17 September 2015

The Office of National Statistics released August CPI and PPI figures which support the Bank of England’s view that deflation is “more likely than not”. The CPI grew by 0.2% in August, down from July’s figure of 0.1% and unchanged on a year on year basis. The less volatile core measure in August was 1.0% year on year, down from the comparable July figure of 1.2%. ANZ said the figures were in line with expectations and were the result of lower fuel prices. On the producer side, UK producer prices fell 1.8% in the year to August 2015, a larger fall than the comparable July figure of 1.6%. Core prices rose 0.1% in the year to August 2015, slightly less than the July figure of 0.2%. Earlier this year the BoE governor Mark Carney had said deflation during 2015 was “more likely than not” but it was expected to be temporary.

17 September 2015

“This is the most well telegraphed rate rise in the history of rate rises. So, if you’re not ready for it, you sure as hell have been warned. You’ve got no excuse.”

Guy Debelle told traders and investors to prepare for a new bond market order where volatility is almost certain to rise in times of stress. Giving a speech at an Actuaries Institute Seminar in Sydney, the Reserve Bank’s assistant governor said the emergence of algorithmic trading and the fall in liquidity which has arisen from stricter compliance regimes meant the market would be more volatile in times of stress.

He said the “flash crash” in the US highlighted the prevalence of algorithmic traders, otherwise known as high frequency traders, who now account for approximately one third of the Australian bond market trading activity and more than half of the US market. High frequency traders provided plenty of liquidity to buy small parcels of bonds at prices close to the market but the depth of liquidity was poor as there were few buyers prepared to take larger parcels. Liquidity could be “both good and bad simultaneously.”

Fund managers needed to recognise the bond market had changed, adapt the way they trade in bond markets and possibly have “a higher liquidity buffer” than in the past to handle unexpected redemptions. Liquidity had never been all that good during financial market crises but now it was worse as banks “are less able to be nimble buyers of assets whose prices they believe have overshot.” The change had arisen because of regulatory changes and internal risk tolerances”. He posed the question: “Has regulation increased the cost of liquidity provision too far with the result that liquidity in the bond market is now too low?”

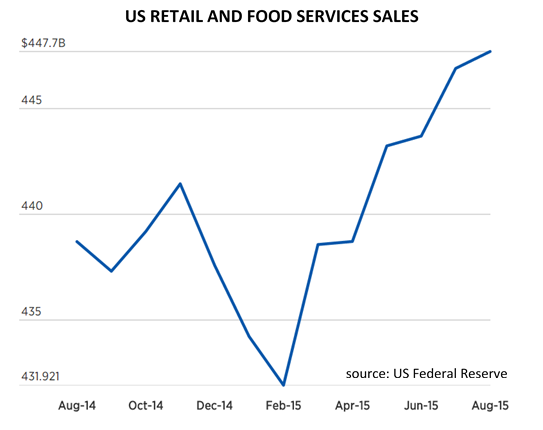

16 September 2015

Sales at retailers and restaurants boosted US retail sales figures in August, offsetting falls of building materials, gardening equipment and furniture stores. The US Commerce Department released retail sales figures showing a 0.2% increase for the month, slightly less than the 0.3% expected and lower than the July figures which were revised up from 0.6% to 0.7% but never the less the sixth consecutive monthly rise. The year on year figure came in at 2.2%.

16 September 2015

In the AOFM’s fourth RMBS auction, just under $78m of securities held by the AOFM were sold, representing a little under 16% of the amortised face value of bonds on offer. The amount sold was less than the previous three auctions held by the AOFM and is in spite of the amount on offer being reduced. The chief of the AOFM, Rob Nicholls gave a speech in July in which he discussed the aims of the sales process and he sought to dismiss theories the AOFM was under pressure to sell. The AOFM bought large swathes of RMBS from investment banks in the aftermath of the GFC in order to inject liquidity into the banking system and keep the mortgage market open. The next auction will be in late October.

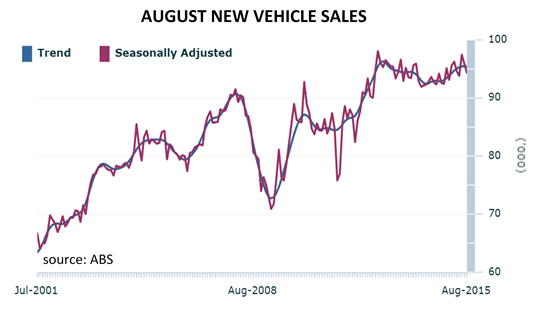

16 September 2015

ABS data released indicates a fall in new vehicle sales of 1.6% for August (seasonally adjusted), continuing on from July’s fall of 1.3% but less than the -2.0% expected. 94,332 new vehicles were sold in August, compared to the upwardly revised July figure of 95,896. The year-on-year result of 2.1% was also lower than July’s 3.7%. The Northern Territory recorded the largest percentage fall (3.3%) while Tasmania recorded the largest increase in sales (0.8%).

15 September 2015

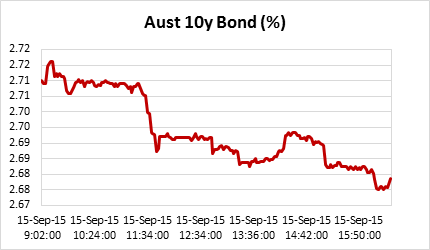

The market awoke to the news that Australia has its fifth Prime Minister in five years with Malcom Turnbull challenging Tony Abbott for the job and winning the party vote. Australia is becoming used to cutting down Prime Ministers and markets took the news in their stride. The joke doing the rounds was that the Richmond Football Club, an AFL club famous for sacking coaches, has had only one coach in the same period!

The move to a new PM saw 10y bond rates rise a couple of basis points as the new PM is seen as business positive and with rhetoric themed around kick-starting the economy. This was swiftly reversed after the RBA minutes were released at 11:30am as can be seen in the chart below of the day’s trading. The minutes of the September RBA board meeting were seen as decidedly “dovish” and long bond rates reversed the early morning trend to fall 2bps. The AUD also dropped against the USD.

Westpac’s Bill Evans said, “The minutes of the monetary policy meeting of the Reserve Bank Board for September provided no real surprises…it would appear that the Bank is now reasonably comfortable with the degree of adjustment of the AUD.” He went to say the RBA is “still not giving any encouragement” to a market expecting a rate cut by November.

JP Morgan’s Stephen Walters said the minutes revealed the chances of further reduction in the official cash rates was slim. “It likely would take more profound disappointments in markets or in conditions in Australia’s major trading partners, alongside domestic deterioration, including a higher jobless rate,” he said.

AMP Capital’s Shane Oliver noted how APRA’s lending restrictions on investment housing may mean the housing market is less of a constraint on rates but added there was nothing really new in the minutes.

The RBA minutes can be summed up as follows:

- Increased household expenditure and the depreciation of the Australian dollar were expected to produce growth in non-mining investment.

- Forward looking indicators of conditions pointed to the unemployment rate remaining around current levels.

- Mining investment appears is expected to weaken further than previously expected.

- Non mining investment was expected to fall further but a slower than previously anticipated rate.

- APRA’s measures had slowed the growth in lending for investment housing, Sydney remains buoyant but the rest of Australia house price inflation had been modest or even negative.

11 September 2015

Philip Lowe, deputy governor of the Reserve Bank, in his speech to the Committee for Economic Development of Australia covered the three themes which he says the RBA has endeavoured to communicate in the last few years:

- Australia’s economy is in a transition from the biggest resources boom in over a century to something a bit more normal. The transition presents challenges which are being compounded by what is happening offshore.

- A reasonably successful transition is probable. The Australian economy’s flexibility helped Australia deal with the upswing of the resources boom and is now helping us deal with the downswing. He made references to floating exchange rate, labour market supply in terms of increases and decreases in immigration and subdued wages growth.

- Monetary policy is helping this adjustment. He said, “It is entirely appropriate that, during a period in which both the terms of trade and mining investment are declining, monetary policy is accommodative.” However, the likelihood of a successful transition would be boosted by a lift in productivity growth and an increase in the risk-adjusted returns on investment. “The missing ingredient continues to be a lift in non-mining business investment, where we are still waiting for convincing signs of a pick-up…. but a material lift in non-mining business investment still seems to be some way away.”

This last statement could be construed as a hint as to the likely trigger for the RBA to begin the rate raising cycle. Though, it is clear from his statement, such a move is “some way away.”

10 September 2015

Firstmac announced it has mandated several banks to arrange meetings with investors in London and the US towards the end of September. The issue of securitised RMBS units is likely to follow.

10 September 2015

Willem Buiter, Citigroup’s chief economist since 2010 and former BoE Monetary Policy Committee member, believes there is a 55% chance of a global recession in 2016 or 2017. He thinks unlike most recessions which emanate from the US, the next one is likely to result from a slowdown in China and the build-up of excess manufacturing capacity there. The risk of what’s known as an economic hard landing is “high and rapidly rising” and he estimates China’s growth rate is already at 4%, well below the official target of 7%. The slowdown in China would be transmitted to the rest of the world’s economies as global trade drops away, given China accounts for roughly one seventh of it and financial markets would become involved if China started selling its massive holdings of US Treasury bonds.

He views the Chinese economy as “a messy market economy of the state-capitalist/crony-capitalist variety” and is sceptical of the effectiveness of Chinese policy. “The policy response to the weakening of domestic and external demand in China is likely to be too little and too late.” Beijing’s recent handling of its housing sector, share market bubble and the devaluation of the yuan, “don’t inspire confidence in the ability of the authorities…”

As the effects flowed to the rest of the world, developed nations would lack policy options. “Today, the interest rate is out of commission as a policy instrument in most developed markets and fiscal space is more severely constrained than in 2008 almost everywhere,” he says. The only lever left for the central banks in Europe, the United States and Japan to extend bond purchases although he views this policy as becoming incrementally less effective. Even so “this will not be enough to prevent most advanced economies from performing worse in 2016 and 2017 than in 2015”.

10 September 2015

In a move which markets expected, the Reserve Bank of New Zealand cut its cash rate target by 25bps to 2.75%. The Bank said it did so as a reduction in the rate was “warranted by the softening in the economy and the need to keep future average CPI inflation near the 2% target midpoint”. The Bank also said some further easing “seems likely”. It is the third rate cut since 2014 after a series a rate rises which the Bank is now reversing.