06 May 2016

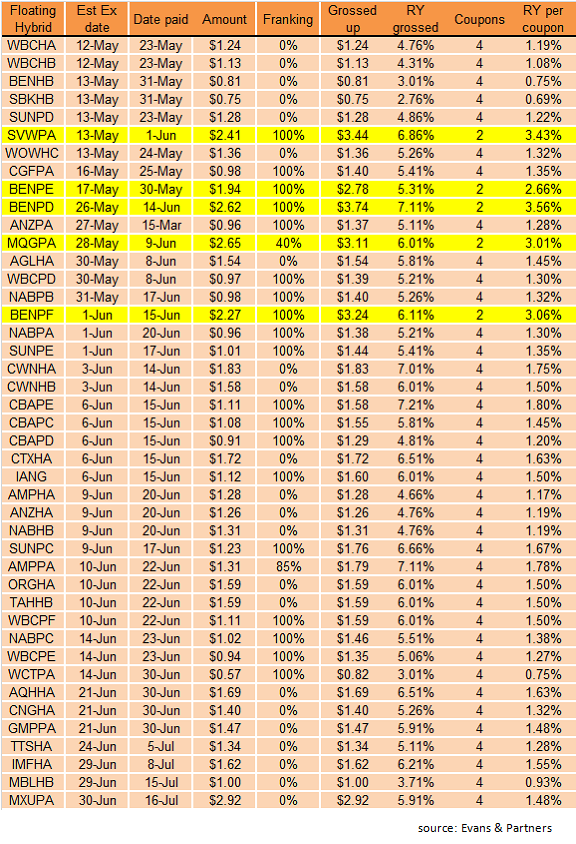

One of the consequences from the RBA’s decision last week to reduce official rates by 25bps is the corresponding fall in the BBSW rates by a similar amount. 3 month BBSW was roughly 2.28% before the March CPI figures were released, 2.14% before the RBA cut the official cash rate to 1.75% and by the end of the week this benchmark rate had come down to 2.04%.

This of course has consequences for the interest/dividend payments on ASX listed hybrids and notes which use BBSW rates as part of their rate-setting formulae. Michael Saba from Evans and Partners suggests that investors look at securities which have already set payment terms in advance of the latest RBA decision and especially those which reset the rate every six months. These securities will have their interest accrual locked in until the next six monthly rate reset. These are highlighted in yellow in the table below.

06 May 2016

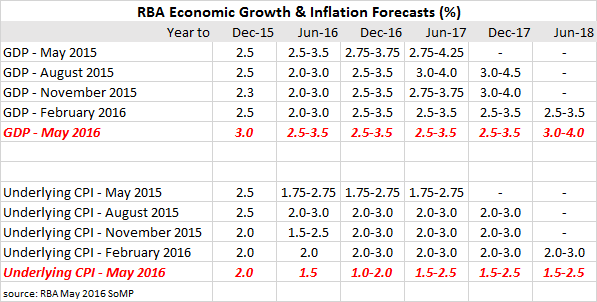

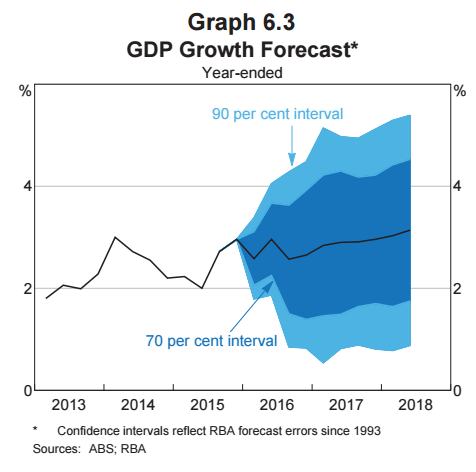

The RBA has reversed course with regards to it GDP forecasts in the latest quarterly Statement on Monetary Policy. It looks as if stronger-than-expected December quarter GDP figures (which were released in March) has led the RBA to increase its forecasts for GDP growth rate for the year to June 2016. Its forecast range has been increased by 0.5%, as has the comparable 2018 figure, although June 2017 remains unchanged.

On unemployment: the RBA expected average economic growth to be a little lower compared to 2015 and employment growth is expected to ease off from the rates seen in 2015. The RBA said low wage growth is supporting employment growth and notes this to be true “across a number of advanced economies.”

Domestic (non-tradables) inflation and low wage inflation over 2015 has led the RBA to reduce 2016 inflation forecasts to 1% – 2%. The RBA appears to have been surprised as much as anyone by the negative March quarter CPI and the average underlying CPI. This latest SoMP specifically refers to underlying inflation and the “broad-based nature” of weak domestic inflation and lower-than-expected wage inflation in 2015 as being responsible for the change in its forecasts.

Westpac Economics said, “If this true for core inflation forecasts then [the] RBA is very downbeat on domestic inflation.” Ex ANZ chief economist Warren Hogan said the RBA’s “optimism suggests next rate cut a few months away at least. The next big move in rates to 1% will come if/when growth falters.”

AMP Capital’s Shane Oliver said, “Expect more rate cuts.”

06 May 2016

YieldReport has referred to the preference of corporates to issue FRNs in several articles recently, the most recent being an issue by Bendigo & Adelaide Bank. Now National Australia Bank has announced it will be issuing a new benchmark 5 year FRN. The last time it issued a bond of this type was in late October when it sold $2.1 billion worth at 3m BBSW + 108bps. This time around it has given guidance in the 3m BBSW + 118bps region which, coincidentally, is the same price at which ANZ issued its 5 year benchmark FRNs in early April.

There has been a plethora of 5 year FRNs issued in the last month. Just over a week ago, Citigroup issued $600 million at 3m BBSW + 155bps, towards the middle of April Bendigo issued $650 million worth at 3m BBSW + 146bps, in early April Suncorp issued $600 million at 3m BBSW + 138bps and then there was the ANZ one referred to previously.

If the guidance is any good, and it should be given this is a “self-led” deal, the 118bps margin indicates things have got a bit more expensive for the banks since NAB‘s last 5 year FRN sale. Back in October 2015, it issued $2.1 billion worth at BBSW +108bps. 0.1% may not sound like much but for every $1 billion that’s $1 million in extra interest per year.

04 May 2016

Lend Lease is said to be about to hold a series of meeting with debt investors in Singapore, Hong Kong and London, commencing this week. The property developer updated bond investors in Singapore in the first week of March and normally some sort of transaction would have been announced shortly thereafter, but two months have passed without anything happening. Perhaps the expansion of investor meetings to Hong Kong and London will do the trick. Lend Lease is rated BBB- by S&P and Baa3 by Moody’s.

04 May 2016

Life has been difficult for Woolworths in recent years; its main competitor, Coles, has got its act together and is proving to be a worthy competitor; Aldi is chipping away with plain-packaged groceries; management has been distracted by the Masters hardware debacle.

The ratings agencies are also having a crack. Woolworths has an investment-grade credit rating but it is now only two rungs above a sub-investment grade rating. To be rated “investment grade”, a company must have a credit rating above BB+ from Standard & Poor’s or above Ba1 from Moody’s. Woolworth’s senior debt is now rated BBB (S&P)/Baa2 (Moody’s) after having suffered the latest downgrade from S&P. Previously its rating was BBB+. Moody’s downgraded Woolworths at the beginning of March in a similar fashion, reducing Woolworth’s rating from Baa1.

According to S&P, continued market share losses in Woolworth’s core supermarket business, declining Big W revenue and an expectation Woolworths will lower prices and spend more on service levels have led to the lower credit rating. The one bright note is S&P’s attachment of a “stable outlook” to this latest credit rating, which indicates the agency does not think another downgrade will be warranted any time soon.

Credit ratings are important as investors use them in assessing the trade-off between risk and return on a range of securities, especially bonds and other debt instruments. As a general rule, a lower credit rating will lead to a higher interest rate payable on a company’s debt. This latest decision by S&P will likely lead to a higher interest bill for Woolworths.

03 May 2016

A negative March quarter Consumer price index print of -0.2% (vs exp +0.2%) has led to the Reserve Bank cutting the cash rate by 25bps to 1.75% at its board meeting today. The rate is a historic low in Australia and demonstrates the RBA is concerned about deflation and its effect on jobs.

GDP growth has been reasonably strong and the recent unemployment rate moved down to 5.7% but inflation is the key to the RBA’s move. The average of the underlying inflation measures came in at 1.55%, well below the RBA’s target band of 2.00% to 3.00% and it analysts calculated it would take three consecutive quarters of 0.7% inflation to get the inflation rate back to the bottom of the band.

The RBA meeting statement said recent inflation data was “unexpectedly low” but with subdued growth in labour costs and low cost pressures elsewhere in the world, a lower inflation outlook than previously forecast is likely.

The RBA has a mandate to maximise employment growth and maintain price stability so the rate move, it is hoped, will increase economic activity and jobs without increasing inflation. The impact of cutting rates when they are already at historic lows will be debated though with some describing such as move as ‘pushing on a string’.

Worries about housing were addressed by the RBA that said “supervisory measures are strengthening lending standards……potential risks of lower rates in this area are less than they were a year ago.”

The Australian dollar lost over 1.5% immediately after the announcement to 75.70 US cents and markets also priced the chance of a further rate cut to 1.50% by August as a 50% chance. Equity markets soared higher on the news. Five hours after the rate cut announcement, the Federal Government is due to hand down its 2016/2017 budget that is also seen as the precursor to a federal election announcement later in the week.

Who said interest rate markets were dull?

02 May 2016

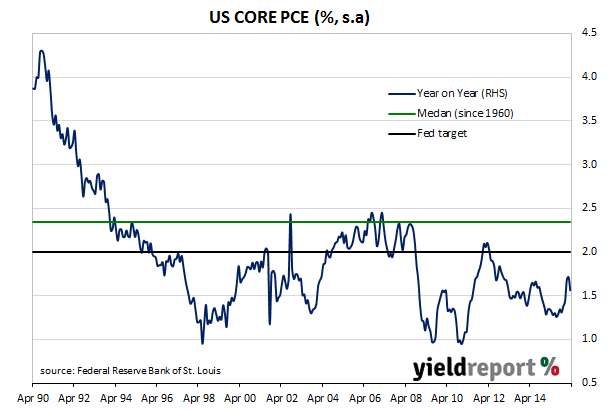

Growth in core personal consumption expenditure (PCE), which strips out energy and food components, is the US Fed’s preferred measure of inflation and the latest release had core PCE at 1.6% for the last 12 months and 0.1% higher than a month ago. In both case, the numbers were as expected and local banks had very little to say about them except for NAB which said the figures did not add “a whole lot to what we learned from Q1 (GDP) data.”

Last month CBA said February PCE figures would lessen the FOMC’s inclination to raise US official rates in a hurry. This latest batch of figures for March is unlikely to change that view. US ten year bonds finished the day 1bp higher at 1.83%.

02 May 2016

Peet, the 120 year old ASX-listed land developer, has just announced the launch of Peet Bonds, a new series of unsecured debt securities. They will be the second series of bonds to be issued under the Commonwealth Government’s 2014 simple corporate bond legislation, the first being Australian Unity’s 2020 bonds which were issued in November/December last year.

Peet plans to raise $75 million from the bond issue, $50 million of which will be used to pay for its convertible notes maturing on 16 June 2016 (but below the conversion price level). The new issue is a straight bond issue and will have a maturity date on 7 June 2021 with an annual coupon to be determined by an institutional book build process. The indicative interest rate will be around 7.50% pa and the bonds will be tradeable on the ASX.

Peet does not have a credit rating and the indicative rate puts it in a similar yield range to other recent debt issues by other unrated corporates. Recently, BB/Ba2-rated BlueScope issued bonds with a 2018 call date at 6.50% and unrated Capitol Health issued 4 year bonds at 8.50%. The fact that Peet has been in business for over a century and has a proven ability to ride out cyclical property downturns is a factor likely to be taken into account by investors.

The upcoming maturity of the convertible notes and the planned issue of bonds comes at a fortuitous time for Peet. Benchmark interest rates are at 60 year lows, allowing Peet to issue bonds at a yield considerably lower than at any other previous time.

The offer is not open to the general public and the bonds are only available to existing convertible noteholders, shareholders, clients of the underwriters and employees. NAB is the underwriting broker but other stockbroking firms dealing in bonds such as Bell Potter, Evans and Partners, Shaw and Partners and RBS Morgans, to name a few, may be able to arrange an allocation.

The closing date for the issue is 27 May, 2016 and the bonds will commence trading on the ASX on 8 June 2016.

02 May 2016

Westpac Trust Preferred Securities units look set to be redeemed in June at their interest step-up date. In Westpac’s latest half-yearly report, the bank stated its policy was to replace instruments which are not Basel III compliant. Westpac’s TPS will lose their Additional Tier 1 (AT1) status from 30 June, which coincidentally is the step-up date for the TPS units, so a new AT1 issue is likely to be announced shortly.

Step-up securities were issued with an incentive for banks to redeem them or pay additional interest to holders. When securities such as these lose their regulatory capital status, they become expensive for the bank to maintain hence the redemption and issue of new regulatory compliant securities.

There are roughly $750 million of TPS units on issue and thus we can expect at least this amount of new securities to be issued. Westpac’s last AT1 issue in July 2015 was in the form of Westpac Capital Notes III (ASX code: WBCPF), were issued with a margin of 400bps over BBSW, a mandatory exchange date in March 2023 and a call date in 2021. Trading margins are higher now, so a new hybrid from Westpac would be in the 475bps range if margins stay roughly at current levels.