18 February 2016

Goldman Sach’s economics research team has released a note saying it expects two 0.25% rate cuts by the RBA in the next 5 months: one 25bps cut in May and one 25bps cut in July. This would take the cash rate to 1.50%.

Cash markets are already pricing in one rate cut as a certainty by September but the team at Goldman has gone out on a limb with its “two cuts” call.

The thinking behind such a bold call is that the US Fed will raise rates at a gentler pace than previously anticipated. The difference between the US rate and Australia’s rate will lead to an appreciation in the AUD/USD exchange and the RBA will then have to cut rates to take ease the pressure on Australia’s economy (a stronger AUD makes it harder for Australian exporters and Australian business to compete against imports).

This is not the only the reason. The GS team believe inflation figures will less than expected in the next few months and employment figures have been overstated. A fiscal tightening is expected from the Commonwealth Government and Goldman’s Financial Conditions Index is at a level higher than where previous cuts have been made.

This is not the first time the Goldman Sachs team has suggested a change in monetary policy which stands out from the market. In October 2015 the team said a November rate cut was “highly likely” while the market pricing for such a reduction was only suggesting a 40% chance of this occurring.

18 February 2016

The minutes of the January meeting of the FOMC were released overnight and they showed that the US Fed was watching global events unfold and were slightly concerned about tighter global financial conditions. “If the recent tightening of global financial conditions was sustained, it could be a factor amplifying downside risks.” The tightening of conditions was perhaps “roughly equivalent” of a de-facto monetary policy tightening.

The Fed was watching the greater-than-expected slowdown in China and emerging market economies trying to calculate whether there would be a “potential drag on the US economy” that may cause it to raise rates at a slower pace than anticipated.

The Fed raised interest rates in December for the first time in nearly a decade and it has indicated it expects to raise rates gradually in 2016 as the US economy picks up. Markets are fixated on the timing of any rate raises and scrutinise the Fed minutes for any minor change in the language used.

16 February 2016

Bank Nederlandse Gemeenten, a regular in the Kangaroo market, has reportedly issued a new line of August 2026 bonds. The $50 million bond sale was priced at ACGB + 63.5bps and it comes just one month after the Dutch municipal bank issued $90 million worth of July 2025s. In contrast to KBN’s latest bond issue, BNG is paying a smaller margin above the Commonwealth benchmark than it has for its bond sales through 2015.

12 February 2016

Just over a week ago YieldReport alerted readers to the mayhem being wrought upon the two series of notes issued by Crown Resorts in a piece titled “Crown Note 13% Yield Not for the Faint-Hearted”. In that article it was mentioned the series 2 notes had hit a new price low of $69.50 before finishing the day a little higher.

The notes have a $100 face value so a 30.5% discount is quite impressive. But it is not quite as impressive as the 34.5% discount the latest closing price of $65.50 represents or the 37.50% discount present when the notes hit $62.50 during the day.

The major issues surrounding the notes have already been covered so they won’t be rehashed here but it seems as if the current market for these notes are still trying to find a level where the uncertainty surrounding the redemption date is offset by such a sizable discount.

12 February 2016

UK 10 year bonds last night fell to a record low of 1.29% as investors continued to flee risk assets and look for safe havens. The move is the latest in a savage round of ring-a-rosy where commodity prices fall, putting downward pressure on share markets and in particular bank prices. Investors looking to park money are accepting lower and lower returns for the benefit of investment safety.

11 February 2016

Janet Yellen gave her semi-annual testimony before the US Congress and the tone of her comments revealed a slightly more cautious tone. Yellen’s testimony implied a March rate increase is unlikely but that the Fed is still being careful not to rule anything out beyond that while she reiterated the Fed’s expectation of gradual interest rate increases. Pricing in US cash markets currently implies a low probability of an increase at the next FOMC meeting.

Yellen said financial conditions have become less supportive of US economic growth. Jitters in the junk bond market which arose after the collapse of the Third Avenue Focused Credit Fund, had led to higher lending rates up and tightened commercial lending standards and if those trends continue, U.S. economic growth could be hurt.

Offshore developments could weigh further on the U.S economy, she said, while emphasizing that officials are watching developments in global financial markets carefully. The impact of a slowing Chinese economy and its financial market turmoil is a major concern and the US economy is also being hampered by a higher USD, which is hurting the US export sector and making life more difficult for US businesses which compete against imports.

When the topic of negative interest rates arose, Yellen said she wasn’t aware of any law that prevented the Fed from using negative rates. The Fed had considered using negative rates in 2010 but the idea was dismissed. (A 2010 Fed memo raised some doubts about the 2006 Financial Services Regulatory Relief Act allowing such a move). Yellen said it was unlikely the Fed would cut the official rate anytime soon from its current 0.25%-0.50% target range.

While her testimony placed a heavier emphasis of downside risks, the Fed chair noted how the unemployment rate was under 5.0% and the low price of oil could further stimulate already-consistent consumer spending. Even with gradual rate increases, she said the Fed anticipates “labour market indicators will continue to strengthen.”

Westpac said the overall impression is one of a Fed likely to remain on hold in March but intent on gradual increases in interest rates. ANZ’s view was the FOMC “will cut its inflation outlook and probably tweak its GDP forecasts and its ‘dot plot’ in March”. It expects the number of rises this year to be limited to two, or three at the most, rather than the four implied by the last FOMC statement.

Click here for the full transcript.

09 February 2016

The former chief economist of the Bank for International Settlements, Bill White, said in an interview this week that ultra-loose monetary policy and the “experimental use” of negative interest rates was making the global economy more vulnerable. Monetary policy is trying to “stimulate aggregate demand and the honest truth is that it’s not capable of doing that in a sustainable way…If people thought we were in a period of deleveraging that would set the scene for a period of robust growth. We haven’t even started yet…Negative rates on reserves are actually squeezing bank profits, and this is something we don’t want in these circumstances, we want them to build up their capital buffers. This is all experimental.” The BIS serves as the bank that central banks use for their banking services.

08 February 2016

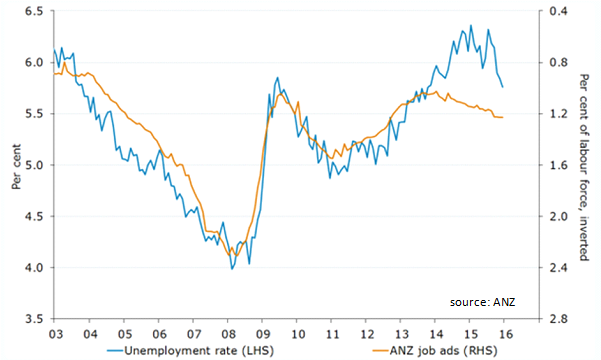

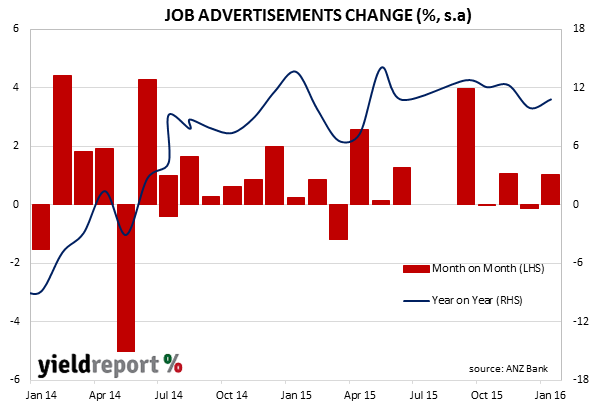

ANZ’s monthly job ads survey was released showing ads were up 1.0% s.a. compared to December and up 10.8% from January, 2015. The comparable December figures were -0.1% and +9.9% respectively. Internet ads were up 1.1% for the month (12.1% for the year) while newspaper ads fell 3.2% (-13.1% for the year). Advertising through newspapers is now close to non-existent and just a small percentage of the internet advertising.

ANZ’s chief economist Warren Hogan said, “Overall we see the job ads series, in conjunction with other leading indicators of labour demand, as consistent with further moderate employment gains in early 2016, enough at least to keep the unemployment rate stable… In 2016 it is unlikely that the Australian economy will enjoy the same strong rate of job creation witnessed in 2015.”

CommSec chief economist Craig James said of the results, “The job market continues to strengthen, underpinned by the low growth of labour costs and firm demand for workers across the services sector.” He added the results made future interest rate cuts less likely.

08 February 2016

Moody’s Investor Services has downgraded the credit rating of Western Australian Treasury Corporation – the borrowing authority of the Western Australia government – from Aa1 to Aa2. The outlook is stable.

Western Australia is a resource rich state that has been hit hard by huge falls in commodity prices that have seen state revenues cut dramatically. The government has been accused of spending the riches from the resources boom that never eventuated. The budget position has deteriorated to such an extent that resource revenues now only account for 14.8% of total revenue compared with 21.6% at its peak. The state’s debt burden was around 44% of revenue in 2008 and is now around 102% and forecast to widen further in 2015/2016 to 128%.

A stable outlook was assigned to the rating because of support provided by Australia’s institutional framework to states and territories and expectations that Western Australia’s policy response will strengthen if its fiscal performance deteriorates well beyond what is projected.

08 February 2016

Unemployment in the US dropped to 4.9% as the US created another 151k jobs in January. The number of jobs was less than the market was expecting at 185k which added fuel to some commentators’ arguments that the US might be headed for recession in 2016. Others such as the Royal Bank of Canada, said in a report “The short-sighted folks out there will, on the basis of private job gains missing the mark by a mere 22,000, conclude that this was a weak report, but the underlying details suggest otherwise”. A significant element of the payroll report was the significant jump in wages. RBC further commented that “Wage pressures look to be perking up now that we have crossed into the Fed’s explicit full employment zone and thus continued declines in the unemployment rate should ultimately put some pressure on the FOMC to maintain a bias to continue removing accommodation.” The wage growth numbers in particular would appear to support the US Fed’s decision to raise interest rates at its December 2015 meeting, a decision that has been widely questioned with the extreme volatility seen in markets at the start of 2016.