July’s trade deficit, or the value of the goods Australia imports less the value exported, was reduced by $0.6bn from the $3.1bn recorded in June. The figure was lower than the expected figure of $3.0bn, especially so when the result came so soon after the surprisingly large deficit for the June quarter. Exports were up 2.3% for the month while imports were flat. Exports of gold surged, while iron ore and coal exports receipts fell. Westpac described the result as “still sizable” but expects net exports for the full September quarter to add to GDP growth as the volume reduction seen in the June quarter is reversed.

News

July trade deficit “still sizable”

03 September 2015

Australian shoppers keep purses closed

03 September 2015

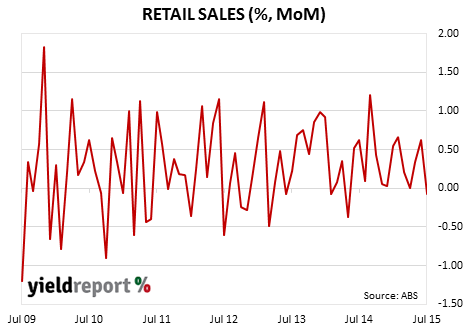

July retail sales decreased by 0.1%, less than the expected +0.4% and a fall from the previously recorded figure of +0.7%. The figures are notoriously volatile from month-to-month (see chart) but it’s the first negative figure since May 2014. AMP’s Shane Oliver thought a negative figure not unusual but he would be concerned if there were not a bounce in the August figure.

People’s Choice Credit Union roadshow

02 September 2015

People’s Choice Credit Union announced it has mandated several banks to arrange meetings with investors during the third week in September. The issue of RMBS under the credit union’s Light Trust programme is likely to follow.

Ex PIMCO stars criticise Fed

02 September 2015

Recently Alliance chief Mohamed El-Erian described the Federal Reserve’s attempts to prepare markets for the normalisation of US interest rate as “wishy washy” https://www.yieldreport.com.au/news/el-erian-says-fed-missed-its-chance-to-raise-us-rates/. His former colleague at PIMCO, Bill Gross, has joined the criticism of the US central bank saying to raise rates now would create financial market instability. However, he recognised a return to a neutral setting for official rates at 2.00% was needed. “The Fed is beginning to recognize that 6 years of zero bound interest rates have negative influences on the real economy – it destroys historical business models essential to capitalism such as pension funds, insurance companies, and the willingness to save money itself.” His advice to investors? “Cash or better yet ‘near cash’ such as 1-2 year corporate bonds are my best idea of appropriate risks/reward investments.” Gross writes a monthly report for bond fund Janus Capital in which he discusses the state of markets and his views on various matters. As the former chief investment officer at what was once the world’s largest bond fund, his views attract considerable attention.

Q2 GDP surprise (and not a good one)

02 September 2015

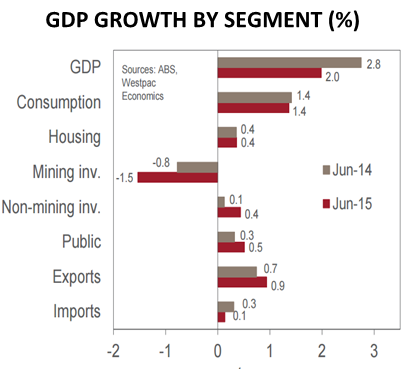

Australian GDP figures for the second quarter came in well under expectations, only growing by 0.2% or 2.0% year on year. The result was half the market expectation of 0.4% for the quarter. In the first quarter growth was 0.9% with annual growth at 2.5%. A sharp drop in export income resulting from lower prices and volumes for commodities and weaker business (especially mining) investment was blamed. The poor GDP result was despite significantly higher government spending and buoyant consumer and housing sectors that had been helped by low interest rates. Westpac noted that this number was unlikely to surprise the RBA which forecast 2% growth in its August Statement on Monetary Policy and will not lead to the rate cut which markets already have priced in. Westpac’s chief economist, Bill Evans, said “It does not appear to us…this print of the national accounts convincingly makes the case for further rate cuts.” UBS said something similar. “This is consistent with ours and the RBA’s near-term outlook for below-trend GDP growth of just 2.0%-2.5% and a cash rate unchanged at 2.0%.” AMP’s Shane Oliver held the contrary view saying 2.0% growth was well below potential and implied rising spare capacity which would lead the RBA to ease again and the dollar to drop below US$0.65. ANZ’s chief economist Warren Hogan said, “We are likely to see growth around this level for a long time.”

QBE roadshow for a new subordinated bond?

02 September 2015

QBE announced it has mandated several banks to arrange meetings with fixed income investors in Asia and Australia during the second week in September. The company stated a subordinated debt transaction may follow, subject to market conditions and terms. QBE’s last foray into debts markets was in November 2014 when it issued US$700m 2044 bonds which are callable in 2024. QBE has ₤300m of bonds maturing this month which will need to be refinanced from existing cash reserves and/or a new issue. The insurer has an A- rating from S&P and Fitch and a Baa2 rating from Moody’s.

June quarter exports drop, likely to reduce June GDP growth

02 September 2015

June quarter figures for Australia’s export and imports show a fall in the value and quantity of exports, in excess of the numbers expected by economists. Analysts had been expecting a current account deficit of around $16bn so the $19bn deficit was something of an unwelcome surprise. A deterioration from March’s revised figure of $13.5bn was expected but a fall of $2.3bn in the goods and services trade surplus and an increase in interest and dividends paid offshore increased the overall deficit. Coal export volumes were down as bad weather delayed shipments although iron ore volumes remained close to the all-time high reached recently. The effects of lower volumes were compounded by a fall in the ratio of export prices to import prices, which declined 3.4% over the quarter and 10.6% over the year. The new figures suggest June quarter GDP growth will be 0.6% lower as a result.

AMP’s new hybrid

02 September 2015

AMP is sounding out investors about a new issue of listed hybrids securities. AMP already has its AMP Capital Notes 2 trading on the ASX, which were issued in 2013 and pay distributions at BBSW + 265bps but the new hybrid is thought to be priced at close to BBSW + 500 bps. At this stage there is little information to go on but it’s not far-fetched to bet it would be similar in terms to the $275m Wholesale Capital Notes issued in March at BBSW + 400bps. Those notes were perpetual, unsecured, subordinated debt obligations with a mandatory conversion date in 2020 and a “non-viability trigger event” conversion clause to give them a Basel 3 tier 1 equity status. Tasmania’s MyState Financial, issued a 10y subordinated bond in early August at Swap + 500bps.

Housing pushes private sector credit higher

01 September 2015

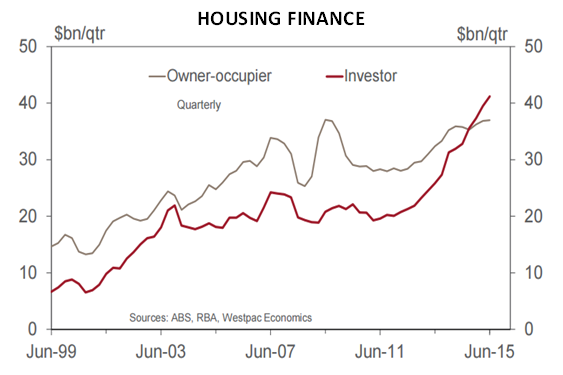

Loans to the private sector grew at a slightly higher rate in July. Loans to business were the main drivers of the higher-than-expected figures, rising 0.7% for the month (previously 0.1% in June) and 4.8% over the year and they offset the figures for personal loans which were flat for the month (previously 0.3% in June) and only 0.9% over the year. Housing loans continued to grow steadily, coming in at 0.6% for the month and 7.4% for the year. AMP’s Shane Oliver speculated APRA lending guidelines may be having an impact on the investor portion of housing loans but suggested more time was needed to confirm the effects due to the lag between approval and the actual draw-down of the loans.

RBA: September rates on hold, economists’ views diverge

01 September 2015

The RBA decision to maintain the official cash rate at 2.00% came as no great surprise to the markets, although the Aussie dollar went 0.50 cents higher immediately after the decision. The RBA seems satisfied with the level of the currency and no longer thinks further depreciation seems both likely and necessary as it did in a previous statement. As in past statements, the RBA expressed some positive views of Australian unemployment rates and moderate economic growth while acknowledging “spare capacity” and offshore weakness. Inflation is expected to remain at the Bank’s target for the next year or two. “In such circumstances, monetary policy needs to be accommodative.”

JP Morgan thought the statement was not materially different from the August one and expected rates to stay on hold until the final quarter of 2016 while TD Securities strategist Prashant Newnaha said “doves” would be disappointed by the statement. On the other hand, AMP’s Shane Oliver thought the RBA’s reference to the “economy operating at spare capacity for some time” was an important point but then said, “If the RBA does have a dovish bias, it is very mild one.” RBC Capital Markets senior economist Su-Lin Ong took a stronger position. “We still have two cuts in our profile, one towards the end of 2015 and another in mid-2016 which takes cash to 1.5 per cent”. She thinks a weak China, lower commodity prices and weaker capex will force the RBA’s hand to cut rates to 1.5%. Westpac’s chief economist Bill Evans said that rates would stay at 2.00% throughout 2016.

Click for more news