01 March 2016

The RBA left the cash rate at 2.00% at its March 2016 board meeting earlier today. This makes it the ninth meeting in a row where the official cash rate has not changed. Economists were not expecting any change and cash markets had factored in only a slim chance of a March cut, with the market pricing implying a much higher chance of a rate cut in coming months.

The Bank’s statement repeated a few things such as the reference to the global economy continuing to grow more slowly than earlier expected and how inflation was low but it was expected to be “close to target”.

The Bank noted how several advanced economies (US, UK) had improved growth rates over the last year and that China’s growth rate “continues to moderate”. It also noted that borrowing costs for high-quality borrowers are “very low” and monetary policy is “remarkably accommodative” however, “funding conditions for emerging market sovereigns and lesser-rated corporates have tightened.”

Some parts of the statement were almost positive in their tone; “the expansion in the non-mining parts of the economy strengthened during 2015”. The banks said that although mining investment contracted, improved labour market conditions and a pick-up in the pace of lending to businesses was noted.

All the same, AMP Capital’s Shane Oliver said, “I’ll stick to my view that there will be another rate cut out there from the RBA, probably around May.”

Full text of the statement is available at http://www.rba.gov.au/media-releases/2016/mr-16-04.html

01 March 2016

BHP Billiton has had its ‘A’ credit rating affirmed by Standard & Poor’s after bowing to market pressure and changing its dividend policy. The statement by S&P referred directly to the change in dividend policy and the additional financial flexibility the company now had. The ‘progressive dividend’ policy that BHP had previously adhered to has now been abandoned in favour of a policy that will pay out at least half of its operating profit.

01 March 2016

Newcastle Permanent was last seen in the domestic bond market in the first quarter of 2015 when it issued 3 year and 5 year FRNs at BBSW + 110bps and BBSW + 130bps respectively. One year later, the building society will be meeting with investors in Melbourne and Sydney in the second week of March with a view to another bond issue, although whether the new securities will be fixed or floating is currently unknown. Newcastle is rated BBB+ by Standard & Poor‘s and A2 by Moody’s.

29 February 2016

Moody’s Investor Services has upgraded the senior unsecured credit rating of Qantas to Baa3 from Ba1, a notch above junk bond status, as the airline continues to improve its operating performance and balance sheet.

26 February 2016

Recently YieldReport flagged an Australian bond issue was coming from the Atlanta-based Coca Cola Company and how a non-bank issuer with a high-end credit rating would allow investors a little more diversity in their bond portfolios without taking on additional credit risk. The issue has not eventuated as yet but perhaps this is just as well from an investor’s point of view as the company’s credit rating has just been downgraded a notch by Standard & Poor’s from AA to AA-. At AA-, Coca Cola is still on par with the major Australian banks and still considered to be blue chip issuer. Its credit rating is also still higher than its arch rival PepsiCo Inc. which is rated A by Standard & Poor’s.

The downgrade has come because S&P is concerned the reduction in leverage from the sale of Coca Cola’s interests in US bottlers will not be sufficient to meet the rating agency’s debt requirements for a AA rated company. Coca Cola has been selling assets since 2013.

26 February 2016

Westpac’s new Tier 2 debt deal was today priced at BBS + 310bps. The deal is Basel 3 compliant and expected to be rated BBB+ (stable) by S&P and A3 (stable) by Moody’s. Maturity is 10 years (10 Mar 2026) with a non-call period of 5 years.

Westpac to launch new Tier 2 deal

25 February 2016

Westpac Banking Corporation has launched a new AUD Basel 3 compliant Tier 2 transaction. Basel 3 compliance indicates the securities will have either “non-viability” or “common equity” trigger clauses which effectively convert the debt to equity in the event of financial distress. The expected benchmark 10-year non-call 5-year transaction will be offered to wholesale investors and is expected to be priced in the coming days.

25 February 2016

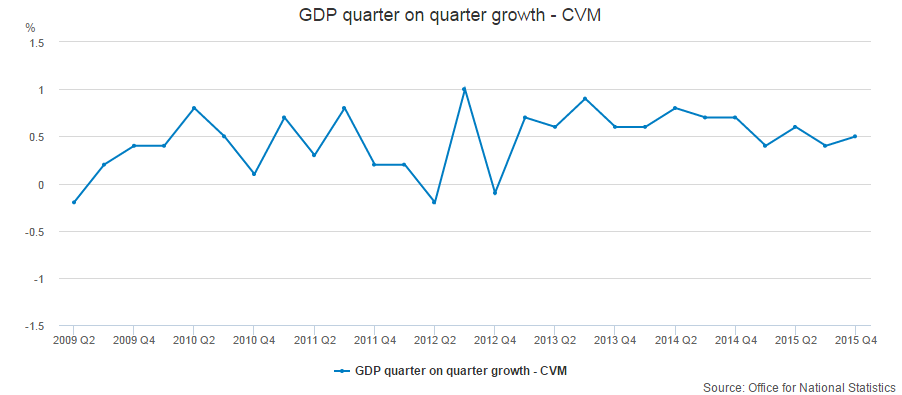

The UK now has the fastest-growing economy among G7 countries. Preliminary figures released indicate the UK economy grew by 0.5% in the December quarter and by 1.9% when compared to the December 2014 quarter. Household spending and business investment provided the bulk of the growth, while the net exports component was a drag on the total growth figure.

The comparable September figures were 0.5% and 2.0%, so the latest figures indicate the UK economy’s growth is not accelerating. It was, however, the fastest growing economy in the G7 group of nations in the December quarter, which includes the US (0.2%) and Germany (0.3%). 0.2% of growth in the came from net migration, with the UK jobs market one of the few European markets which holds an attraction for job seekers.

Preliminary estimates contain less than half of the total data required for the final output estimate and are subject to revision. The Office of National Statistics says revisions are typically small between the preliminary and third estimates of GDP, which means this latest set of GDP data provides a good picture of the UK’s economic performance.

25 February 2016

Just a couple of days ago YieldReport informed readers of Toyota Finance (Netherlands) issuing AUD-denominated bonds into the euro bond market, most likely taking advantage of a currency/interest rate swap anomaly. This time it’s Toyota Finance Australia’s turn but instead, the bonds have been sold in the US market. The USD$66 million worth of bonds have a March 2020 maturity and carry a coupon of 1.18%. Corporate issuance went into hibernation during the recent bout of financial market turmoil but recently few high quality issuers have decided to take advantage of record-low benchmark rates. Toyota Finance, with a AA+ rating from Standard & Poor’s, is one of those high quality issuers which has the ability to issue bonds in almost any sort of environment.

25 February 2016

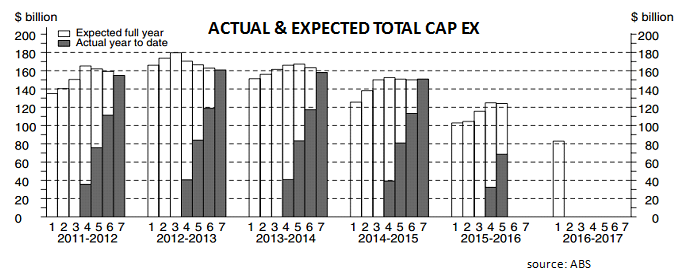

Fourth quarter private capital expenditure figures have been released by the ABS and the 0.8% quarter-on-quarter figure was better than the 3.0% fall expected by economists, although it is still 16.4% lower than the corresponding period a year ago. Capex figures have been easing off since 2013/2014 but the decline has accelerated in recent quarters (see below chart), which has provided some impetus to calls for a lower cash rate to stimulate investment in other sectors of the economy.

10 year bond yields fell from 2.43% to 2.39% before recovering a little in the afternoon. The AUD was immediately sold off against the greenback from USD$0.7190 to USD$0.7160, before it recovered to USD$0.7170.

CBA’s chief economist Michael Blythe said, “It’s better than expected in terms of the GDP numbers next week, but otherwise looking ahead it’s more of the same story, with further declines in mining Capex as you would expect as those big projects wind down. The non-mining side that we’re all hoping will start to pick up is still looking fairly soft overall.” RBC Capital Markets senior economist Su-Lin Ong said, “It is consistent with the RBA’s easing bias. We have pushed back our forecast of a rate cut to Q3. We have another easing in Q4.”

Estimate 5 for 2015/16 Capex plans is now $124.0 billion, 0.6% higher than November’s Estimate 4 of $120.4 billion but 18.8% lower on the previous year’s Estimate 5 of $150.8 billion. The Capex forecasts are updated in sequence and from the chart above, it becomes clear how the estimates change over time.

25 February 2016

The University of Melbourne made its inaugural foray into the US private placement market, with a multi-tranche issue of bonds worth an approximate AUD$275 million. Part of the reasoning behind the offshore issue is to diversify the university’s funding in terms of sources, currencies and duration. The result was a four tranche issue which extended the average debt maturity by 10 years for a 0.3% increase in the average cost of debt.

Demand was strong, with the equivalent of AUD$2.4 billion worth of bids made, which led to a tightening in pricing and an increase in the issue size. The university is rated AA+ by Standard & Poor’s. YieldReport will provide further details when they come to hand.