02 May 2016

With the March quarter headline inflation rate of -0.2% shocking markets and leading to the RBA cutting the official cash rate, investors will be watching carefully for signs that inflation is not continuing to fall. The official ABS statistics are released quarterly and so the monthly Inflation Gauge released by the Melbourne Institute will be heavily scrutinised to determine future interest rate direction.

The latest data for April shows that consumer prices edged up just 0.1% as fruit and vegetables, fuel and medical services, rose between 3% and 4%, offsetting the 4% fall in travel and accommodation prices. 12 month inflation (blue line below) fell for a third month in a row, from 1.7% to 1.5%.

Falling fuel prices have been responsible for low headline inflation rates until recently. However, given global oil prices have rebounded since reaching a low of USD$28 in February, continued low headline inflation figures are the result of other factors.

According to the Melbourne Institute’s Dr. Sam Tsiaplias, “The March quarter ABS CPI was driven by significant falls in the fuel price, particularly in February. The Monthly Inflation Gauge also fell by 0.2 per cent in February. April’s data, which showed an increase in both the headline and trimmed mean measures, provides an initial indication that prices will increase in the second quarter.”

02 May 2016

Australian businesses are still enjoying buoyant trading conditions even though business conditions and confidence levels have slipped back in April, according to NAB’s latest Monthly Business Survey. Its Business Conditions Index fell 3 points from 12 to 9, while the Business Confidence Index fell 1 point from 6 to 5.

NAB’s interpretation of the figures was one of a confirmation of “a continuation of the favourable business environment that has helped to underpin the non-mining recovery”, a view Westpac senior economist Andrew Hanlon shared. He said, “This confirms that the non-mining sectors are benefitted (sic) from low interest rates and a sharply lower currency…Solid business conditions are now evident in manufacturing and transport/utilities.”

Domestic bond markets reacted to the report by sending interest rates slightly higher on the day. Implied yields on 3 year bonds edged higher by 1bp to 1.81% while the 10 year bond futures yield increased by 3bps to 2.55%.

29 April 2016

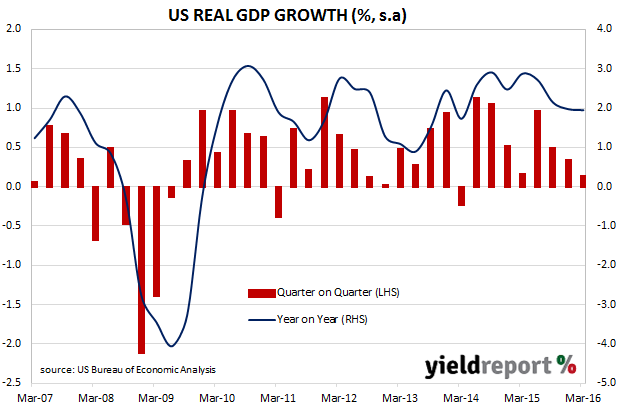

The US Commerce Department released Q1 “advanced” estimates of US GDP, which is the first of four estimates and subject to three more revisions over the next two months. They showed an annualised growth rate of 0.5%, lower than the consensus estimate of 0.7% and lower than the Q4 2016 figure of 1.4%. The yields of US 2 year Treasury notes reacted by moving down 2bps to 0.79% while US 10 year bond yields edged down 1bp to 1.82%.

According to Commerce Department annualised data, consumers and government expenditures grew while net exports and investment shrank. Personal consumption expenditure (PCE) was up 1.9%, government expenditure was up 1.2%, investment was down 1.9%, exports were down 2.6% and imports up 0.2%.

The Commerce Department calculates the annualised figure by compounding the quarterly result and so a direct comparison with UK or Australian figures is not meaningful. However, if the US GDP growth figures were to be calculated in same way as Australia (that is, q/q and y/y), then the quarterly US GDP figure would be 0.1% s.a. (previously 0.3% s.a.) and the year-on-year figure would be 1.9% s.a. (previously 2.0% s.a.).

Local banks were generally positive in their interpretations of the figures. Westpac noted how investment was the biggest drag on the growth figures but noted inventory reduction had occurred for three successive quarters in a row and were unlikely to continue. NAB was quick to point to the stronger-than-expected core PCE figures which are known to be watched closely by the US Fed while ANZ pointed to the weekly jobless data which they think “suggest[s] the labour market remains firm.”

ANZ summed up the banks’ attitude with the following comment. ”While the data certainly sends a clear signal that the US economy is in the midst of a soft patch, it arguably adds little to the FOMC’s assessment yesterday that the economy has slowed.”

28 April 2016

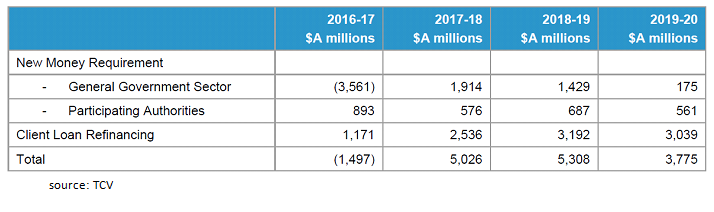

The release of the latest Victorian budget indicates another surplus, this time for $2.9 billion over the 2016/2017 year. It has now also released its expected funding requirements over the forward estimates period (see below table). The Victorian Government, as with its NSW counterpart, is currently in the enviable position of being able to repay debt, and it officially plans to reduce government and state enterprise (“Participating Authorities”) debt by $1.5 billion over 2016/2017.

Whenever governments run surpluses for sustained periods, bond markets can reach the point where future availability can become an issue, such as in the early 2000s with regards to Commonwealth bonds. Despite having run surpluses for the last two decades and the Victorian budget forecasting surpluses for the next four years, TCV’s statement indicates a total of $14 billion will still be required from 2017/18 through to 2019/20.

Maturing bonds account for $8.5 billion, while the funding requirement of the government sector and state-owned enterprises account for the rest. The discrepancy between the total of the surpluses and the funding requirement comes down to definitions used in the budget papers; budget items are typically “operational” and do not include all cash flows in and out of government coffers.

28 April 2016

QPH Finance, the financing arm of the Port of Brisbane, has mandated a couple of local banks to arrange a series of meetings with debt investors. Invariably a bond issue follows a week or two later, although in the Province of Quebec’s case the issue of bonds did not occur for over six weeks.

QPH last issued bonds in June 2014 with the issue of $200 million worth of July 2021s at Swap + 145bps into the domestic market and $USD750 million of 2029s into the US private placement market. QPH is rated BBB by Standard & Poor’s.

28 April 2016

Falling global oil prices have seen the largest US oil producer, Exxon Mobil, lose its coveted AAA credit rating – a rating it has held since 1930. Standard & Poor’s now rates the company AA+, the same level as the US government.

The rating cut is not that much of a surprise as S&P had placed the company on notice in February but the company had been working hard behind the scenes to maintain the lofty rating. Only two companies in the world are left with a AAA rating – Microsoft and Johnson & Johnson.

In 1980, there were more than 60 US companies with AAA ratings. That number declined to six in 2008. General Electric, Pfizer, ADP and now Exxon Mobil have since fallen out of that illustrious group.

28 April 2016

The US Fed held its regular monthly meeting this week and once again the world’s interest rate markets held their collective breath to see what chair Janet Yellen would do. As expected though, the Fed left its benchmark interest rates unchanged. It did note that growth in economic activity appears to have softened but labour market conditions in the US had improved.

The Fed is keen to move interest rates away from between 0.25% and 0.50% and the market is betting on the June meeting for a change to occur. The Fed moved rates from close to 0.00% at its December 2015 meeting after holding them steady since 2008. It has previously commented on volatility in global markets as one reason why rates have not risen more quickly. It is also said to be concerned that Japan and Europe are stimulating markets to the tune of billions of dollars each month and that a rate rise by the US could see the US dollar soar to economy-stifling levels.

A vote of the UK’s exit from the European Union could also create significant volatility and the Fed are known to be keen not to get caught shifting rates against such a backdrop. A vote on the ‘Brexit’ is scheduled for 23 June.

Overall the Fed is looking at a more gradual series of rate increases than has been the case in past tightening cycles and as usual it will be data dependent.

28 April 2016

The US bond market is the flavour of the month with Australian corporate debt issuers. First it was GPT group with a two tranche USD$100 bond deal with 2027 and 2028 maturities. Then, came along Suncorp with a USD$500 million issue of 2019 bonds. Now it is BlueScope’s turn to tap the US bond market after receiving a credit rating upgrade from Moody’s earlier this month.

Initially, BlueScope advised the ASX it would be offering $300 million of senior unsecured notes with a 2021 maturity date and a 2018 call date. The steel maker, perhaps best known for its Colorbond range of products, has since advised it is now looking at raising USD$500 million at a yield to maturity of around 6.50% to 6.75%. US 2 year Treasury notes are currently yielding just above 0.80%, so a yield at the lower end of the indicative range would be at nearly a 6% margin, a reflection of BlueScope’s sub-investment BB credit rating.

The funds raised would be used to repay an existing bridging facility. Part of the rationale behind BlueScope’s decision is to diversify its funding sources and extending it maturity profile. It is this repayment of bank debt and replacement with corporate bonds which seems to becoming a theme in Australia in recent times. With yields at historically low levels and banks highly focused on creditworthiness, corporates are finding debt markets are allowing them to reduce the reliance on bank funding.

Other corporates such as Capitol Health have hinted as such in their announcements and it may be a pre-cursor of things to come. With the major banks set to report earnings in the next few weeks a large focus will be on the prospect rising default rates.

27 April 2016

March quarter CPI figures were released today showing a headline quarterly rate of inflation of -0.2% (seasonally adjusted) or 1.3% for the year to the end of March. This surprised markets which were expecting 0.2% for the headline rate and an annual inflation rate of 1.6% and it is the first negative headline CPI figure since December 2008. Some analysts have described the result as a game changer that will lead to a rate cut when the RBA meets on 3 May. JP Morgan’s Sally Auld said the RBA had ”no choice” but to cut rates next Tuesday.

Markets reacted swiftly. Cash markets, which had become accustomed to some chance of a rate cut this year, quickly switched to fully pricing in one rate cut by August and a 50% chance of a cut on 3 May. 10 year bond yields fell 12bps in afternoon trading and the Australian dollar fell 1.3 US cents as markets factored in lower rates than anticipated just a few hours earlier. Investment banks such as Goldman Sachs, JP Morgan and Macquarie now believe the CPI data should force the RBA to act on its easing bias and reduce rates at its next meeting.

*average of trimmed mean & weighted median CPI measures

Here’s a round-up of the views from leading economists:

JP Morgan’s Sally Auld: The RBA has “no choice” but to cut rates on Tuesday.

AMP Capital’s Shane Oliver: “Ultra weak inflation significantly ups the pressure on the RBA to cut rates again. I still see another easing ahead.”

UBS’s Scott Haslem: “Given 3% GDP growth and 5.7% unemployment, we doubt a short period of sub-target core CPI is a sufficient condition alone for the RBA to trim.”

Justin Fabo, former ANZ senior economist: A “difficult one for the RBA given the activity data have looked ok.”

Citi’s Josh Williamson: “So far the signs on the economy would suggest that another cut isn’t needed, particularly with unemployment at 5.7 per cent and the economy growing at around trend.”

Westpac’s Justin Smirk: “Low inflation, on its own, is not a trigger for a rate cut…A rate cut is dependent on local economic conditions demanding a rate cut. With unemployment on a new downtrend this is not so at the moment and we suggest that the RBA is waiting to see a new weaker trend in domestic activity and employment before it would embark on such a strategy.”

27 April 2016

Victorian state government coffers are predicted to grow sharply on the back of revenue growth from payroll tax, stamp duty and higher GST grants. The budget numbers are due to be handed down on 28 April and projected to deliver $9.2 billion of surpluses over the next 4 years. While one should be cautious over government projections on budget surpluses (who can forget Wayne Swan’s “four budget surpluses that I deliver tonight” speech), the numbers bode well for investors in Victorian state government bonds. A stronger balance sheet usually means less default risk and narrower spreads to Federal Government bonds.