29 October 2015

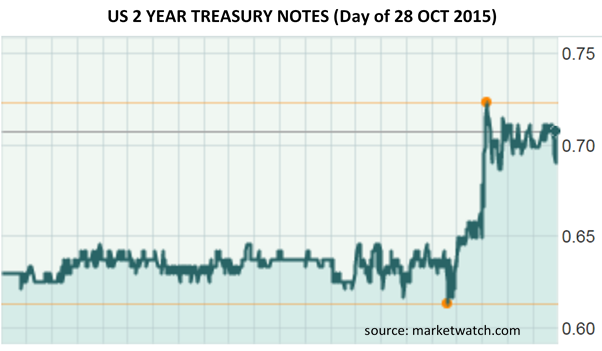

While the odds of an Australian rate cut firmed after the release of the September quarter CPI figures, in the US the odds are in favour of a move in their official rate in the opposite direction. The Federal Reserve’s Federal Open Market Committee finished its two day October meeting and left the federal funds target rate unchanged at a range of 0% to 0.25%. The US cash markets had been pricing a 30% chance of an increase by the end of the year ahead of the decision but shortly after the decision the implied probability was closer to 50%. US 2 year Treasury notes yields rose quickly on the release of the statement and finished at 0.70%, up 7bps on the day.

The committee downplayed the threat to the US economy from the global developments which were a feature of its September statement, a change which Westpac described as giving the statement a “more hawkish twist.” However, the real surprise was the modification to the reference as to how long to maintain its target rate. The latest statement made a direct reference to the next meeting in December with the reference “whether it will be appropriate to raise the target range at its next meeting.” Westpac noted this change and said, “This is by no means a promise of action but was much firmer than markets expected.” ANZ also used the term “hawkish” but said, ”To be fair, a hike in December is far from certain” and pointed out the upcoming data such as US payrolls “will be key”.

For the full statement, click here.

29 October 2015

The Reserve Bank of New Zealand left rates unchanged at its meeting yesterday but signalled it was likely to cut them again. “Some further reduction in the OCR (Overnight Cash Rate) seems likely,” said Governor Graeme Wheeler. “This will continue to depend on the emerging flow of economic data. It is appropriate at present to watch and wait.”

The Bank held rates steady at 2.75% after cutting rates for the three previous months in a decision that was widely expected. The Bank is concerned about a strengthening currency however, noting that the NZD is at a 5 month high against the AUD and heading towards parity again. Inflation is also below the 1.0% to 3.0% target range.

29 October 2015

The ring-a-rosy game of quantitative easing has struck again with the Riksbank of Sweden announcing it will purchase an additional 65bn krona ($10.7bn) of bonds each month – the fourth expansion of the QE programme that it started in February 2015. The bank decided to maintain its benchmark repo rate at -0.35%.

In a statement the Riksbank said, “There is still considerable uncertainty regarding the strength of the global economy and central banks abroad are expected to pursue an expansionary monetary policy for a longer time” and that “an initial raise (sic) in the [repo] rate will be deferred by approximately six months compared with the previous assessment.”

Many state central banks are battling to fight the currency wars that have re-ignited after the announcement by the European Central Bank that it is considering extending its QE programme. The problems for Sweden stem from the fact that its currency is rising and Swedish exports are falling. Inflation is just above zero, well below the Riksbank target of 2.0%. The governor of the bank, Stefan Ingves, flagged that it could cut rates further into negative territory if it needed to. “We do have more space,” he said, “I wouldn’t pin down a floor presently, so we can go below -0.35pc if we need to do that”.

Sweden’s QE programme represents around 5.0% of its GDP and around 34%c of total outstanding debt. This new bond buying will expand the Riksbank balance sheet to around 200bn krona ($33bn) by the end of June 2016. Sweden has a population of just under 10 million people so to put that into an Australian perspective it would be like the RBA buying $107 billion of Australian bonds.

Adding to the uncertain economic environment are the waves of migrants heading to Sweden that are likely to result in huge increases in government spending.

28 October 2015

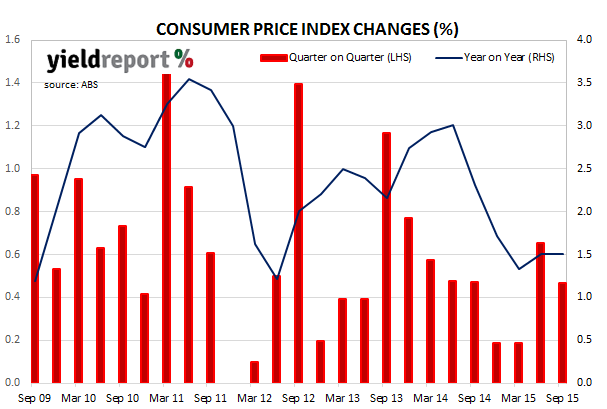

In the wake of the softer than expected September quarter CPI figures, YieldReport put together a round up of analysts’ comments. No commentator which YieldReport follows forecast inflation at such a low rate so the market impact may well be greater than usual.

Chief economist from BT Chris Caton, “Inflation is simply not a concern at present” and suggested that while it’s a close run thing, he is staying with his call that the RBA will not cut in November. Of interest will be the RBA’s rhetoric from next week’s meeting and whether the recent rise in retail mortgage rates gives them a basis to ease without stoking an already hot property market.

Scott Haslem from UBS said, “With core at 0.25% q/q” it was “one of the two lowest outcomes in almost 20 years.” With the headline CPI below the RBA’s 2-3% target now for a year, “there’s little here to stop the RBA offsetting the recent regulatory inspired retail rate hikes when it meets next week.”

Michael Blythe, chief economist at the CBA, noted that the CPI result was below even the RBA’s recent forecast. “Deflation is not a risk” and because there were “some unusual price outcomes in Q3” the CPI was not “low enough to ‘demand’ a rate cut at next week’s RBA Board meeting. “The cash rate should remain at 2% when the RBA meets next week. But the odds on a cut have clearly lifted.”

AMP’s chief economist Shane Oliver, said “The bottom line is that pricing power remains very weak reflecting constrained growth in retail sales and cautious consumer confidence. The fact that inflation is lower than expected and below target despite a 20% plus fall in the value of the $A over the last year adds to the case for the RBA to cut the cash rate again in order to offset the potential negative impact on the economy of big bank mortgage rate hikes. I continue to expect the RBA to cut the cash rate by 0.25% when it meets next week or if not then, then sometime in the next few months.”

28 October 2015

The September quarter CPI figures surprised markets by coming in well below expectations at +0.5% and +1.5% for the year to the end of September. The market expected a +0.7% rise for the quarter and a +1.7% rise year on year. The underlying inflation figure, which strips out the more variable components of the measure, was expected to come in at +0.6% for the quarter and +2.5% for the year and have come in at +0.3% (q/q) and +2.1% (y/y).

Markets immediately saw room for the RBA to cut rates at its 3 November meeting with underlying inflation at the bottom of its targeted range. The dollar fell sharply and cash markets doubled the chances of a November rate cut, now pricing it as a 60% chance.

ANZ said the figures would not trigger a rate cut but nor would it stop the RBA should they decide to reduce rates. Shane Oliver, from AMP, said any inflationary effects from a lower exchange rate was being “swamped” and “there’s no barrier” to a rate cut on Cup Day. He fully expects the RBA to cut next week.

The breakdown of figures are as follows:

September quarter CPI: +0.5%

June quarter CPI: +0.7%

CPI to September year end: +1.5%

Underlying September quarter CPI: +0.3% (trimmed mean)

Underlying June quarter CPI: +0.6%

Underlying CPI to September year end: +2.1%

27 October 2015

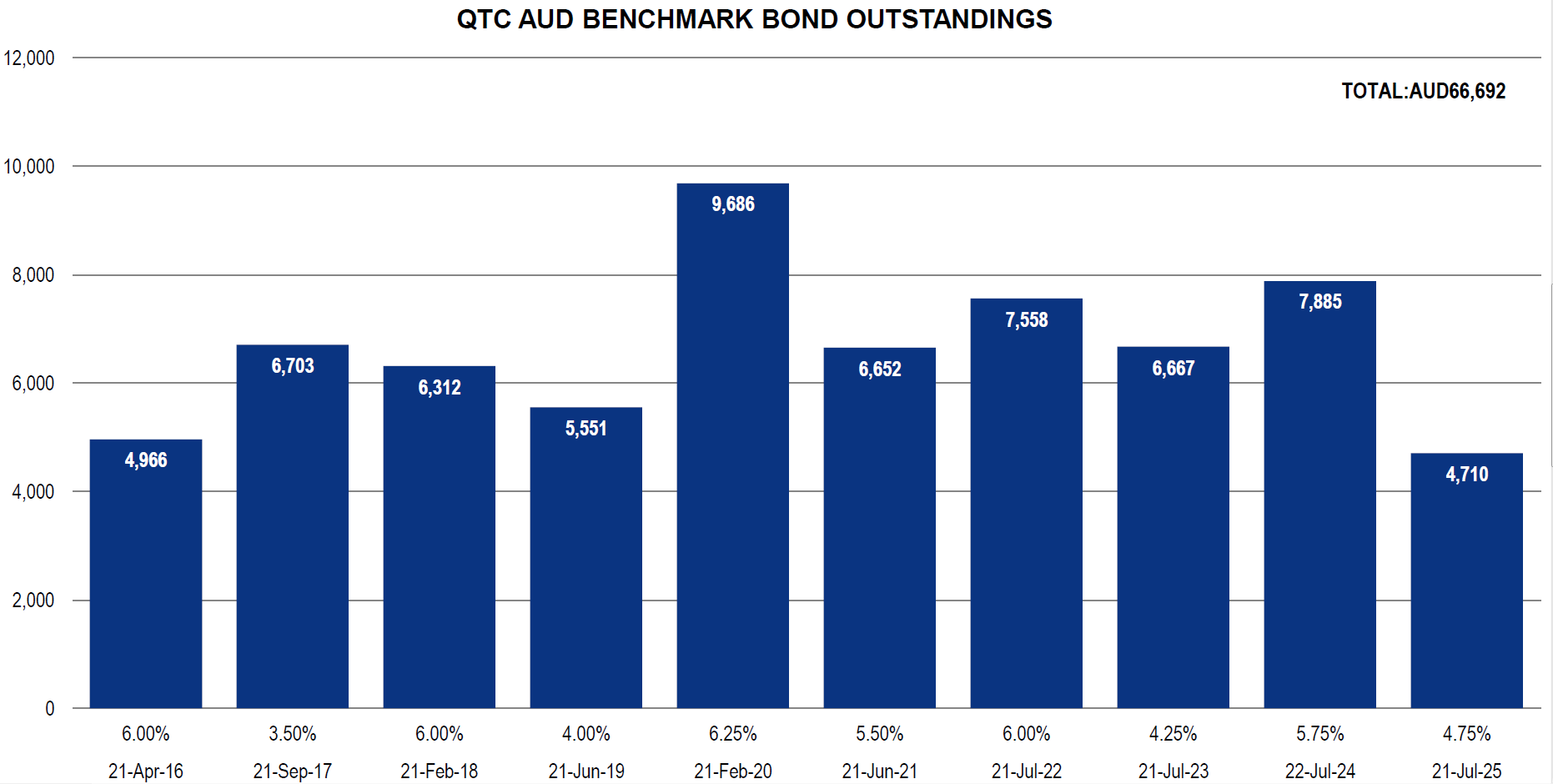

Queensland Treasury Corporation today priced a new benchmark 11 year bond. The new bond will mature in October 2026 and pay a semi-annual coupon of 3.25%pa. The size of the issue was $1.75 billion and they carry an AA+ (stable) rating from Standard & Poor’s and a Aa1 (negative) rating from Moody’s. The bonds will go part of the way to re-finance QTC’s $4.022 billion October 2015 bond that matured recently.

The issue yield to maturity was 3.33% or 63bps above the April 2026 commonwealth government bond (or EFP + 67bps) and the issue was led by ANZ, Citigroup and UBS.

QTC has $68.44 billion of benchmark AUD debt outstanding as well as $7.05 billion of floating rate notes. The chart below shows the present maturity profile of QTC’s regular bond issuance.

26 October 2015

Business confidence fell in the September quarter, dropping 4 points to 0, according to National Australia Bank’s quarterly survey of business confidence and conditions. The quarterly survey is a more thorough examination of conditions compared to the monthly survey and it also ask firms to provide their perceptions of their industries’ outlooks. NAB says the fall was likely to be due to the timing of the survey, which took place prior to the change of Prime Ministers and when concerns about Chinese growth were at their peak. Subsequent monthly surveys have indicated these concerns have abated and confidence has picked up. Confidence varied across industries, with construction and retail apparently the most buoyant, while firms in other sectors to point to subdued customer demand dampening confidence levels.

26 October 2015

- Expected margin of 5.10%-5.30% over 3m BBSW

- Franking level 85%

- First call date 22 Dec 2021

AMP has today announced a new issue of capital notes aimed at raising at least $200m of Additional Tier 1 capital. The securities will be perpetual, subordinated and unsecured with an optional exchange date on 22 December 2021 and a mandatory conversion on 22 December 2023. Distributions will be discretionary with an expected margin of 5.10% to 5.30% over the 90d bank bill rate – this includes franking at an expected 85% rate. The Capital Notes will have the usual APRA non-viability clause.

26 October 2015

National Australia Bank announced it will be offering investors access to managed funds via the ASX’s mFund Settlement Service and will include some of its own funds on mFund. The mFund Settlement Service allows investors to acquire and redeem units in unlisted managed funds via their sharebroker on the ASX. The service does away with many of the paper forms normally required for an unlisted managed fund application.

The mFund service uses CHESS, ASX’s electronic settlement system, to automate and track the process of applying for and redeeming units in these managed funds. Holdings, referred to ‘mFunds CHESS holdings’ are held electronically and can be linked to the same Holder Identification Number (HIN) used to hold other investments transacted through ASX. Investors can track their managed fund investments using the same systems used for shares and other securities.

National Australia Bank (NAB) is the first of the big four banks to offer this service and it joins Macquarie Online Trading which began offering the service earlier in October.

26 October 2015

Readers may recall PaperlinX’s 2013 offer to hybrid holders, the resulting dispute and the close of the offer without result in early 2014. The dispute is over the rights of hybrid holders against the rights of ordinary shareholders. The two parties came into conflict over the hybrid’s terms of issue.

Typically a hybrid will mature or cease to exist when the issuer, in this case PaperlinX, chooses to either redeem the hybrid at face value ($100.00), convert it into shares equivalent to the face value or repurchase the hybrids via a bid tender. PaperlinX, having made a series of losses in recent years, does not realistically have the second or third option available to it and so some sort of conversion is the most likely option.

The hybrids were issued with a face value of $100 and so conversion into ordinary shares would produce a massive dilutionary effect on ordinary shareholders. Hybrids holders have not received a distribution in recent years and so a reasonable valuation would be less than $100. But how much less?

Robert Kaye, the chairman of PaperlinX hinted at the 2015 AGM a resolution may soon be found when he said PaperlinX’s board will seek over the next 12 months “to address the group’s capital structure and with goodwill on behalf of all parties we hope to reach an agreement.”