09 September 2015

The ABS released the August Labour Force figures which came in as expected. The increase in jobs was a seasonally adjusted 17,400 to 11.8m, made up of 11.5k full time and 5.9k part time.

The unemployment rate came in at 6.2%, down 0.1% from the 6.3% recorded for July, helped by a lower participation rate which was 0.1% lower at 65.0%.

The states with the lowest rates of unemployment were NSW (6.0%), W.A. (6.1%) and Victoria (6.1%) with both W.A and Victoria showings falls from the July figure of 6.4%. The state with the highest rate remains South Australia with a rate of 7.9%, unchanged from the previous month. Seasonally adjusted monthly hours worked in all jobs decreased 0.6m hours in August 2015 to 1,623.8m hours.

Shane Oliver, AMP Capital’s chief economist, rated the result as “surprisingly strong” given the recent GDP figures he described as “soft”.

ANZ said, “Importantly, the employment-to-population ratio continued to rise, signalling a slowly improving labour market.” However, the banks says it expect employment growth to slow and at the moment the cash rate is likely to be reduced by the RBA.

While the 6.2% rate was as expected, Westpac said the rise of 17400 in total employment was “well above market expectations for a 5000 rise.”

08 September 2015

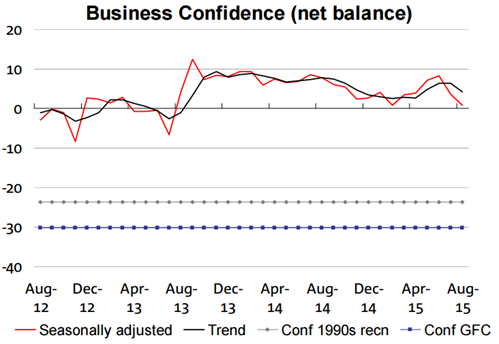

Business confidence has eased again according to NAB’s August survey, with the index falling to 1 from its previously recorded figure of +4. As part of the same survey, NAB also measures business conditions and this index rose a strong 5 points to +11. NAB said recent financial market ructions and Chinese growth concerns appear to be unsettling business confidence, although mining and construction recovered some of last month’s sharp declines and it wasn’t enough to send the confidence index negative.

According to the bank, a lower exchange rate and record low interest rates are probably offsetting weakness in the mining sector. The services sectors remain more buoyant than average, retail has improved but the wholesale industry remains weak. Business capacity utilisation rates have lifted to 81.2%, up from 80.9% and is close to the long-term average. Labour costs growth accelerated in the month but remains at relatively subdued levels and final product prices growth was pointing to moderate upward pressure on inflation.

Commonwealth Bank’s viewed the figures as quite robust: “On balance this was still a strong report and most of the subindexes were strong, with the notable exception of the employment index. But the result is only good if the fears about China prove unfounded.”

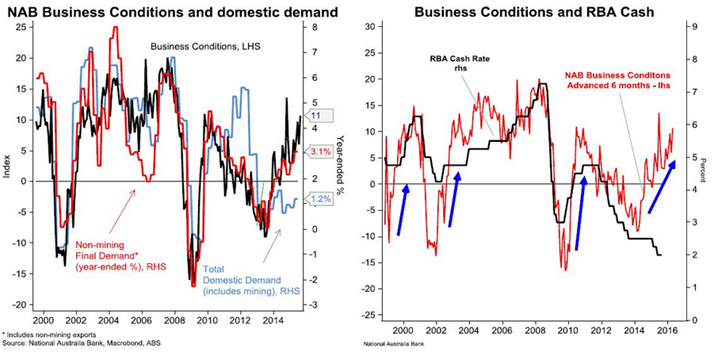

Peter Jolly, the NAB’s global head of research, in a note to clients said that some of the negative assessment of the outlook for the economy, particularly coming from international economists and journalists, were unwarranted.

He cited a business conditions chart (on the left) that showed a proxy for annual growth of the non-mining economy (red line) growing at around 3.1% year on year to June 2015. This growth line tracked well against the NAB Business Conditions survey he said and with the latest August business conditions number rising 5pts to +11 the economy was in robust shape. In fact, the chart on the right shows that when business conditions are this robust the RBA is usually lifting their cash rate target rather than lowering it.

08 September 2015

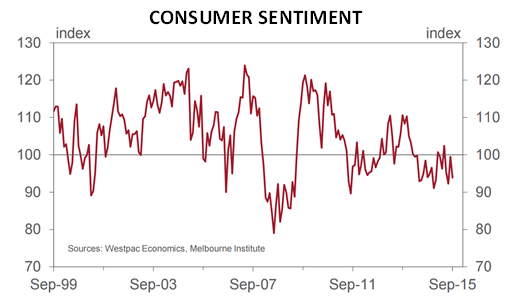

The Westpac – Melbourne Institute September survey of consumer sentiment was released showing a decline in the ratio of optimistic consumers to pessimistic consumers. A value below 100 indicates there are more pessimistic consumers than optimists and the September index dropped 5.6 points to 93.9 from the almost-neutral value of 99.5 registered in August. There was broad range of reasons which led to increased consumer pessimism with most of the components of the index falling.

Westpac’s chief economist, Bill Evans said he wasn’t surprised by the result. “We were somewhat puzzled by the surprise increase in the Index last month of 7.8% and there was always likely to be some correction this month. Of course the deluge of disturbing news around violent gyrations in both Australian and overseas equity markets, poor economic data from China, a disappointing report on Australia’s growth rate and the weakness in the Australian dollar were also likely to have unnerved households.”

Westpac still expects the RBA to maintain its steady rates policy through to the end of 2016. “The key to any decision to further cut rates, as expected by the financial markets, will be whether the Bank’s current forecast that the unemployment rate can stabilise around current levels proves sustainable.”

08 September 2015

Apple Inc, the ubiquitous maker of iPhones, iPads and Macintosh computers, made its debut in the Australian bond market in August when it issued 3 tranches of bonds. There were two fixed rate bonds and one floating rate note issued in the wholesale market at 2.88% (4y fixed & 4y floating) and 3.71% (7y fixed). Smaller investors were unable to buy the Apple bonds but FIIG, the fixed interest broker, has now made the bonds available to sophisticated and wholesale market customers in the secondary market in smaller parcel sizes.

08 September 2015

Ordinary Australian bonds have never traded at a negative yield as many European bonds did in 2015 but in the inflation linked bond market there have now been two instances of a negative yields at an ILB tender. ILBs are bonds that have the capital amount adjusted by the quarterly inflation rate thereby protecting investors from the effects of inflation. Well, that’s the theory.

Normally the rate received is a positive number above the inflation level. However, this week an ILB sold at a negative yield at tender. The investors in this instance are locking in a return that is below the level of inflation. The AOFM ILB tender was sold to 8 bidders at a ‘real’ yield of -1.69bps (i.e. 1.69bps below the level of inflation). This is the second time that an ILB tender has been sold at a negative yield with a tender in April being sold at -7.63bps for the same bond series.

Why would investors lock in a return below inflation for three years?

Inflation in Australia to the end of June 2015 was 1.50% and ordinary 3y bonds are currently priced at around 1.80%. If inflation stayed the same over 3 years the real return would be 0.30%. In other words the purchasing power of the funds invested would have increased by 30bps. If inflation rose above 1.80% over the 3y period then the bond investor’s purchasing power would be eroded.

So an investment in an ordinary bond runs the risk that if inflation rises sharply, the investor’s real return would be negative. That is, below the level of inflation. So if inflation was to rise sharply, investing in an ILB for 3 years would see the nominal returns rise commensurately albeit, in this case, less 1.69bps.

That is one of the reasons why an investor might buy ILBs at a negative yield. Effectively it is a 1.69bp option against inflation rising sharply.

There are other reasons of course that include many life offices and insurance companies having mandates to invest in such bonds or liabilities that match the investment profile of an ILB.

07 September 2015

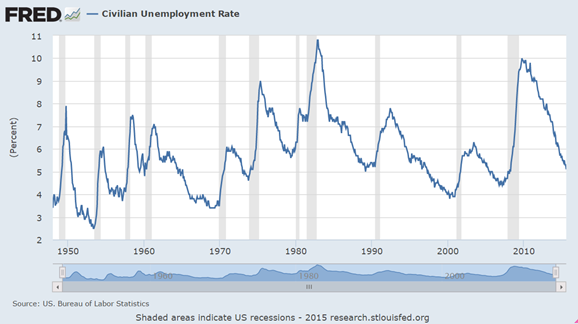

US employers added 173,000 jobs in August, below market estimates of 217,000, according to the US Labor Department. Unemployment dropped to 5.1%, the lowest rate since March 2008 and below the 5.2% rate expected. There were also 44,000 of upward revisions to the previous two months’ figures. Employment in mining and manufacturing declined, while education and health services added over one third of the new jobs. Richmond Fed president Jeffrey Lacker , a voting member of the FOMC and a known “hawk” said prior to the release the figures were unlikely to “materially alter the labour market picture or, for that matter, the monetary policy outlook.” But he added, “Waiting too long to begin raising rates could require a more dramatic increase in rates to restrain inflation pressures once they have become apparent in the data.” Opinions are divided as to whether the US Federal Reserve will leave official rates unchanged or raise them for the first time in almost ten years when the FOMC meets on 16 Sep.

07 September 2015

Saul Eslake, former Bank of America Merrill Lynch chief economist, thinks bond markets will act as safe havens from the turmoil recently seen in global share markets. He said, “I don’t believe the turbulence we’ve seen in the equities markets in the past couple of months…is the beginning of another significant global crisis. It’s more like the tech wreck of 2000.” He added the recent performance of bonds would have been better if bond prices were not already “richly valued” and there was not an expectation of a US interest rates rise.

07 September 2015

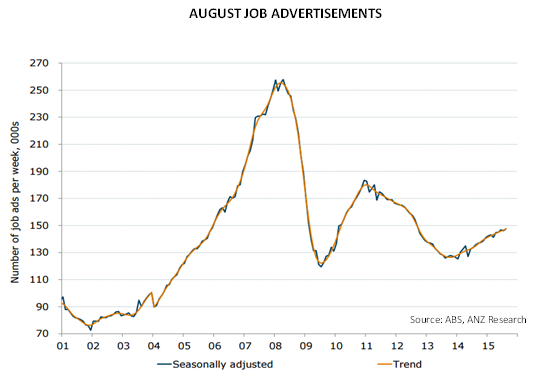

ANZ’s monthly job ads survey was released showing ads were up 1.0% (seasonally adjusted) compared to July and up 8.7% from August, 2014. The comparable July figures were -0.4% and 9.3% respectively. Internet ads were up 1.0% for the month while newspaper ads were up 0.8% but compared to a year ago internet ads were up 9.6% while newspaper ads were down 19.6%. ANZ’s chief economist Warren Hogan said, “The bounce in job advertising is a good sign for now.” Employment growth has been concentrated in service industries. However, he went on to say employment growth would “moderate” in the second half of the year as job losses are likely in the mining, mining-related construction and manufacturing sectors.

07 September 2015

Of the ASX-listed hybrid securities in the YieldReport survey, there are two securities making payments this week and two securities making payments next week.

This week ANZ Bank’s CPS3 (ASX code: ANZPC) and Capital Note (ASX code ANZPD) paid franked distributions on 1 Sep. Next week, AGL Energy’s Subordinated Notes (ASX code AGLHA) pays interest on 8 Sep, which is the same date for the payment of interest on Westpac’s Capital Note (ASX code WBCPD).

Primary Health Bonds (ASX code PRYHA) mature this month on 28 Sep. Holders will receive $100 plus interest.

04 September 2015

European Central Bank president Mario Draghi has announced a change to the ECB quantitative easing programme. Amendments to the QE programme, on the back of reduced 2017 GDP and inflation forecasts, give the ECB more flexibility to continue the asset (bond) purchase programme without running into roadblocks such as the 25% security issue limit (which has now been raised to 33%). It also sends a signal the ECB is prepared to do more if European growth and inflation figures don’t meet ECB expectations. The ECB president said the programme may continue past the original scheduled finish of September 2016. Talking about the pace of recovery and inflation he said, “Taking into account the most recent developments in oil prices and recent exchange rates, there are downside risks.” He noted European inflation figures may end up being negative but the circumstances would be “transitory” and due to oil price falls.