Moody’s announced QBE is up for review of its credit rating and a possible credit rating upgrade. Moody’s said QBE’s management had acted to reduce gearing and improve the quality of its earnings. Moody’s senior analyst Frank Mirenzi said, “The sustainability of QBE’s current capital structure, with lower levels of financial leverage, and the sale of underperforming businesses, may, over time, improve the underlying performance of the group.” Currently QBE has a rating of Baa2 from Moody’s and A- from S&P and Fitch.

News

QBE set for ratings upgrade

25 August 2015

Asciano a higher risk after Brookfield takeover

24 August 2015

Moody’s has placed Asciano on negative credit watch following the agreement between the board of Asciano and its suitors, the Brookfield Consortium, in regards to Brookfield proposed takeover. The change in outlook relates to Moody’s concerns the new owners will apply a risker approach to balance sheet financing or the consortium looks to refinance the acquisition funding by raising debt at Asciano. Asciano currently has a Baa2 rating but the rating will be cut a notch if the ratings agency thinks the debt to EBITDA ratio is maintained above 4 and/or the EBIT to interest ratio falls below 1.5.

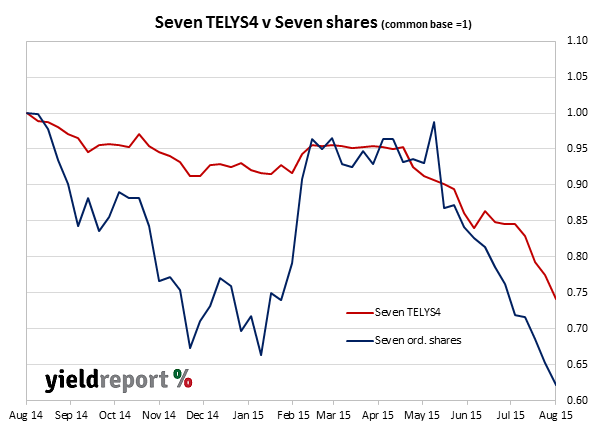

Seven’s TELYS 4 hybrid storm in a tea cup

24 August 2015

Seven Group is chaired by well-known WA businessman Kerry Stokes and owns a 35% stake in Seven West Media (owner of the Seven Network, some radio stations, magazines and WA Newspapers) as well as a 68% interest in Caterpillar Australia, an investment fund with holdings in ASX listed stocks and various properties.

Recent newspaper reports have focussed on the company’s listed hybrid securities, or TELYS4 (ASX code: SVWPA) which have been subject to substantial price declines in the past month. TELYS4s were trading at $80 per security at the start of July and dropped as low as $62 on 20 August, down 7.8% on the day. Volume of trade on the day was five times more than average, however the value of trade was only $1.75 million.

It has been reported there is a rumour doing the rounds that Seven Group may not pay the next hybrid distribution and that some investors were getting nervous about this, hence the sell-off. YieldReport should point out it has seen no basis for this nor any comment from the company itself. In any case, it is worth noting the distribution, while discretionary, is also subject to what is called a “dividend stopper” clause in the terms of the issue. A dividend stopper is a clause which stops the issuer, in this case Seven Group, from paying dividends on its ordinary shares unless the distribution/interest on the hybrid is paid first. A cessation of ordinary dividends would affect Kerry Stokes personally as he is the largest Seven Group shareholder. Seven Group has been paying six monthly ordinary dividends at a rate of 20 cents per share and so a pause in payments would cost him around $80 million cash and $34 million in franking credits for every year.

It’s been suggested the fall in the price of TELYS4 is feeding into the price of the ordinary shares. An analysis of the trading of the two securities may call that proposition into question. A diagram of weekly traded prices over the last 12 months shows how the ordinary shares (ASX code: SVW) fell first, then recovered and then led the hybrid securities (ASX code: SVWPA) down, not the other way around.

Seven Group has debt of $800 million and $1 billion of listed and unlisted assets on its balance sheet and is due to report its annual results in late August. The hybrids have a running yield of 7.5% fully franked or the equivalent of 10.7% before tax at the current price.

Vanguard sounds warning on ‘rules-based’ ETFs

24 August 2015

Vanguard, seen as the pioneer of the low cost passive investment strategy now manages over $4bn in bond and equity funds. Rodney Comegys, head of investments at Vanguard says, “Indexing is hot. Target date funds are hot. Exchange-traded funds just keep growing.” Vanguard is now the largest bond fund investor in the world and it’s partly a reflection of the dissatisfaction investors have with active managers’ performances and fees. However, parts of the passive investment community have sought ways to become wring more out of their passive returns. Starting in 2006, ETF providers such as Wisdom Tree launched one of the first alternatively weighted ETFs, calling them “fundamentally weighted.” Describing the ETFs as rules-based and offering representative exposure to an asset class, the new style of index ETF had “alternative weighting methods” and a high correlation to established benchmarks. This style became known as “smart beta”, which The Economist later defined as an approach that tries to enhance the return from tracking an asset class by deviating from the traditional “cap-weighted” approach, with “deviation” produced by employing screens and filters over the benchmark index. However, Vanguard and Comegys are wary. “It’s neither smart nor beta…we are talking a rules-based active strategy. It’s going to perform like active. It’s going to outperform, underperform, it’s going to have transaction costs and there are taxes that have to be paid.”

Apple’s stunning Australian dollar bond issue

21 August 2015

The world’s largest tech company, Apple Inc., tapped the Australian bond market on Friday for $2.25bn worth of Australian dollar denominated bonds in three tranches; 4y fixed rate, 4y floating rate and 7y fixed rate. The issue is the largest seen for an international company issuing corporate bonds in Australia as the company was deluged with over $3bn worth of orders.

Pricing for the iBonds, as they are being dubbed, came in at 5-10bps ahead of initial guidance.

The 4y fixed rate tranche was for $400m at 2.88%, or BBSW + 65bps, the 4y floating rate tranche was for $700m at BBSW + 65bps and the 7y fixed rate tranche was for $1.15bn at 3.71% or Swap + 110bps.

Part of the reason for the demand was the high quality of the issuing company and the fact that Apple is one of the few non-bank companies rated AA+ by S&P. This allows investors to diversify their risk into a high quality company that is not directly exposed to the banking system.

For Apple, issuing AUD bonds is a way to diversify its funding base away from USD and partially hedge its sales revenue in Australia. The company has a market capitalisation of around US$650bn and is sitting on a cash hoard of over US$200bn that is stashed around the world, out of reach of the US taxman. If Apple was to repatriate that money back to the US it would immediately be hit with corporate tax at the rate of 35%. So it prefers to keep the money outside the US, borrow money to pay dividends and undertake share buy-backs. The cost of borrowing itself is a tax deduction.

As Apple’s cash pile grows, the risks of borrowing in the one market and one currency grows so Apple began borrowing in yen, pounds, Swiss francs and euro. This latest $A bond issue is a further attempt to diversify its funding sources.

The issue is a tremendous fillip for the Australia bond market that has recently seen SAB Miller issue $700m worth of $A corporate bonds and that is seeking to increase the breadth of corporate bond offerings in this country. The swiftness of the raising and the keen pricing will no doubt encourage other issuers to consider the Australian debt market.

El-Erian says Fed missed its chance to raise US rates

21 August 2015

Allianz chief economic adviser Mohamed El-Erian says the US Fed had missed its chance to raise interest rates when US and international data was “more in alignment”. There had been an opportunity to get off zero interest rates when US domestic data was relatively strong and international data was OK but this had now passed. A gloomy outlook for international markets that began in emerging markets but was now spreading to mainstream markets highlighted the Fed’s most glaring problem of “pretty awful international data”. As a result the Fed has ended up looking “wishy-washy” when it came to preparing the market for an eventual interest rate hike. The recent Fed minutes show that the Fed is torn between raising rates in September and waiting for more data to confirm that economic recovery in the US was on track. Recent weak data out of China, falling energy and commodity prices and the devaluation of China’s yuan had created uncertainty about the world’s second largest growth engine.

July Fed minutes show dilemma of when to raise rates

20 August 2015

Minutes of July’s Federal Reserve Open Markets Committee (FOMC) were released last week and indicated that it is torn between a rate hike in September or waiting further for confirming data. Westpac said the minutes showed a leaning towards a rate hike by the Fed but more evidence of inflation moving back towards 2% and economic growth would be required before a move was made. The bank also noted the downgrading by Federal Reserve staff of its internal inflation outlook. According to the minutes, “some participants expressed the view that the incoming information had not yet provided grounds for reasonable confidence that inflation would move back to 2 percent over the medium term.” However, the meeting itself was held before an upward revision to first quarter GDP figures, a solid second quarter GDP figure and a July unemployment rate described as being close to full employment. Westpac said this new information was the evidence required by Fed board members. ANZ was not quite as confident saying, “Given that commodity prices have fallen further since the FOMC meeting, it is a fair assessment by the market that the odds of rates being lifted next month is not as high as it was.” CBA believes December is the most likely timing for a move but it was not as positive as market pricing was suggesting.

As for the Federal Reserve holdings of Treasury bonds and mortgage backed securities, the minutes indicated no particular hurry to offload them back to the private sector. The holdings will be maintained as interest rates in the US rise until at least the early stages of the rate rising cycle. Currently, as the US central bank’s holdings of bonds mature, the redemption proceeds are reinvested back into the purchase of more securities in the US bond markets, thus maintaining downward pressure on market interest rates. The reinvestment policy would remain until the FOMC thought economic conditions allowed.

Benchmark US 10y rates fell about 6bps on the day, finishing at 2.14% while the US dollar dropped against major currencies.

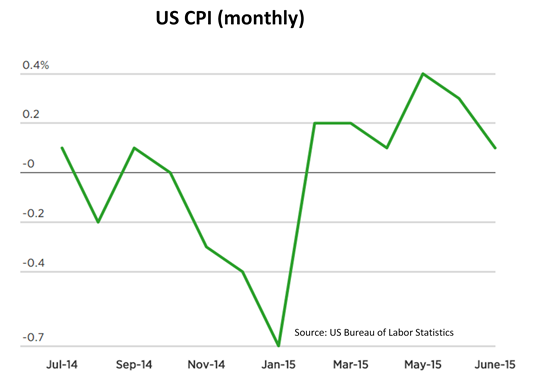

US CPI as expected, airfares keep inflation grounded

20 August 2015

The US Labor Department released July CPI figures that were largely in line with expectations. Airfares dropped the largest amount since 1995 and that was the driver behind the headline CPI figure rising 0.1% instead of the consensus 0.2%. The year to date figure was 0.2%, up marginally on the 0.1% comparable figure from June. Core inflation, which strips out the more volatile food and energy component, came in at 1.8% for the last 12 months, the same as June’s figure and in line with market expectations. US 10y bond yields fell to 2.13% on the back of the results but as it occurred at the same time as Chinese share market volatility there was potentially a “flight to safety” aspect to the bond market move. ANZ said lower oil prices and the stronger USD has broadly offset the effects of a reduction in spare capacity in the US economy.

The US Labor Department released July CPI figures that were largely in line with expectations. Airfares dropped the largest amount since 1995 and that was the driver behind the headline CPI figure rising 0.1% instead of the consensus 0.2%. The year to date figure was 0.2%, up marginally on the 0.1% comparable figure from June. Core inflation, which strips out the more volatile food and energy component, came in at 1.8% for the last 12 months, the same as June’s figure and in line with market expectations. US 10y bond yields fell to 2.13% on the back of the results but as it occurred at the same time as Chinese share market volatility there was potentially a “flight to safety” aspect to the bond market move. ANZ said lower oil prices and the stronger USD has broadly offset the effects of a reduction in spare capacity in the US economy.

Read more about inflation and why it is important to investors.

Lloyds Bank roadshow, potential new issue

20 August 2015

Lloyds Bank has announced a series of investor meetings in what is seen as preparation for a potential issue of a Kangaroo bond. The last time Lloyds issued AUD bonds was in March this year when it had a two-tranche issue of 5y fixed and floating securities at BBSW + 110bps. Lloyds has an A/A1 rating.

Citibank flags roadshow, potential new RMBS

20 August 2015

Citibank Australia announced it will be arranging a series of investor meetings on its own behalf, which is typically a prelude to a forthcoming debt issue. Citibank’s Securitised Australian Mortgage Trust programme last came to market in November 2014.

Click for more news