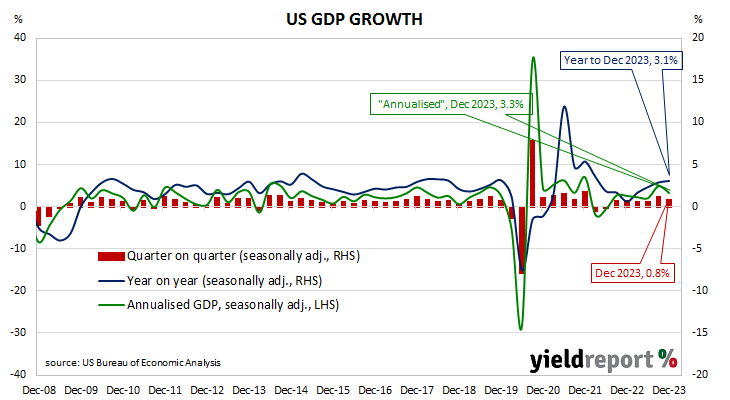

Summary: US GDP up 0.8% (3.3% annualised) in December quarter, above expectations; US Treasury yields fall; rate-cut expectations harden; GDP price deflator rate slows from 3.2% to 2.6%.

US GDP growth slowed in the second quarter of 2019 before stabilising at about 0.5% per quarter. At the same time, US bond yields suggested future growth rates would be below trend. The US Fed agreed and it reduced its federal funds range three times in the second half of 2019. Pandemic restrictions in the June quarter of 2020 sent parts of the US economy into hibernation; the lifting of those same restrictions sparked a rapid recovery which lasted until 2022.

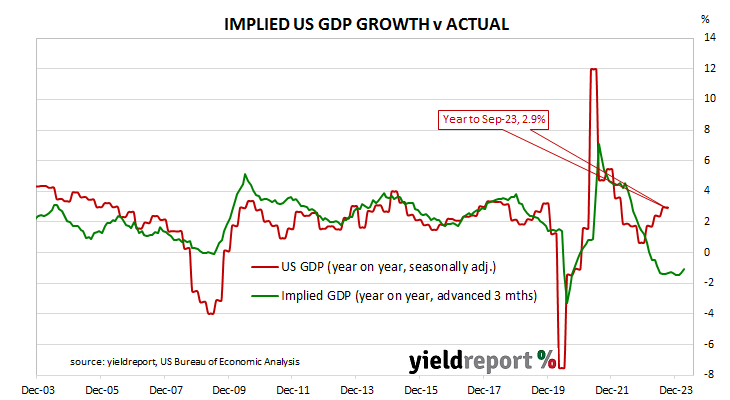

The US Bureau of Economic Analysis has now released the December quarter’s advance GDP estimates and they indicate the US economy expanded by 0.8% or at an annualised rate of 3.3%. The result was significantly more than the 0.5% increase (1.9% annualised) which had been generally expected as well as the September quarter’s 1.2% rise.

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with the figure from the same period in the previous year. The diagram above shows US GDP once it has been expressed in the normal manner, as well as the annualised figure.

US Treasury bond yields fell on the day despite the figures. By the close of business, the 2-year Treasury bond yield had lost 7bps to 4.31%, the 10-year yield had shed 5bps to 4.13% while the 30-year yield finished 4bps lower at 4.37%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months hardened, factoring in several cuts. At the close of business, contracts implied the effective federal funds rate would average 5.325% in February, in line with the current spot rate, 5.28% in March and 5.205% in April. January 2025 contracts implied 3.92%, 141bps less than the current rate.

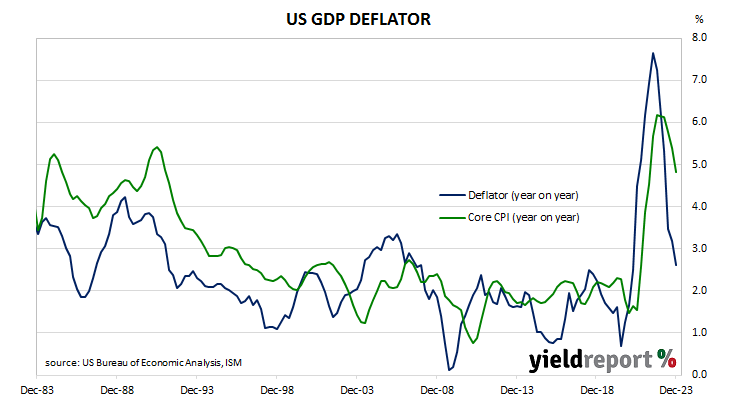

One part of the report which is often overlooked are the figures regarding the GDP price deflator, which is another measure of inflation. The GDP price deflator is restricted to new, domestically-produced goods and services and it is not based on a fixed basket as is the case for the consumer price index (CPI). The annual rate slowed again, this time from 3.2% to 2.6%.