15 April 2016

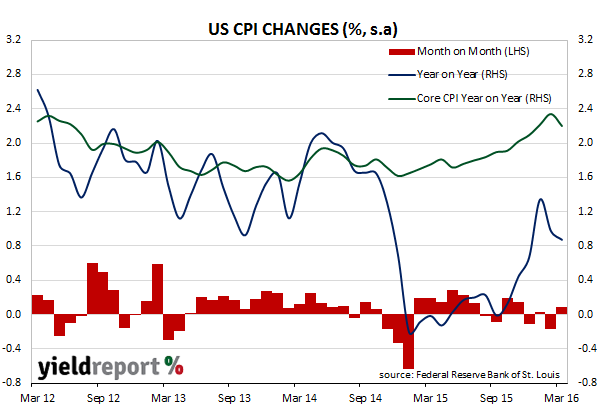

Unlike the release of US CPI figures for February, the latest CPI figures were not clouded by being released right next to a Fed FOMC meeting and so a bit more attention should be paid to them this month. The headline inflation rate came in at 0.1%, a rise from February’s -0.2%, but less than the 0.2% rise expected. Petrol prices were responsible for much of the index’s rise but they were largely offset by falls in the price of clothing. The year-to-date CPI figure fell to +0.9%, which is down from February’s comparable figure of 1.0%.

Westpac pointed to Janet Yellen’s recent comments regarding the first quarter jump in inflation as being “transitory” and how the latest CPI figures added weight to her argument. ANZ took the opposite view and said the numbers “did little to support” her view. Got to love economists!

February figures contained surprisingly strong core inflation numbers but comparable figures for March indicated the first drop in core CPI after a run of nine months of increases. Core inflation, which strips out the more volatile food and energy components, rose 0.1% for the month and 2.0% over the last 12 months, down from February’s figure of 2.3%.

The CPI figures, plus lower than expected jobless claims, sent treasury yields higher. 2 year bonds went from 0.75% to 0.77% and 10 year bonds rose from 1.76% to 1.80%.

14 April 2016

Bendigo & Adelaide Bank has joined the floating rate debt trend that has become evident in recent months. The Bank has raised $650 million at BBSW + 146bps, in line with the 145-148 bps guidance investors were given prior to the sale but way in excess of the BBSW + 110bps payable on bonds issued in a similar transaction in mid-August of last year. Margins over BBSW have gone up since October 2015 when Commonwealth Bank paid BBSW + 78bps for a 3y FRN. Recently CBA paid BBSW + 98bps, which is a 20 bps spread blowout but Bendigo’s latest bond sale represents a 36bp blowout. Debt pricing would appear to be getting tougher for banks which is likely to lead to higher non-bank debt pricing.

CBA’s $2billion worth of FRNs at BBSW + 98bps this week followed Suncorp-Metway’s 3 year FRN as part of a two tranche deal which raised $750 million ($600 million fixed, $150 million floating). In the last week of March NAB issued $2 billion worth of FRNs.

14 April 2016

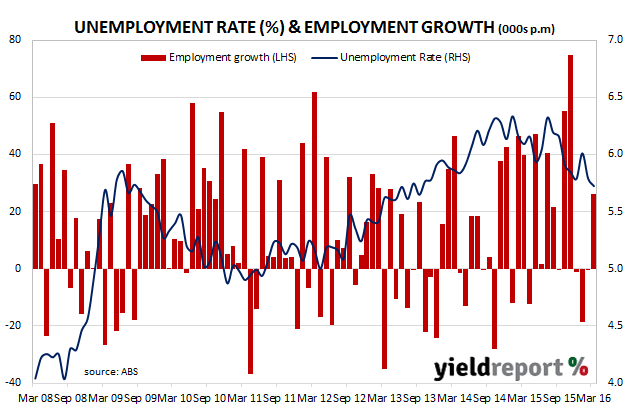

Australia created 26,100 jobs in March, reversing 3 months of poor or disappointing jobs growth. Australia’s unemployment rate dropped from 5.8% to 5.7%, beating economists’ expectation of a rise to 5.9% on expectations of a higher participation rate (which in fact remained steady at 64.9%). However, all the growth came from part-time jobs, which increased by 34,900 to 372,900 while full-time employment fell by 8,800 to 8,180,400. As a result, monthly hours worked in all jobs decreased 17.5 million hours to 1,632.3 million hours.

The numbers caused 10 year bond yields to rise by around 4bps-5bps and prices in the cash market moved to imply a lower level of confidence in the likelihood of rate cuts in 2016. The chance of a rate cut by August this year is now back to 70% and the month in which one rate cut has been fully factored in has been pushed out to December.

NAB said, “It’s clear the labour market has improved over the past year” while Justin Fabo from ANZ described the jobs figures as “strong”, saying there was no chance of a RBA rate reduction in the near term. Nomura no longer expects a rate cut in May and has pushed its rate cut call back to November.

13 April 2016

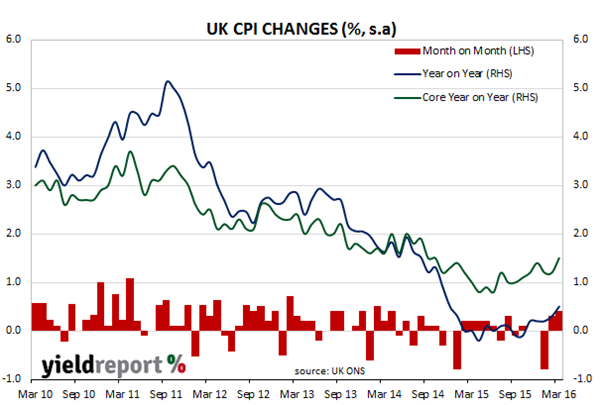

UK inflation in March has surprised market pundits by rising at a greater rate than expected. The UK’s Consumer Prices Index (CPI) rose by 0.2% during March, or 0.5% for the last 12 months. The annual figure was expected to be 0.4% but the higher number was driven by rises in clothing and airfares which ANZ pointed out had been distorted by this year’s early Easter. The rise in consumer inflation was tempered by falls in food prices, while petrol prices rose less than in February.

The UK’s Office of National Statistics noted how the rate has increased since October 2015 but pointed out it was “still relatively low in the historical context.” Core consumer inflation figures, which strip out alcohol, tobacco, energy and food price changes, rose by 1.5% over the last 12 months.

13 April 2016

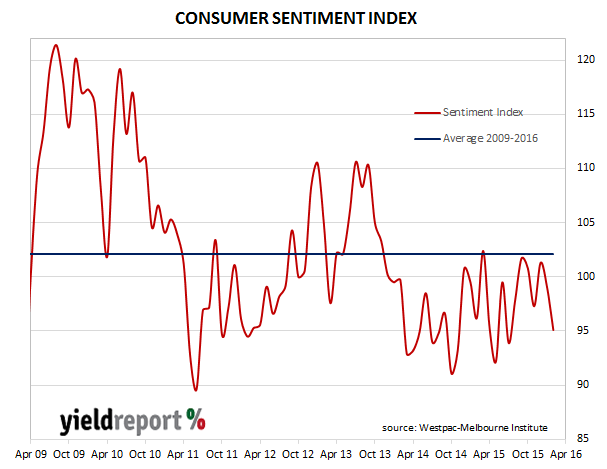

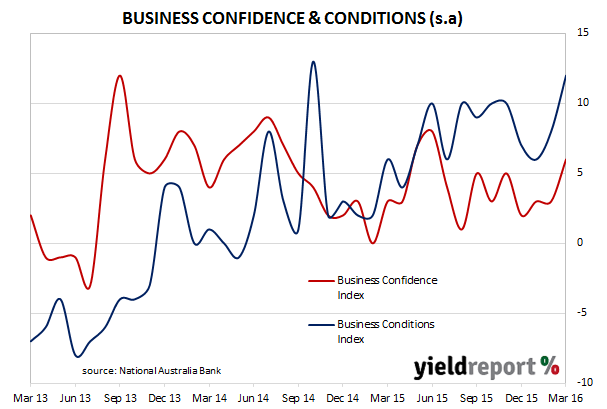

Earlier this week NAB released its business conditions and confidence survey which sent bond yields higher on the back of business conditions being at an 8 year high. Memories of the financial markets turmoil earlier this year may be fading but the business confidence is not extending to consumers.

The latest Westpac Melbourne Institute consumer sentiment survey was described by Westpac’s chief economist Bill Evan as “disappointing” after the index came in below 100 for the second consecutive month. Readings below 100 indicate the number of pessimists outweigh the number of optimists. Given the long term average reading is 101.30, readings at lower levels indicate Australian consumers have lost confidence, which in turn may lead to reduced spending and employment opportunities in the domestic economy. AMP Capital’s Shane Oliver said this latest survey keeps an “RBA rate cut alive.”

Four of the five components of the index fell in April and the only component to rise, the ‘time to buy a major household item’ component, rose just 1%. Mr Evans said international news, the recent fall in the Australian share market and media coverage of China’s economy were probably behind consumers’ unease and he noted how sentiment towards housing had fallen ”sharply”.

13 April 2016

In recent weeks YieldReport has noted the recent popularity of floating rate notes (FRNs) and bonds among issuers and investors. Commonwealth Bank has kept the trend intact by issuing $2 billion of new 3 year benchmark FRNs at 3m BBSW + 98bps. This margin is exactly the same as the $2billion worth of NAB 3 year FRNs issued in March. The two banks share the same credit rating and are clearly two of the four major banks in Australia.

It’s already been a busy week for the CBA. The latest issues comes on top of £250 million of 1 year FRNs issued in the UK and nearly $300 million of 1 year and 3 year fixed rate bonds issued into the domestic market in the last few days.

12 April 2016

Australian businesses appear to have navigated global uncertainties relatively well with business conditions and confidence levels markedly higher in March, according to NAB’s latest Monthly Business Survey. Its Business Conditions Index rose from 8 to 12, while the Business Confidence Index rose from 3 to 6. Business conditions are now at an 8-year high and back to pre GFC levels.

UBS referred to the combination of improved business conditions and very low inflation pressures as “a Goldilocks combination which should please the RBA” while ANZ noted the outlook for the business sector “is much more robust now”. JP Morgan said the NAB survey results provide “a reliable signal of the rebalancing that would eventually become evident in GDP and employment data.” NAB said their GDP model now indicates “solid” GDP for Q1 (March quarter) 2016, “with no more cash rate cuts expected.”

Domestic bond markets reacted by sending interest rates higher. Implied yields on 3 year and 10 year bond futures both increased by 5bps to 1.84% and 2.46% respectively.

08 April 2016

The news in the global steel industry has been one of woe and misery but it seems there is the odd exception. Moody’s announced the upgrade of BlueScope Steel’s senior unsecured debt to Ba2 from its previous Ba3 rating as a result of the streel maker’s improving financial profile. At the same time, Moody’s changed BlueScope’s ratings outlook from “stable” to “positive”.

Moody’s says BlueScope has been the beneficiary of the lower raw materials costs and a cost cutting programme whose effects are now coming through. Moody’s said, “The company is also now reaping the benefits of restructuring and cost-cutting initiatives. These positive factors are offsetting the effects of a difficult global environment for steel producers.”

08 April 2016

Paper money wears out quickly and new bank notes must be printed just to replace damaged ones. So it is with interest we note that Japan’s Ministry of Finance (MoF) plans to increase the number of ¥10,000 notes by 17% for the 2015/16 financial year. In contrast the number of ¥5,000 notes to be issued in the same period will fall by 28% while ¥1,000 notes newly issued will fall by 6%. In the five years to June 2015 Japan’s printing of ¥10,000 notes had been constant but the implementation of a negative interest rate regime has seen Japanese households start to hoard cash rather than pay banks to hold their money.

Central banks in Europe are debating the continued existence of high denomination notes and are suggesting that they only help those in cash businesses and criminals. Countries which have the euro as their currency have discovered negative interest rates tend to promote cash hoarding and the largest denominations became the most popular ways of storing cash. The central banks want citizens to spend money not hoard it and so are concerned that the large denomination notes allow citizens to store cash easily – in effect thwarting some of the aims of their quantitative easing programmes.

The actions of the MoF in Japan suggest it has taken the increasing cash holdings by Japan’s citizens as just a fact of life, at least for now. Dai-ichi Life Insurance’s chief economist, Hideo Kumano estimated the total amount of cash kept at home has risen by 14% in the past year alone. He said it is likely to be the result of people’s desire to keep their wealth unknown to Japanese authorities after a new tax and social security identification system was introduced but he also thinks the Bank of Japan’s (BoJ) negative interest rate policy is a factor.

Recent BoJ data indicates currency in circulation rose 6.7% over the year to February, the highest rate in 13 years and perhaps evidence of Japan’s increased reliance on physical cash. At the end of February, the number of ¥10,000, ¥5,000 and ¥1,000 notes in circulation increased 6.9%, 0.2% and 1.9% respectively.

Related Articles

500 euro note an obstacle to ECB policy

Zero % rates and the Swiss 1000 franc bank notes

07 April 2016

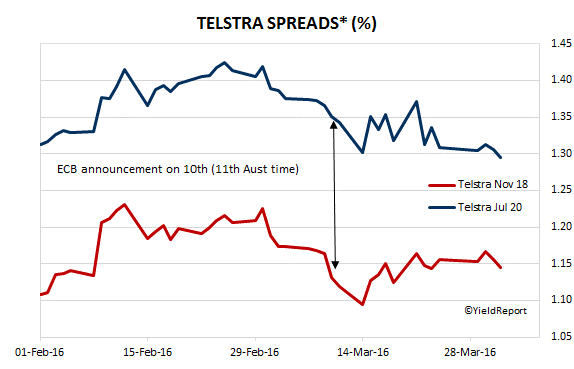

We got another taste of the level of European investor demand for blue chip corporate debt this week when Telstra placed €750 million worth of March 2028 bonds at 20-25bps less than initially indicated. Telstra has an A/A2 credit rating and the substantial discount obtained by the telco group lends credence to the theory the ECB’s asset purchase programme is behind the recent narrowing of corporate spreads over government bonds.

* spread to comparable ACGB

* spread to comparable ACGB

Initially the ECB programme was limited to euro-denominated covered bonds. It was then expanded to state-backed company bonds in 2015 and in February this year it was expanded to investment-grade euro-denominated bonds issued by non-bank corporations established in the euro area. While Telstra does not fit the definition, as yields of bonds which do fit the definition fall, yields on other comparable bonds begin to look relatively more attractive. Because of the ECB buying, the relative shortage of available bonds for other investors has provided Telstra with a windfall benefit on issue.