04 November 2015

The ABS preliminary estimates of the Australia’s September quarter trade deficit and terms of trade were published indicating a recovery in Australia’s export earnings and prices received. The trade deficit narrowed to $7.5 billion, down from the revised June quarter deficit of $10.5 billion (initially a $9.6 billion deficit).

Westpac economist, Andrew Hanlan, said the most interesting part of the report was the narrowing of the trade deficit in the third quarter on a rebound in exports, which was the result of a lower exchange rate and higher export volumes.

Higher import prices which resulted from the lower exchange rate were largely offset by a fall in volumes, although the net effect was a 1% rise in the value terms. However, in some bright news, Commonwealth Bank said the low exchange rate had “continued to support [the] tourism industry.”

Westpac will revise third quarter GDP estimates up as a result for the figures, but their full year estimate will remained unchanged because of the downwards revisions to the June quarter deficit.

04 November 2015

OCBC (Sydney branch), rated AA-/Aa1, has mandated a new 3 year AUD senior unsecured note. Westpac is the joint lead manager along with OCBC and Commonwealth Bank. More details when they come to hand. (update 5 Nov) The size of the transaction was $400m and the price was set at BBSW + 86bps.

04 November 2015

Australia Pacific Airports Corporation, the owner and operator of Melbourne Airport, has raised $120m in a new 10 year issue led by Citi and ANZ.

The A-/A3 domestic issue was priced at 4.55%.

04 November 2015

The RBA chose to leave rates unchanged at its 3 November board meeting. The cash rate remains at 2.00%. Governor Glenn Stevens, in the accompanying media statement, pointed to the global economy still being very accommodative and noted that some central banks were looking to raise rates in the ‘period ahead’ while others were still easing. In Australia a “moderate expansion in the economy continues” and that “prospects for an improvement in economic conditions had firmed a little over recent months.”

With regard to inflation, Stevens noted that “Inflation is low and should remain so, with the economy likely to have a degree of spare capacity for some time yet. Inflation is forecast to be consistent with the target over the next one to two years, but a little lower than earlier expected.”

Westpac’s senior economist Bill Evans was not surprised that the RBA kept rates on hold. He said that the recent inflation print “allowed the Bank scope to cut if it so desired but that decision would be predicated on a substantial downward revision in the outlook for economic growth.” He didn’t see a downward revision at this point to justify a rate cut and remained of the view that rates would remain at 2.00% throughout 2016.

The market is almost pricing in a full rate cut by February (the RBA board meeting does not meet in January although could agree in advance to alter rates between meetings if certain conditions are met) but by then the RBA will have the benefit of seeing the December quarter CPI, economic activity around Christmas and whether the US Fed has raised interest rates for the first time in over 8 years.

02 November 2015

The Australian Bureau of Statistics released September building approval figures which were better than expected, with total approvals rising 2.2% compared to the expected figure of +1.0%. The increase was driven by a sharp rise in Queensland and robust gains in Victoria which outweighed a significant fall in non-house approvals in NSW.

Private house approvals were down 1.9% for the month but up 1.5% for the year while units were up 6.1% for the month and up a whopping 53.5% for the year. Total approvals were up 21.4% for the year to September, a number significantly higher than the 5.1% increase in the year to August.

Westpac noted how high rise units accounted for all the approvals growth in the last 12 months and this growth was centred on NSW and Victoria. The bank is concerned revisions to previous months “hint at a more rapid underlying slowdown” but “importantly, this will take a long time to feed through into actual construction.”

02 November 2015

Westpac today announced that their full year cash profit was $7.82 billion, up 3% for the year. CEO Brian Hartzer commented on the bank’s capital position saying that the $6 billion of new capital Westpac has raised this year has increased its capital levels significantly. The Murray report in financial services recommended that Australia’s banks needed to be “unquestionably strong” and Mr Hartzer said, “The capital raised responds to regulatory changes that increase the amount of capital needed to be held against mortgages by more than 50 per cent. Our capital raising allows us to meet regulatory requirements while continuing to support growth in the Australian economy.” He also said that Australia is stuck in a “lower-for-longer” environment.

02 November 2015

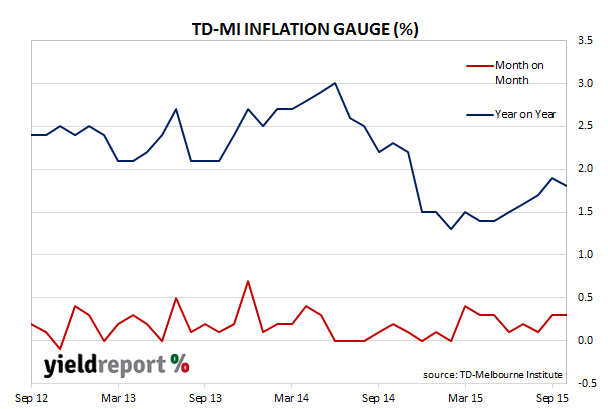

The TD Securities Melbourne Institute Monthly inflation gauge indicator showed there was no change in consumer prices over the month. It put the annual rate of inflation at 1.8%.

Head of TD Securities Asia Pacific research, Annette Beacher, said despite inflation being below the RBA’s target inflation band of 2.0% to 3.0%, the RBA was unlikely to cut rates on 2 November when it next meets. This is in line with the view of the Australian National University’s “shadow RBA board” that forecast no change to rates. The market pricing, using the 30 day cash rate futures, suggests a 44% chance of a rate cut.

Paul Bloxham, HSBC’s chief economist and the only bank economist to sit on the shadow board said that last week’s surprise low CPI release could see the RBA cut rates if it wanted to, “The question isn’t whether growth is picking up; it’s can we get a bit more growth”. This echoes the recent comments by the RBA that monetary policy has its limits and further rate cuts might not have the desired effect of stimulating growth. Other analysts believe the RBA prefers to keep stimulus ‘up its sleeve’ in case the economy takes a turn for the worse and it really needs a rate cut.

Westpac said the Gauge has been “almost spot on” to the quarterly change in the CPI since 2014. “We are now closely watching the Gauge for a lead on the Q4CPI. The Gauge is pointing to another very modest print in Q4.”

30 October 2015

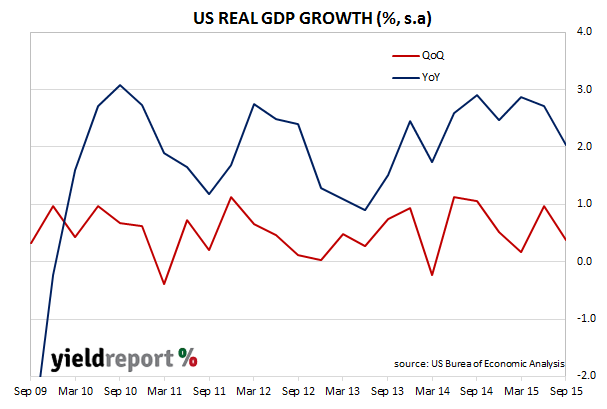

The US Commerce Department released the Q3 GDP “advanced” estimates which showed an annualised growth rate of 1.5%, lower than the consensus estimate of 1.7% and lower than the Q2 figure of 3.9%. Despite the lower than expected figures, US 2 year Treasury notes reacted by moving up 2bps to 0.75% while US 10 year bonds moved 9bps higher to 2.19%.

The fall in the growth rate in the third quarter was the primarily due to businesses drawing down on inventory stocks but according to the Commerce Department all sectors of the economy acted as a drag on the overall growth rate.

Westpac described the result as indicating an economy that was healthy, noting the final sales figure grew 3% which, while not a strong as the 3.9% for the comparable figure in Q2, was in their view still “decent”. ANZ referred to the “robust” domestic demand and said the results were consistent with the Fed’s description of the growth rates as being “solid”.

The Commerce Department calculates the annualised figure by compounding the quarterly result and so a direct comparison with UK or Australian figures is not meaningful. However, if the US GDP growth figures were to be calculated in same way Australia does (that is, q/q and y/y), then the quarterly US GDP figure would be 0.4% s.a. (previously 1.0% s.a.) and the year-on-year figure would be 2.0% s.a. (previously 2.7% s.a.).

30 October 2015

This week Italy sold 2 year bonds, for the first time ever, at a negative yield. The auction for €1.75 billion 2 year bonds were sold at a yield to maturity of -0.23%. The bonds have a zero coupon, meaning investors lent their money to the Italian government and will receive a lesser amount when the bonds mature and, in the meantime, will receive no income. This is quite extraordinary given that Italian short dated bonds hit a high of around 8.10% during the eurozone debt crisis and the fact that Italy has one of the highest debt-to-GDP ratios in the world at around 135%.

The auction comes in the same week as Sweden increased their bond purchases for the 4th time this year on what is being called “QE4” and not long after ECB president Mario Draghi announced that the bank has contemplated further stimulus to the European economy.

YieldReport has already reported on more than USD$1.57 trillion of European bonds trading at a negative yield and this number is bound to go higher. Investors are caught between getting a decent return on their funds and the security of getting their money back at maturity.

30 October 2015

Demand for AMP’s new capital notes in the institutional book-build process has seen the issue upsized from an indicated $200m to at least $230m. The margin has been fixed at the lower end of the initially indicated range at 5.10% above the 90 day BBSW rate. This margin is fixed for the life of the notes with the BBSW rate reset each quarter.

Total return for the first quarter will be around 7.20% including a franking component based on an 85% franking rate.

The $230m is the amount allocated to brokers and institutional investors with the final issue size determined by the shareholder and retail allocation. The PDS for the issue can be found at www.ampcapitalnotes.com.au