17 May 2016

The RBA’s May board meeting minutes have markets less confident of any further rate cuts this year. After the March CPI figures were followed by a 25bps cut, markets quickly factored in another rate move down to 1.50% and were placing a reasonably high probability on another cut down to 1.25%. However, economists pointed to the “Considerations” section and focussed on a sentence which is not always present: “members discussed the merits of adjusting policy at this meeting or awaiting further information before acting.” The general interpretation was the RBA’s decision to cut rates in May was not clear cut, which now casts doubt on any other rate moves before August when June quarter CPI figures are published.

However, it is worth recalling recent history in regards to a phrase in the April minutes. The words “with inflation close to target” was attached to some stock-standard words which had not changed from the previous month. The change was seen as being on the hawkish side. Look at what then happened; the RBA reduced the official cash rate.

In any case, the AUD jumped three-quarters of a US cent immediately after the release, a sign the currency market is factoring in higher-than-previously-expected rates. The bond market took a similar view and 3 year bonds moved up 4bps while 10 year bonds moved up 5bps.

Westpac’s Bill Evans was fairly neutral in his response saying, “It is difficult to see any significant additional insights in these minutes relative to the more comprehensive Statement on Monetary Policy.” NAB was similar with its take on release. “In any event, NAB’s view is that the Board will at least want to see the Q2 inflation data before deciding whether to cut again.” ANZ was more forthright in its view: “However, we believe the absence of an easing bias is normal practice immediately following a rate cut, and the size of the downgrade to the Bank’s inflation forecasts strongly suggests that further monetary policy easing is likely. We continue to expect further easing given the soft inflation outlook, and we are looking for another 25bp cut in the cash rate to 1.5% at the August meeting.”

Click here for the full version of the May minutes.

13 May 2016

Congratulations to John McNiven, Ian Martin and Richard Murphy, the founders of Australian Corporate Bond Company, who won the award for Best Disrupter at the Afiniation Network’s recent fintech event held at the Melbourne Grand Hyatt. ACBC created bond ETFs which retail investors can access, unlike the bonds which underlie the ETFs and typically trade in amounts of $500,000 or more.

11 May 2016

YieldReport has made several references in recent months to a trend in Australian bond markets by banks such as CBA, NAB, BoQ to raise funds by issuing FRNs instead of fixed rate bonds. Bank of Queensland’s (BoQ) latest fund raising exercise is consistent with this trend but it comes with a potential twist and their previous bond issues may provide a clue to current state of bond markets and demand/supply dynamics.

BoQ’s previous 5 year deal (excluding the tier 2 issue at the end of April) was back in late 2014 when it raised $550 million, comprising a floating rate component worth $125 million and a fixed component worth $425 million. An analysis of BoQ’s fund raising in recent years indicates issuing bonds via both a fixed and floating structure has been BOQ’s preference method.

The latest raising by BoQ was an issue of $650 million of 5 year FRNS at 3m BBSW + 148bps. There was no fixed component this time and YieldReport understands that this was canvassed amongst investors but ultimately withdrawn. There may a number of reasons why the fixed component was canned but in a world of (really) low interest rates, perhaps it is a case of borrowers being keen to lock in low long-term funding but lenders less so.

11 May 2016

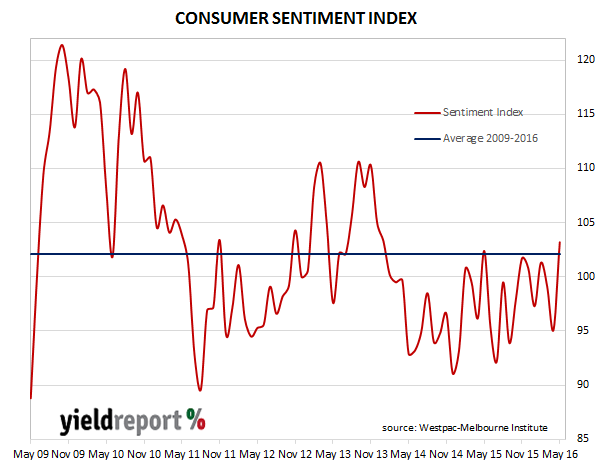

It seems as if the RBA magic wand has done the trick. The latest Westpac Melbourne Institute consumer sentiment survey shows a big kick upwards to 103.2 from April’s reading of 95.1. The higher reading indicates more consumers are optimistic than the number of consumers who are pessimistic.

All of the five components of the index rose in May. Westpac’s chief economist Bill Evans says his bank’s analysis suggest the recent rate cut was the “dominant driver” and such a rise has been common in the past after other rate reductions. However, even after the turnaround in consumer optimism, Westpac still expects the RBA to reduce rates by another 25bps to 1.50% in August.

11 May 2016

“I’d like to borrow $7 billion, please.” Try saying that to your bank manager. Yet, without any great fanfare, the AOFM, the Commonwealth Government’s finance arm, has done the equivalent by issuing $7 billion worth of May 2028 bonds via a syndication deal this week. It’s the largest bond offering by the AOFM since it offloaded $7 billion worth of April 2037s in October 2014 and prior to that sale, $7 billion worth of April 2026s in March 2014.

It gets better, too. The coupon rate of interest on the bonds is a miserly 2.25%, although the final yield to maturity is slightly higher at 2.525%. 70% of the bonds were taken up by domestic buyers. Fund Managers, both domestic and foreign, took about 30%, while banks’ trading desks took another 30%. YieldReport has commented on several occasions on what appears to be a trend towards greater issuance of FRNs in the corporate sector and speculated on the reasons for it. In any case, pressure on issuers to offer FRNs does not appear to have reached the ACGB sector.

10 May 2016

The sale of index linked bonds is are not a particularly common form of fund raising for the Commonwealth Government but on the other hand they do come along usually at least once a month. Inflation-linked bonds issued by the Australian Office of Financial Management are securities where the capital value of the bond is adjusted for movements in the Consumer Price Index. Index linked bonds therefore offer investors a “real” yield, or a return adjusted for inflation. Normally such bond tenders pass without much comment; the amounts offered are small, typically $150 million, and much smaller than $700-$900 million vanilla bond tenders held each week.

Sometimes, though, something about the tender stands out. For instance, in September last year, the AOFM sold November 2018 index linked bonds at a negative yield meaning that the buyers were locking in a return below the rate of inflation. Such behaviour may occur when people think this is the best outcome in a world where the alternatives are worse and therefore a negative yield indicates a level of anxiety about economic conditions at the time.

The unusual thing about this week’s latest indexed bond tender is the fact it was swallowed up wholly by one bidder. There were 42 bidders, lodging bids worth a collective $542 million and their bids ranged from a real yield of 1.175% to that of the successful bidder, a real yield of 1.005%. These inflation-linked bond tenders typically attract a good level of interest and coverage ratios are typically on the higher side. Buyers of index linked bonds tend to be life offices and insurance companies with matching liabilities.

09 May 2016

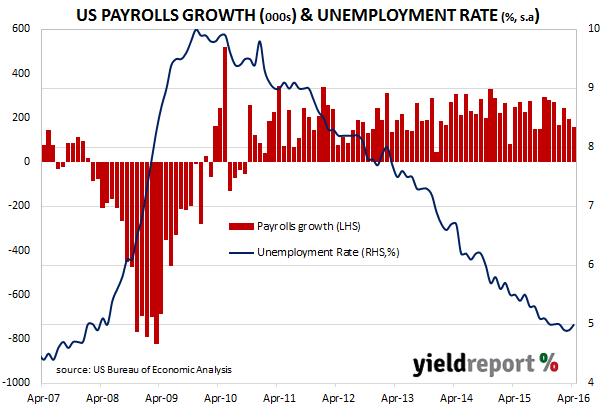

Unemployment in the US remained unchanged at 5.00% as the US created another 160k jobs in April. The number of jobs was less than the 12 month average (232k) and less than the 200k expected by the economists surveyed by Reuter’s just prior to the release. Revisions were also made to February and March figures, the net effect being slightly lower than the original figures.

WBC said they latest figures plus other recent US data “suggests a slow start to Q2 for the US economy.” ANZ was a little more positive and said, “While the NFP report had something for everyone, it does confirm the ongoing improvement and absorption of slack in the US labour market.

One bit of information which was taken as a positive was rise in the average hourly earnings which unexpectedly rose to 2.5% (yoy), up from March’s figure of 2.3%. US interest rates rose modestly on the day. 2 year bond yields rose 1bp to 0.73% and 10 year bond yields finished the day at 1.78%, up 3bps.

09 May 2016

Australia’s major banks are known for their bond issues which are typically on the large side; only last week NAB issued $3.2 billion worth of fixed and floating rate bonds in two tranches. While such bond issues may be somewhat routine, they are still worthy of note given banks are at the heart of the financial web and their actions and bond pricing can provide a good insight into current global market trends.

Westpac’s latest 5 tranche issue certainly fits the bill. It continues the recent preference for USD transactions from corporates such as Amcor, Sydney Airport and BlueScope but of course it is substantially larger, totalling USD$4 billion (AUD$5.5 billion). The majority of the funds raised were via fixed-rate bonds with tenors of 3, 5 and 10 years, while only USD$500 million was raised in the two floating rate tranches.

09 May 2016

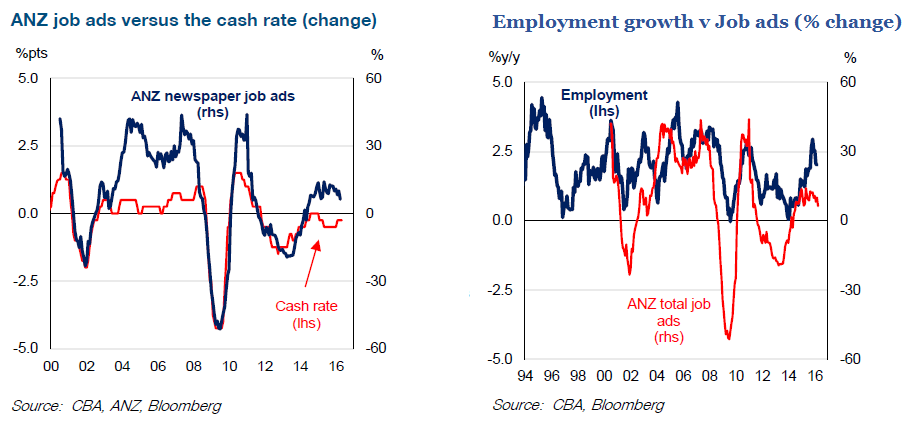

Financial markets are usually very interested in job ads surveys, especially those surveys which bear a good relationship over time to the official jobs numbers or indeed the RBA’s cash rate (see below).

ANZ’s most recent monthly job ads survey was released this week and it showed total ads down 0.8% (seasonally adjusted) in April but up 6.3% over the year. The comparable March figures were +0.1% and +10.0% respectively. Internet ads were down 1.6% for the month (+8.7% for the year) while newspaper ads rose 6.9% (-10.7% for the year). Advertising through newspapers now represents less than 2% of total ads and is now close to irrelevant from a sampling point of view.

Commonwealth Bank viewed the latest figures as a sign “momentum is waning” but it also notes how ANZ’s survey is in contrast to employment components of NAB’s business survey. The mention of the contrast suggests Commonwealth is wary of taking too firm a view without further evidence.

ANZ also noted how job ads had been “broadly flat” for the last six months, something which may have come from a softer domestic economy but as their chief of Australian Economics, Felicity Emmett said, ”[it] follows a period of substantial growth in employment, so some modest slowdown should probably not be surprising.”

06 May 2016

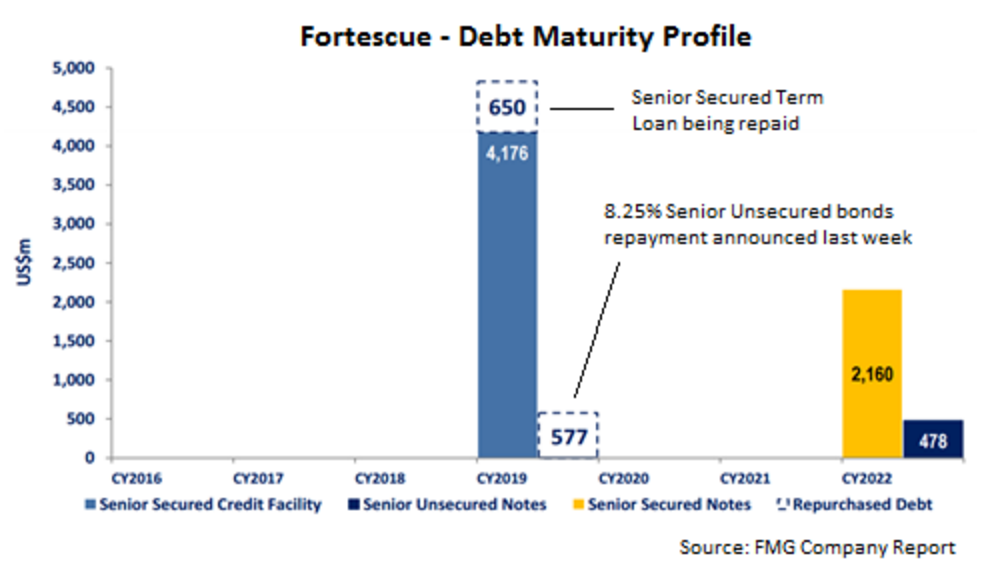

Companies and governments are said to tap a market when they sell more of an existing series of bonds. Fortescue has been busy doing the opposite; it has been buying back the debt it issued in the past, prior to its maturity date.

The latest debt reduction came in the form of voluntary redemption notice for all USD$577 million of its 8.25% 2019 bonds. The bonds will be repurchased at a price of 102.0625% of face value, which include a premium for early redemption premium equal to half of 4.125% coupon. A couple of days later Fortescue announced it was repaying an additional USD$650 million from it senior secured credit facility which will reduce the balance to a little over USD$4 billion.

This is not the first time for Fortescue. So far it has reduced its debt load by around USD$2.3 billion during the current financial year, via several bond buybacks and its moves may be provoking other corporates to do the same thing. Rio is in the middle of a $1.5 billion bond tender and GE Australia has just announced something similar.