26 October 2015

China’s determination to reinvigorate its economy has seen the People’s Bank of China cut its 1 year lending rate from 4.60% to 4.35%. In addition, it reduced the reserve cash requirements for all banks by at least 50bps, with some bank reductions up to 100bps or 1.00%.

Facing the weakest growth in two decades and anticipating further stimulus measures from the ECB and Japan, the PBoC moved quickly over the weekend to make the adjustments. China has seen producer prices easing and recent GDP growth data has been disappointing. While GDP was released at 6.9%, slightly higher than market expectations, few outside the country believe the figure and even point to the fact that the GDP number benefited from a surge in financial services activity as a result of the huge increase in share trading activity over the past year. A surge that is unlikely to be repeated.

22 October 2015

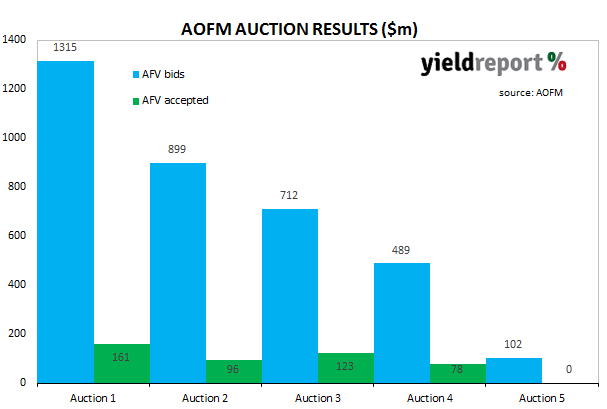

In late July, Rob Nicholls, the chief of the AOFM gave a speech regarding the divestment of the Residential Mortgage Backed Securities (RMBS) acquired after the GFC. In the speech he said the AOFM would sell the securities in an orderly fashion and without resorting to a “fire sale” but the latest auction would suggest an orderly sales process has become somewhat problematic.

The AOFM has nearly $3.5bn of RMBS on its books and $366m worth of securities were offered for sale. Bids for $102m were made but no bids were accepted. In a previous YieldReport article it was suggested the AOFM was seen as a disciplined seller but Westpac described the result as “disappointing” and noted the value of bids for each auction has been declining. The next auction is on 23 November 2015.

21 October 2015

Suncorp Group’s general insurance subsidiary AAI Ltd will be holding a series of meetings with investors in Australia and Asia in the last week of October. AAI Ltd has an A+ credit rating, the same as Suncorp’s banking subsidiary, Suncorp-Metway Bank, which recently had a dual-tranche 5y fixed and floating issue one week ago. Pricing for that deal was at Swap/BBSW + 125bps. Given A rated Macquarie Bank got a dual tranche fixed and floating deal away at Swap/BBSW + 105bps in the last day or so, it would seem that A+ rated AAI Ltd should be able to issue at a lower rate this time around.

20 October 2015

The Chinese National Bureau of Statistics released Q3 GDP figures which indicated a quarterly increase of 1.8%, 0.1% higher than expectations. The annual growth rate was 6.9% and slightly lower than the expected 7.0%. It’s the lowest annual result since 2009 and the NBS put it down to “increasing downward pressure of domestic economic development” and a “recovery of the world economy [which] was weaker than expected”.

ANZ’s Warren Hogan did not have a lot to say about the results other than to say the result added to “international market concerns over the integrity of the data.” Noted China watcher, Capital Economics’ Julian Evans-Pritchard said the numbers “will further cement concern over their credibility.” He believes growth in China is far lower than official numbers but regardless appeared to have stabilised.

Westpac zeroed in on the nominal GDP figure which the bank sees as a more reliable gauge of underlying demand conditions. It said the increase in nominal GDP indicates “growth decelerated in a material but not dramatic fashion in the quarter”. The 6.2% increase is down from the 7.1% annual increase reported for the Q2, as well as the revised Q1 figure of 6.6%.

Prior to the GDP release the Chinese government released fiscal revenue and expenditure data which suggested that official expenditure accelerated by a staggering 26.9% in the June quarter. This increase saw spending up 16.4% from the same period in 2014. It would seem abundantly clear that the government is doing its best to support the economy and growth from this stimulus may well flow through in the December quarter.

20 October 2015

The U.S Bureau of Labor Statistics released the September CPI figures which were largely in line with expectations. The headline inflation rate came in at -0.2% for the month, down from August’s -0.1%, as energy prices continue to offset price rises elsewhere in the economy. The year-to-date figure was -0.1%, down from August’s comparable figure of 0.2%. Core inflation, which strips out the more volatile food and energy components, rose to 1.9% for the last 12 months, up from August’s figure of 1.8% and higher than market expectations.

ANZ said the higher core inflation result suggests reduced spare capacity in the economy is offsetting the higher US exchange rate and lower energy prices. U.S core inflation had been steady at 1.8% for the six months previous to this result and the September core figure is just short of the Fed’s target of 2.0%. US 10y bond rates finished the day higher, up 5bps to 2.02%.

19 October 2015

Westpac’s out-of-cycle, 0.20% rate rise for all residential mortgages has provoked a number of investment banks and economists to bring forward their predictions of a RBA rate cut with some now expecting a rate cut as soon as November. According to a Bloomberg poll, six out of twenty-six economists now expect a rate cut in November, among them Macquarie Bank, Goldman Sachs and UBS.

The analysts believe that the mortgage rate hike, particularly if followed by the other banks, will lead to lower economic growth, hence the need for a rate cut. Some have even speculated that this may even be a co-ordinated move that allows for the RBA to cut rates without fuelling an already overheated housing market.

ANZ pointed out mortgage rate rises have been expected by the RBA since the APRA’s banking review that flagged the need for the big four banks and Macquarie to raise more capital ( and and ). Governor Glenn Stevens has previously said, ”If banks raised rates no-one should find that surprising or controversial…the whole point of [APRA changes] was to change the competitive landscape between the majors and the others”. However, Westpac’s rate rise seems to have provided the trigger for investment banks to bring forward or firm up their rate reduction timetables.

Macquarie said “Westpac’s hike all but seals the deal for a November rate cut from the RBA” while UBS sees a November cut as “the path of least regret for the RBA”. Nomura’s Australian fixed income strategist, Andrew Ticehurst, was not quite as certain, saying a rate cut was coming but not in November unless all the banks raised mortgage rates. “Nomura’s house view is for a 25bps RBA rate cut in February, and not this year…But particularly if the other three big lenders follow Westpac’s lead, this would of course increase the possibility that the RBA could respond this year.” Goldman Sachs introduced another consideration when the risk of a severe drought and its effect on growth were brought into the equation.

National Australia Bank and Westpac are holding out as a minority of banks which thinks rate cuts are not a given. “We find it difficult to mount a case for further policy easing on purely domestic grounds and view market pricing for another 25bp cut over the coming 6 months as overly pessimistic”, said NAB. Westpac’s chief economist, Bill Evans, is on record as saying interest rates will be on hold at 2.00% throughout 2016.

On the Friday prior to Westpac’s mortgage rate move, cash rate markets implied a 20% probability of a November cut. Over the course of the following few days, market pricing increased the odds to around a 40% chance.

19 October 2015

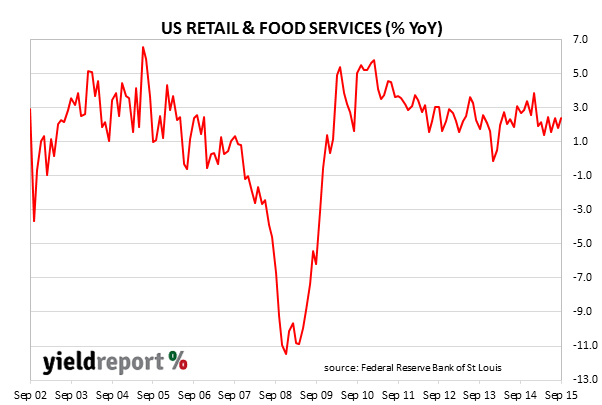

Car sales were again behind the larger-than-expected US retail sales figure for September with clothing and restaurants and bars the next largest growth segments.

The US Commerce Department released retail sales figures showing a 0.1% increase for the month, slightly less than the 0.2% expected but higher than the August figures which were revised down from 0.1% to 0%. The September figures are the seventh non-negative month in a row and represent a 2.2% increase from September 2014.

ANZ and Westpac called the figures “disappointing” and while ANZ bank still expects a December rate rise for the US, it thinks the likelihood has been reduced by these figures. US cash futures now imply a 30% chance of a rise by December and US 10 year Treasury yields fell 5bps on the day to 1.99%. However, known Fed “hawk” Jeffrey Lacker said the sales figures didn’t change the fundamental outlook and UBS said a “steady pick-up in the prices of other goods and services suggested inflation was set to rise”.

19 October 2015

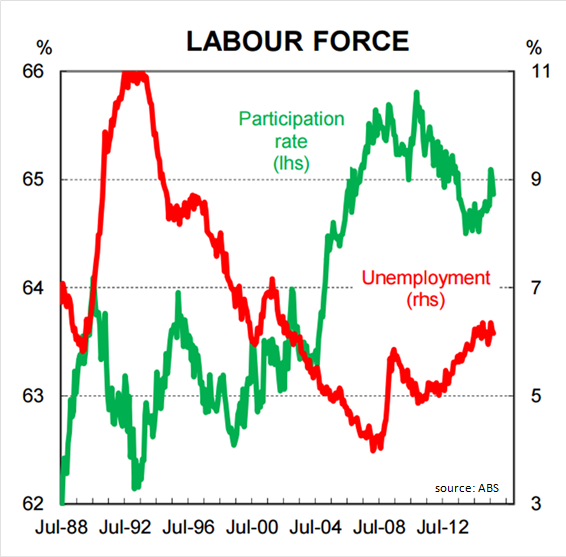

The ABS released the September Labour Force figures which came in less than the 10k increase which was expected. Commonwealth Bank said the drop does not change the underlying resilience of employment growth as the Australian economy transitions from mining investment and construction to non-mining activities.

The unemployment rate remained steady at 6.2% while the participation rate fell 0.2% to 64.9%.

Seasonally adjusted jobs fell 5.1k to 11.8m, the result of a fall of 13.9k full time jobs and an increase of 8.9k in part-time jobs. Total employment 2.0% in the year to September. Seasonally adjusted monthly hours worked in all jobs increased 12.2m hours in September 2015 to 1,638m hours, or by approximately 0.7% for the month and 2.5% for the year. Commonwealth Bank saw the rise in hours worked as “another positive in today’s data in terms of labour market solidity”.

There is more controversy surrounding the employment data as the former Australian statistics chief said prior to the release, “The results of the last six months aren’t worth the paper they’re written on, so why are we wasting millions of taxpayers’ money on the survey?” He said since early 2014 the ABS has effectively produced a different statistical series to what existed previously. Westpac was less harsh in its verdict saying, “We know the ABS is making significant adjustments to the underlying data to remove the volatility but this is a bit of a black box.”

The states with the lowest rates of unemployment were NSW (5.9%), W.A. (6.1%) and Victoria (6.2%) with NSW continuing its role as the largest employer of Australians. The state with the highest unemployment remains South Australia with a rate of 7.7%, which is down 0.2% from the previously recorded 7.9%.

15 October 2015

The minutes of September’s Federal Open Markets Committee (FOMC) were released and they revealed little in the way of new information. They confirmed more than a few members believed the conditions necessary for a rate increase had been met or would be met soon. Countering this view was a group of members who wanted further confirmation of labour market improvement, economic resilience and rising core inflation before moving to higher official rates. Westpac noted the unusually high number of references to the US dollar and said the absence of “robust” US wages growth meant global developments were seen as much more significant for the inflation outlook.

On the whole, the FOMC expects economic growth to remain “above its longer-run rate over the next two years and lead to further improvement in labour market conditions.” While inflation was expected to remain subdued, more of the FOMC members saw “the risks to inflation as tilted to the downside.” However the minutes also point to the rise in core PCE, the Fed’s preferred inflation measure. “Since January when the steep drop in energy prices ended, core PCE prices had risen at an annual rate of 1.7%, closer to the Committee’s objective”

Janet Yellen is seen from her speeches in late September as being supportive of a 2015 rise and Westpac sees the minutes as confirmation her view represents the consensus. The bank sees “no chance” of October 29 move but a rate rise in December is likely “barring a marked deterioration in the pulse of inflation and US domestic activity.” Commonwealth Bank said its view is the Fed rise would come in December “remains intact, though weak payrolls data over the past two months casts doubt on even that timetable.”

15 October 2015

Business confidence has recovered after a reduction in financial market volatility and the Federal Government’s leadership change, according to NAB’s September survey. The index rose 4 points to +5, reversing the 4 point drop in August. As part of the same survey, NAB also measures business conditions and this index remained steady with last month’s reading of +9.

NAB noted the improvement in confidence was not broad-based with the mining sector still under pressure and “notable” deteriorations in the construction and finance sectors, while the service sectors “continue to outperform”.

According to the bank, a lower exchange rate and record low interest rates are continuing to provide support to the non-mining sectors. Capacity utilisation lifted again to 81.3%, previously 81.2%, which NAB says bodes well for non-mining business investment and the labour market.

Labour cost growth increased in the month but the growth rate was 0.6% for the quarter and final product prices growth was slightly lower in September at a quarterly rate of 0.2%. NAB viewed the low growth in product prices as evidence that firms are currently finding the passing of higher prices on to customers as difficult, thus keeping consumer inflation contained.

JB Were said, “Components of the report were indeed encouraging, however the details of today’s survey caution against an overly optimistic interpretation of the headline result”, while AMP Capital’s Shane Oliver said the business conditions were still “OK”.

NAB said “the ongoing high level of business conditions and trend improvement in key leading indicators such as capacity utilisation supports our view that the gradual recovery in the non-mining economy is becoming more resilient.” In a statement which makes it the most optimistic of the banks, it said it views “market pricing for another 25bps cut over the coming 6 months as overly pessimistic.”