11 November 2015

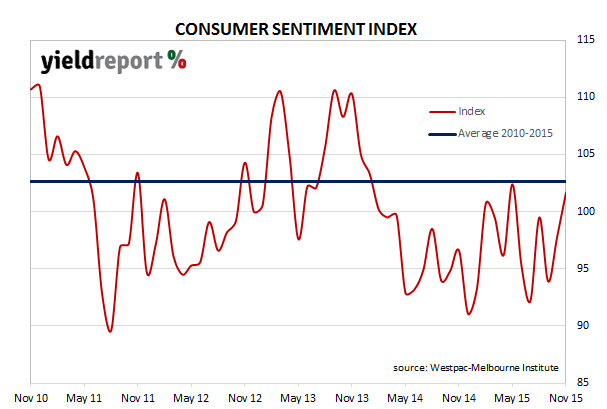

The Westpac-Melbourne Institute index of consumer sentiment increased to 101.7 in November from the October recording of 97.8. The rise in the index indicates an increase in the ratio of optimistic consumers to pessimistic consumers and it follows on from of October’s rise. A reading above 100 means there are more positive responses from people in the survey than negative ones.

Bill Evans, Westpac’s chief economist, described it as a “cracking result” and he went on to say, “It marks only the third month out of the last twenty one that optimists have outnumbered pessimists”.

In spite of the banks’ decisions to raise mortgage rates, the confidence of respondents who hold a mortgage increased by slightly more than the increase in the overall index. Individual components of the index suggest people in the survey may be concerned about their personal finances but these concerns are being outweighed by a generally positive view of the overall economy. While the survey indicates more people think unemployment will rise in the year ahead, the unemployment component of the index remains 10.9% below the September level, which indicates people are generally less pessimistic about their employment prospects than they have been for some years.

All this leads the chief economist to say growth in the Australian economy “will remain sufficiently supportive through 2016 to ensure steady rates.”

Domestic bond markets may have already priced the news in as the 3 year bond futures yield fell 2bps to 2.03% while the 10 year bond futures yield also closed 2bps lower at 2.90%.

11 November 2015

Fortescue Metals Group Ltd has launched a US$750 million debt repayment offer for senior unsecured notes with maturities in 2019 and 2022 via a tender. The company has offered to purchase up to US$750 million (in face value terms) of the two series of notes via a modified Dutch auction.

The price range for the 8.25% 2019 series will be between 88% and 93% of face value while the 6.875% 2022 series will have a price range of 75% and 80%. Notes tendered before 24 November 2015 will receive a bonus 3 cents in the dollar in what seems to be a large inducement by Fortescue to get the deal done as quickly as possible.

The upcoming tender continues Fortescues recent practice of buying back debt. Fortescue repurchased USD$384m in the September quarter, although those purchases were made in the secondary market and not via an official tender. Fortescue said it had paid an average 80 cents in the dollar for that debt, with about 40% of the purchases made in the 2019 unsecured bonds and about a third in the 2022 secured bonds and the balance put towards the 2022 unsecured bonds. Prior to the September quarter purchases, there was another tender in March where bonds with maturities in 2017, 2018 and 2109 were purchased, mostly at prices close to par value and with a bonus 3% if tendered early.

Chief Executive Officer Nev Power said, “Accelerating Fortescue’s debt repayment programme through this tender will further reduce our interest costs while ensuring that we remain on track to achieve our initial gearing target of 40 percent.”

10 November 2015

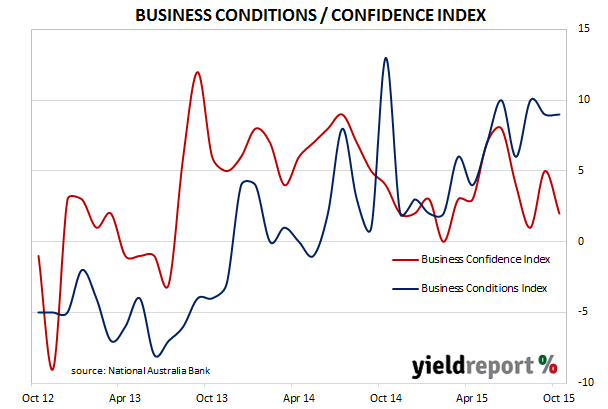

Business confidence has fallen in October after a string rise in September according to National Australia Bank’s latest survey. The index fell 3 points to +2, reversing the 4 point gain in September. As part of the same survey, NAB also measures business conditions and this index remained steady with last month’s reading of +9.

NAB described business confidence as “somewhat fickle” despite strong business conditions. The index reading of +2 was still “well below” the long run average and the deterioration was reasonably broad based but the bank noted the finance, property, business, manufacturing sectors improved and in the case of the mining sector, was less negative. Westpac interpreted the results as an indication the RBA’s actions earlier in the year were kicking in. “This strengthening of business conditions suggests that lower rates and a lower dollar are having a positive impact.”

UBS said the employment intentions part of the index “are consistent with ongoing solid ~2% jobs growth.” Goldman Sachs was less positive in its view and said, “We retain a far more cautious interpretation of these data and still see the risks as skewed towards the broader recovery falling short of expectations.” NAB said the market’s pricing for another cut in the next six month was overly pessimistic. With the release of the October indices, the bank reiterated its view of rate cuts as being “unlikely” and it expects official rates to be hold. However, it acknowledged how the timing of the first rate rise had been pushed out to 2017.

Domestic bond markets received the data as being positive for growth prospects and pushed the 3 year bond futures yield up 2bps to finish the day at 2.05% while the 10 year bond futures yield closed up 1.5bps at 2.92%.

10 November 2015

The value of loans for housing fell by 1.6% in September, led by an 8.5% drop in the value for loans to investors. The total value of loans approved for housing was down on August’s figure of 3.5% and the turn-around may mark the beginning of the end for the decade-long housing boom. “Owner-occupied” housing loans grew by 3.0% but even then they were down from August’s 6.1% increase. In terms of the number of loan applications approved, loans to owner-occupiers grew by in 2.0, down from the 2.9% increase recorded in August but better than the market forecast.

Goldman Sachs noted the rise in owner-occupier approvals was mostly the result of refinancing while approvals for new construction were “sharply lower over the year” and “ongoing macro-prudential policies have proved effective in curbing investor lending.” The investment bank said this would give policymakers room to cut rates “should the broader demand side of the economy warrant it.”

Back in September AMP’s Shane Oliver thought the new APRA lending guidelines were likely to have an effect on investor lending and this latest batch of loan data seems to be confirming his suspicions. He thinks the latest data points to a definite slowing, event taking into account the reclassification of some investors as owner occupiers.

09 November 2015

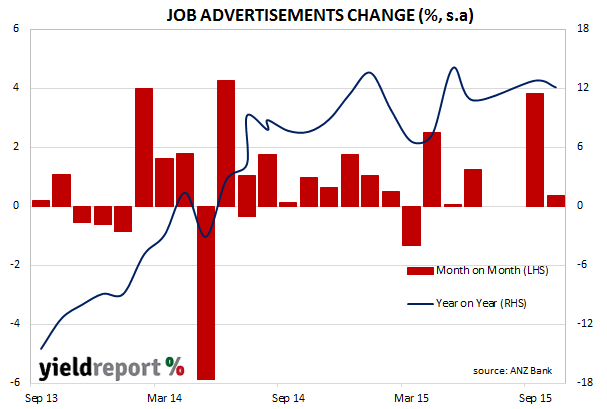

ANZ’s monthly job ads survey was released showing ads were up 0.4% (seasonally adjusted) compared to September and up 12.1% from October, 2014. The comparable September figures were +3.9% and +12.8% respectively. Internet ads were up 0.3% for the month while newspaper ads were up 3.0%. Compared to a year ago internet ads were up 12.9% while newspaper ads were down 15.3%.

ANZ’s chief economist Warren Hogan said, “The improving trend in job advertising is good news. Despite some challenges, the economy overall is currently tracking along pretty well.” He expects the labour market to remain “quite good” and even thinks the unemployment rate may drop a little. However, he expects the jobs growth to be temporary and “likely to wane in the first half of 2016.”

09 November 2015

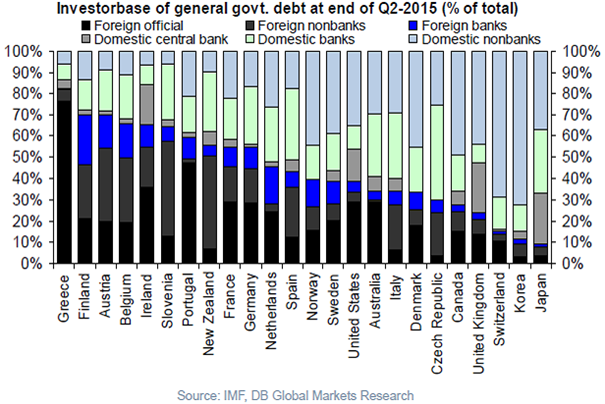

An interesting chart from Deutsche Bank shows who owns the government bonds from different countries around the world.

09 November 2015

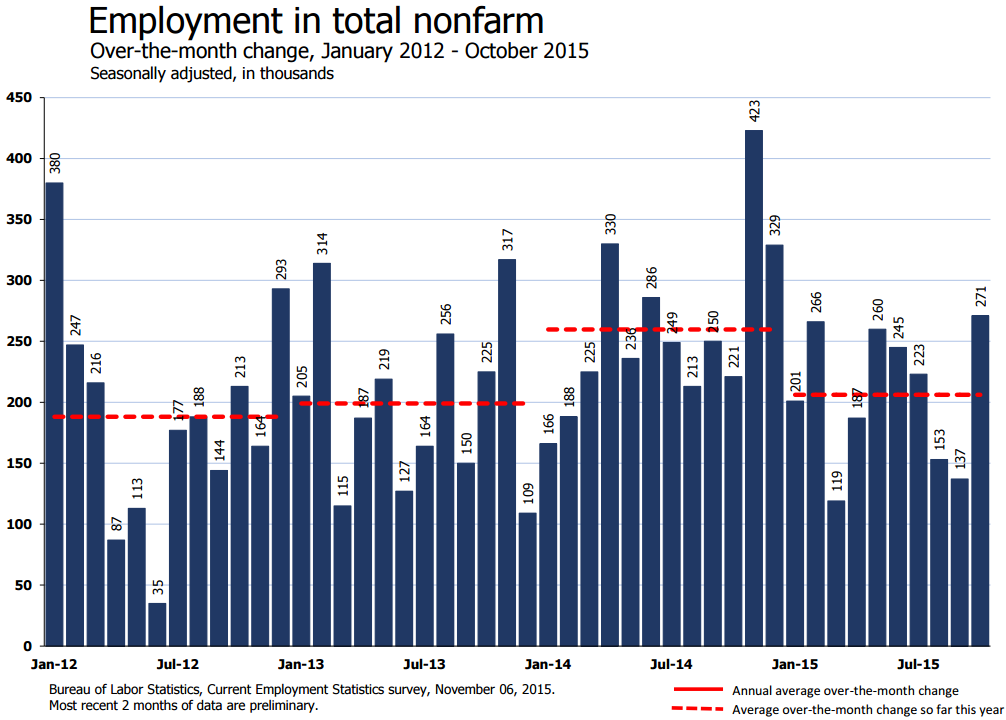

A massive jump in US non-farm payroll numbers on Friday has seen the odds of a December rate hike by the US Federal Reserve increase sharply. The US economy added 271k jobs in October and unemployment dropped to 5% – a level that most analysts call “full employment”. The market was expecting jobs growth of 182k.

The odds of a rate hike jumped to over 70% and US 2 year Treasurys hit an intra-day high of 0.96% – the highest in 5 years.

Job numbers for August were revised up from 136k to 152k and for September revised down from 142k to 137k. Average jobs growth over the past three months is 187k. Wages growth was also particularly strong at 2.5% year-on-year. Average hourly earnings have been the missing ingredient in the employment puzzle and this number is the strongest since 2009.

05 November 2015

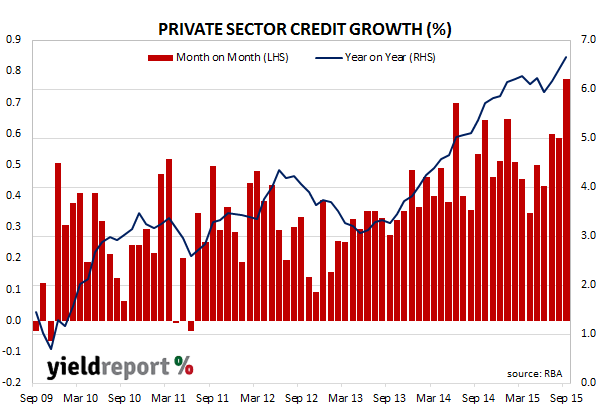

Loans to the private sector grew at a slightly higher rate in September. Loans to business were the main drivers of the higher-than-expected figures, with total credit rising 0.8% for the month compared to the 0.6% recorded in August. Total credit grew by 6.7% in the year to September.

Business loans, which accounted for 33% of all loan growth in the month, grew by 1.2%, while housing loans which account for just over 60% of monthly loan growth, grew by 0.6%. The balance which comprises personal loans, grew by 0.1%.

In the housing component, “owner-occupier” housing grew at 0.7%, up from August’s 0.6% while investor loans growth grew by 0.5%, down from August’s 0.6%.

Westpac said the tightening of investor lending conditions is driving a clear shift in housing lending away from investors to owner occupiers.

05 November 2015

ANZ is looking to issue Tier 2 subordinated notes, subject to market conditions. ANZ has the mandate. More when information is available. (update) ANZ’s AUD Tier 2 deal is a 10.5 year maturity with no-call for 5.5 years at a price around BBSW + 270bps. Size of the deal is $600m.

According to YieldReport tables, a similar Tier 2 deal in July 2014 from ANZ – a Tier 2, $750m 10 year, no-call for 5 years, sold at BBSW + 193bps.

04 November 2015

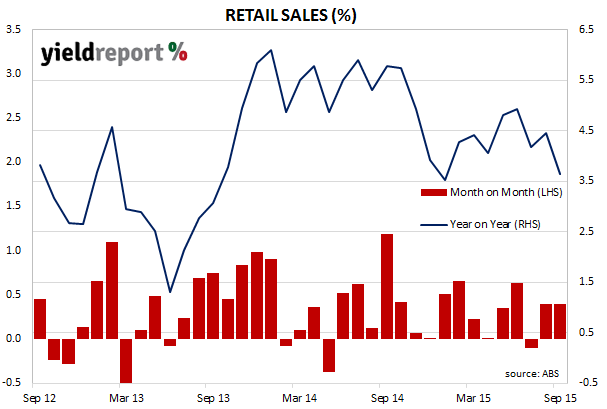

The Australian Bureau of Statistics released September retail sales figures which were pretty much in line with expectations, rising a seasonally adjusted 0.4% for the month and the same as the August figure. The overall rise was driven by sales at restaurant, cafes and household goods and all states had gains except for Queensland and the ACT where seasonally adjusted sales fell 0.3% and 0.1% respectively. On a year-on-year basis, sales were up 3.6%, down from August’s annual figure of 4.5%.

Commonwealth Bank described the September growth rate as “tepid” while Westpac noted the large retailers were behind the increase, as small retailers were struggling. Westpac also made mention of the larger-than-expected increase in the retail price deflator which is a measure of price rises in the sector.