% and 10 year bond yields rose from 1.75% to 1.77%.

17 May 2016

When CBA announced the redemption of its PERLS III (ASX code PCAPA) step-ups in late March, speculation arose as to Westpac’s intentions with regards to Trust Preferred Securities (TPS) step-up units. This was all but confirmed in early May when Westpac released its half year results and said its policy was to replaces non-Basel III compliant securities. Westpac has now confirmed it will be redeeming its non-Basel III compliant TPS units (ASX code: WCTPA) on the step-up date, which is 30 June 2016. The redemption amount is $100.00 and the final distribution of $0.5724 per TPS unit will be paid on the same day. The last day of trading in the units is 10 June, 2016 and holders will be able to access the reinvestment option offered by Westpac in regards to the Westpac Capital Notes IV offer just announced today.\

Related article: New Westpac hybrid to start at 6.90%